Rheological Additives Market

Rheological Additives Market & Trends Analysis Report, By Type (organic rheological additives, Inorganic), By Application (Paints and Coatings, Cosmetics & Personal Care), By End User (Liquid, Powder)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

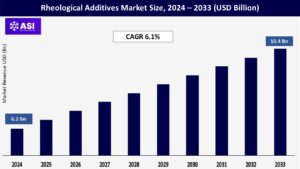

CAGR: 6.1%

Last Updated : March 13, 2026

The global rheological additives market size was valued at approximately USD 6.2 billion in 2024 and is projected to reach USD 10.4 billion by 2033, growing at a CAGR of 6.1% during the forecast period.

Rheological additives are critical performance enhancers used to control the flow properties, consistency, and suspension of materials across various industries, including paints & coatings, cosmetics, pharmaceuticals, and construction.

Growth is primarily fueled by increasing demand for high-performance and sustainable formulations, technological advancements in additive chemistry, and rising consumption across end-use sectors such as automotive, construction, and consumer goods.

The market for rheological additives is mostly driven by the paints and coatings industry’s explosive growth, especially in Asia-Pacific and North America. These additives are essential for maximizing coatings’ viscosity, flow properties, and application attributes.

Rheology modifiers play a crucial role in architectural, industrial, marine, and automotive coatings by reducing pigment sedimentation, facilitating smooth brush or spray application, and improving surface gloss.

Demand is being further accelerated by increased vehicle production, urbanization, and infrastructure developments, particularly in emerging countries like China, India, and Southeast Asia.

The need for high-end, natural, and clean-label formulations is driving the significant expansion of rheological additives in the personal care and cosmetics industry. Creams, lotions, gels, and serums are among the products whose texture, stability, and spreadability are regulated by these chemicals.

Customers are increasingly looking for items that provide both exceptional sensory experience and utility, particularly in North America and Europe. Rheology modifiers facilitate the creation of novel formulations, including high-viscosity serums, transparent gels, and waterless cosmetics by stabilizing emulsions and enhancing consistency.

Stricter environmental rules are putting more and more pressure on the market for rheological additives, especially with regard to volatile organic compound (VOC) emissions, chemical safety, and product sustainability.

The usage of synthetic, solvent-based, and petroleum-derived rheological agents is being subject to stricter regulations from regulatory authorities like REACH (Europe), EPA (U.S.), and regional environmental agencies in the Asia-Pacific.

Although these rules are encouraging the use of waterborne and bio-based substitutes, they may also restrict the use of conventional high-performance additives, particularly in situations where reformulation is expensive or technically challenging. Adherence to changing standards lengthens the time needed to develop new products and raises R&D costs.

Supply chain interruptions, energy prices, and geopolitical events can all affect the price of essential raw materials like organoclays, fumed silica, cellulose ethers, and synthetic polymers. The cost of producing rheological additives can be greatly impacted by these variations, particularly for smaller producers with few sourcing options.

Furthermore, margins are further strained, and consistent pricing is hampered by uncertainty surrounding international commerce, growing freight costs, and sporadic shortages of natural feedstocks or specialty chemicals (such as guar gum or xanthan gum).

For downstream users in coatings, personal care, and industrial formulations, price volatility also makes long-term supply contracts and planning more challenging.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Organic Rheological Additives Inorganic Rheological Additives |

| By Application |

Paints and Coatings Cosmetics & Personal Care |

| By End User |

Liquid Powder |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Rheological Additives Market is segmented by Function (Acidulant, Emulsifier, Diuretic), By End-Use (Food & Beverage, Pharmaceuticals, Personal Care, Industrial).

Each factor plays a crucial role in enhancing patient safety, increasing the adoption of self-administered anticoagulant therapies, and supporting the development of more convenient, prefilled drug delivery systems that streamline treatment in the management of thromboembolic and cardiovascular conditions.

The dominant segment is organic rheological additives.

The greatest market share is held by organic rheological additives, mainly because of their superior compatibility with water-based formulations and the rising demand for low-VOC, environmentally friendly systems.

These include acrylic polymers, cellulosic thickeners, and modifiers based on polyurethane, which are frequently found in adhesives, coatings, personal care, and household goods.

The market for organic rheology modifiers is still expanding due to the growing need for environmentally friendly and manageable additives, especially in the paints and coatings and cosmetics industries.

They are extremely adaptable in both industrial and consumer applications because to their capacity to provide smooth flow, sag resistance, and long-term stability throughout a broad range of pH and temperature conditions.

Rheological additives that are inorganic

In solvent-based and high-performance formulations, inorganic additives such metal soaps, bentonite clay, hectorite, and fumed silica are commonly utilized. These additives are perfect for industrial coatings, adhesives, sealants, and lubricants because they have outstanding thixotropy, anti-settling qualities, and resilience to high temperatures and mechanical stress.

In situations where superior structural strength, thermal stability, and viscosity recovery are crucial, inorganic rheology modifiers are nevertheless necessary, while being less sustainable than their organic counterparts. Particularly in areas with well-established manufacturing bases, demand is stable for products like heavy-duty industrial chemicals, protective finishes, and automobile coatings.

The Widest Use of Paints and Coatings

The market for rheological additives is dominated by the paints and coatings industry, which is fueled by robust demand for protective, industrial, automotive, and architectural coatings. In order to guarantee ideal viscosity control, sag resistance, anti-settling behavior, and smooth application using brushes, rollers, or spray systems, rheology modifiers are crucial in these formulations.

These additives aid in achieving consistent film thickness in architectural coatings and guard against dripping or uneven surface textures. They assist the performance stability and integrity of the film in industrial coatings, particularly those subjected to extreme environments.

The usage of rheological additives, especially organic ones, is increasing in Asia-Pacific, North America, and Europe as water-based and low-VOC formulations become more and more popular.

Cosmetics & Personal Care

Rheological additives play a critical role in personal care products such as creams, lotions, gels, serums, sunscreens, and hair care formulations. They contribute to texture, spreadability, stability, and overall sensory appeal, which are key factors in consumer product preference.

The growing shift toward clean-label, organic, and plant-based cosmetics, particularly in Europe and North America, is increasing demand for natural and multifunctional rheology modifiers such as xanthan gum, hydroxyethylcellulose, and natural clays.

Additionally, the rise of skincare innovations like waterless formulations and multiphase gels is pushing the need for rheology control to ensure formulation stability and market differentiation.

Liquid

Because of their quick dispersion, ease of inclusion, and suitability for automated, continuous manufacturing processes, liquid rheological additives are frequently chosen in industrial applications.

They are particularly favored in adhesives, aqueous coatings, and personal care items where uniformity and efficiency depend on quick and even blending into the formulation.

Large-scale operations frequently choose liquid forms because they improve process control and minimize dust handling problems. However, compared to powdered alternatives, they usually have a shorter shelf life and need to be stored more carefully.

The fastest-growing segment is powder.

Due to their longer shelf life, reduced storage and transportation expenses, and growing use in dry-blend and pre-mix formulations, powdered rheological additives are expanding at the quickest rate. In building materials (such as dry-mix mortars, tile adhesives, and grouts) and powder coatings, where on-site mixing is typical, these additives are especially sought after.

Because powder forms frequently eliminate the need for solvents, decrease packaging waste, and offer greater formulation flexibility, they also complement the expanding sustainability initiatives. Market penetration is also being aided by their growing use in small-scale or portable manufacturing setups, especially in emerging nations.

Asia-Pacific dominates the global rheological additives market, both in terms of volume and growth rate. The region benefits from large-scale industrial manufacturing, infrastructure development, and a booming middle-class population that is driving consumption across paints, cosmetics, pharmaceuticals, and construction sectors.

Countries such as China, India, Japan, and South Korea serve as major production and consumption hubs. China, in particular, is a key global supplier of both organic and inorganic rheological additives, supported by an extensive chemical manufacturing base.

India’s rising demand for packaged cosmetics and construction chemicals also contributes to regional growth. Additionally, government-led investments in industrial and smart city infrastructure projects are further fueling demand.

North America remains a mature and innovation-driven market, led by the United States, which accounts for the majority of regional demand. The region is characterized by high R&D investment, a well-established paints & coatings industry, and an advanced personal care and pharmaceutical sector.

There is growing momentum toward sustainable, low-VOC, and bio-based rheology modifiers, with companies actively developing green alternatives to meet regulatory and consumer expectations. The presence of leading global manufacturers, strong intellectual property frameworks, and stringent product quality standards support continued market development.

Europe represents a highly regulated and environmentally conscious market for rheological additives. The region is a leader in sustainability, eco-label compliance, and clean-label cosmetics, which is driving demand for bio-based and naturally derived rheology modifiers.

Countries such as Germany, France, the UK, and Italy are major consumers, especially in sectors like specialty coatings, skincare, and construction chemicals. European manufacturers are also investing heavily in R&D to replace solvent-based systems with waterborne alternatives, increasing the uptake of organic rheology modifiers.

The Latin American and MEA regions are witnessing moderate but rising demand, particularly in countries like Brazil, Mexico, UAE, and Saudi Arabia. Growth is driven by urban development, infrastructure upgrades, and increasing demand for consumer products, especially personal care and household formulations.

However, market expansion is somewhat limited by price sensitivity, inconsistent regulatory frameworks, and limited local manufacturing capacity, leading to a high reliance on imports. Nevertheless, with increasing foreign investment and industrial modernization, these regions are expected to offer long-term growth potential for global suppliers.

The global rheological additives market size in 2024 was USD 6.2 billion

The projected CAGR of the rheological additives market is 6.1%

The Paints & Coatings dominate the rheological additives market.

Asia-Pacific shows the highest growth potential in the rheological additives market.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Rutile Market, By Grade

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Rutile Market, By Application

5.3 Rutile Market, By End User

6.1 North America Rutile Market , By Country

6.1.1 Rutile Market, By Grade

6.1.2 Rutile Market, By Application

6.1.3 Rutile Market, By End User

6.2 U.S.

6.2.1 Rutile Market, By Grade

6.2.2 Rutile Market, By Application

6.2.3 Rutile Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping