Oxidation Catalyst Market

Oxidation Catalyst Market Report & Trends Analysis Report, By Type (Precious Metal Catalysts, Base Metal Catalysts, Mixed Metal Oxides), By Application (Automotive, Industrial Processes, Power Generation, Chemical Processing)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

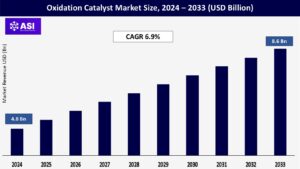

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 6.9%

Last Updated : February 5, 2026

The global Oxidation Catalyst Market size was valued at approximately USD 4.8 billion in 2024 and is projected to reach USD 8.6 billion by 2033, growing at a CAGR of 6.9% during the forecast period.

Oxidation catalysts are specialized materials designed to accelerate oxidation reactions, enabling the conversion of harmful exhaust gases or industrial emissions (such as CO, VOCs, and hydrocarbons) into less harmful compounds like CO₂ and H₂O.

They are critical in emissions control, chemical manufacturing, and process optimization across automotive, industrial, and energy sectors. Growth is driven by stricter emission regulations, expansion of the chemical processing industry, and the global push for cleaner air technologies. Rising demand for sustainable manufacturing and energy-efficient processes further accelerates adoption.

Governments worldwide are enforcing stringent regulations on nitrogen oxides (NOx), carbon monoxide (CO), and volatile organic compound (VOC) emissions from both vehicles and industrial facilities.

Oxidation catalysts play a critical role in catalytic converters, enabling compliance with advanced standards such as Euro 6/7, EPA Tier 3, and China 6. The automotive sector—particularly diesel engine vehicles—relies heavily on these catalysts to meet particulate matter (PM) and CO limits.

In addition, industrial facilities, power plants, and refineries are increasingly adopting oxidation catalysts to meet air quality standards, maintain regulatory compliance, and avoid financial penalties.

Oxidation catalysts are essential in chemical processing for producing acids, aldehydes, and other key intermediates. The rapid growth of petrochemical and specialty chemical sectors in Asia-Pacific, coupled with refinery modernization projects, is driving higher demand for both precious metal-based (platinum, palladium) and non-precious metal catalysts.

Furthermore, rising adoption of low-VOC solvents, green chemistry principles, and waste-to-value technologies is expected to support sustained market growth in the coming years.

Precious metals that are highly volatile in price, such rhodium, palladium, and platinum, are commonly used as oxidation catalysts.

Geopolitical unpredictability, mining restrictions, and a restricted worldwide supply are some of the factors that might cause abrupt price increases that have an immediate effect on end-user pricing and production costs. Producers looking for steady profitability and long-term contracts face difficulties as a result of this cost uncertainty.

Sulfur or phosphorus poisoning, thermal deterioration, and sintering can all cause oxidation catalysts to work less well in high-temperature or contaminant-rich operating conditions.

These problems shorten the catalyst’s lifespan and efficiency, which raises the need for maintenance, regeneration, or total replacement. Adoption in sectors with difficult operating conditions and cost-sensitive applications may be discouraged by such factors.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Precious Metal Catalysts Base Metal Catalysts Mixed Metal Oxides |

| By Application |

Automotive Industrial Processes Power Generation Chemical Processing |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Oxidation Catalyst Market is segmented by Type (Precious Metal Catalysts, Base Metal Catalysts, Mixed Metal Oxides), By Application (Automotive, Industrial Processes, Power Generation, Chemical Processing).

Each factor plays a crucial role in enhancing patient safety, increasing the adoption of self-administered anticoagulant therapies, and supporting the development of more convenient, prefilled drug delivery systems that streamline treatment in the management of thromboembolic and cardiovascular conditions.

Precious Metal Catalysts (Largest Segment)

Because of their exceptional activity, stability, and selectivity in both industrial and automotive applications, oxidation catalysts based on palladium and platinum have the largest market share. To meet strict pollution regulations, they are widely used in diesel oxidation catalysts (DOCs) for automobiles, marine engines, and stationary generators.

Base Metal Catalysts

Catalysts of base metals These catalysts, which are made up of manganese, copper, and cobalt oxides, offer reasonably priced options for particular industrial VOC abatement and chemical synthesis applications. Continuous research and development is increasing their long-term stability and poisoning resistance, which broadens their use in emission control.

Mixed Metal Oxides

These catalysts, which may function without precious metals and have outstanding thermal stability, are becoming more and more popular in industrial pollution control systems. They are appropriate for large-scale operations because to their affordability, especially.

Automotive (Largest Market)

With oxidation catalysts included into exhaust aftertreatment systems for gasoline and diesel engines, the automotive industry (biggest market) represents the largest application segment.

Tighter international pollution standards and the growth of the world’s automobile fleet, which includes passenger automobiles, commercial vehicles, and marine vessels, are driving demand.

Industrial Processes

Industrial Processes: This includes VOC reduction in sectors including printing, food processing, electronics production, and vehicle paint shops. As businesses strive to adhere to regional air quality rules and ISO 14001 environmental management standards, adoption is growing.

Power Generation

Power Generation: Used in stationary generators, gas turbines, and biomass power plants to lower emissions of volatile organic compounds (VOCs) and carbon monoxide (CO). This segment is further supported by rising investments in clean and renewable energy infrastructure.

Chemical Processing

Ammonia oxidation, methanol synthesis, formaldehyde production, and other specialty chemical manufacturing processes all depend on chemical processing. The growth of chemical and petrochemical facilities worldwide, especially in the Middle East and Asia-Pacific, supports demand.

The region leads global production and consumption of oxidation catalysts, with China, India, Japan, and South Korea at the forefront. Rapid industrialization, expanding automotive manufacturing, and stringent air pollution control measures drive demand.

Additionally, the rising adoption of clean coal technologies, biomass plants, and natural gas-based power generation further supports catalyst usage.

Strong adoption in both automotive emission control systems and industrial VOC abatement is driven by stringent EPA regulations and ongoing industrial modernization. The U.S. dominates the regional market, benefiting from advanced automotive manufacturing, extensive refinery capacity, and established environmental compliance infrastructure.

A mature yet highly regulated market, supported by Euro 6/7 automotive emission norms and strict industrial emission directives. Germany, France, and the UK are leaders in adoption and innovation, with a strong presence of catalyst manufacturing companies focusing on sustainable and high-performance solutions.

Moderate but steadily increasing demand, particularly in Brazil, Mexico, Saudi Arabia, and the UAE. Industrial growth, oil & gas sector modernization, and stricter environmental regulations are driving the need for upgraded emission control technologies in these regions.

USD 4.8 billion

6.9%

Precious metal catalysts in automotive applications

Asia-Pacific, driven by rapid industrial growth and stringent emission norms

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Oxidation Catalyst Market, By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Oxidation Catalyst Market, By Application

6.1 North America Oxidation Catalyst Market, By Country

6.1.1 Oxidation Catalyst Market, By Type

6.1.2 Oxidation Catalyst Market, By Application

6.2.1 Oxidation Catalyst Market, By Type

6.2.2 Oxidation Catalyst Market, By Application

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping