L-Glufosinate Ammonium Market

L-Glufosinate Ammonium Market Size, Share & Trends Analysis Report By Form (Liquid, Dry formulations) by Application (Agriculture, Non Crop Applications, Horticulture & Plantation Crops) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

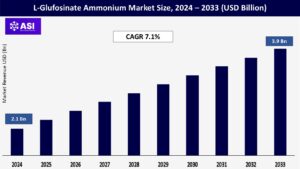

CAGR: 7.1%

Last Updated : March 16, 2026

The global L-Glufosinate Ammonium Market size was valued at approximately USD 2.1 billion in 2024 and is projected to reach USD 3.9 billion by 2033, growing at a CAGR of 7.1% during the forecast period.

L-Glufosinate ammonium is a broad-spectrum, non-selective herbicide widely used for weed control in agricultural and non-agricultural settings. Known for its effectiveness against a wide range of annual and perennial weeds, it is increasingly adopted as an alternative to glyphosate, especially in regions facing herbicide resistance issues and stricter chemical usage regulations.

Growth is driven by the rising demand for high-efficiency herbicides, expansion of genetically modified (GM) glufosinate-tolerant crops, and increasing emphasis on sustainable weed management solutions.

The worldwide agricultural productivity is seriously threatened by the proliferation of glyphosate-resistant weed species. Because of its unique mechanism of action, L-glufosinate ammonium is an essential substitute in integrated weed management (IWM) initiatives.

Agronomists, regulatory agencies, and agricultural extension services are increasingly advocating for its use to impede the development of resistance, especially in high-value crops, including fruits, vegetables, and specialty grains.

Growth of Genetically Modified Glufosinate-Tolerant Plants. The demand for the herbicide has significantly expanded worldwide as a result of the commercialization of glufosinate-resistant genetically modified (GM) crop varieties.

Adoption rates are especially high in the United States, Brazil, and Canada, where the production of glufosinate-tolerant cotton, maize, and soybeans has grown quickly, allowing for less mechanical tillage and more effective broad-spectrum weed control.

Widespread adoption is being hampered by stricter environmental restrictions and maximum residue limits (MRLs) in several markets. Ecotoxicity and soil persistence are the main topics of regulatory evaluations in the EU and several regions of Asia, which may limit use in delicate agricultural areas.

Producing high purity Lglufosinate ammonium necessitates sophisticated synthesis and purification procedures, which frequently call for significant energy inputs and specific catalysts. Price competitiveness is a major obstacle, particularly when compared to less expensive herbicide alternatives, as these variables increase overall production costs.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Form |

Liquid Dry formulations |

| By Application |

Agriculture Non Crop Applications Horticulture & Plantation Crops |

| Key Players |

BASF SE UPL Ltd. Nufarm Limited Zhejiang Yongnong Chem. Jiangsu Sevencontinent Green Chemical Co., Ltd. SinoHarvest Corp. |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The L-Glufosinate Ammonium Market is segmented by Form (Liquid, Dry formulations) by Application (Agriculture, Non Crop Applications, Horticulture & Plantation Crops).

Each factor plays a crucial role in enhancing patient safety, increasing the adoption of self-administered anticoagulant therapies, and supporting the development of more convenient, prefilled drug delivery systems that streamline treatment in the management of thromboembolic and cardiovascular conditions.

Liquid (Largest Segment)

Because of its quick absorption by target weeds, even coverage, and ease of administration, the liquid formulation dominates the market. It is the go-to option for large scale commercial farming since it works with common spraying equipment and may be combined with other herbicides in tank blends. Particularly common are liquid formulations in areas like North America, Brazil, and Australia where row crops are grown intensively.

Dry formulations

which are preferred for their extended shelf life, less storage needs, and cheaper shipping costs, include wettable powders and water-dispersible granules.

In areas with inadequate infrastructure for handling liquids or where prolonged storage without deterioration is essential, dry versions are more common. Smallholder farmers in developing markets also favor them because of their low cost and ease of distribution.

Agriculture (Largest Segment)

Lglufosinate ammonium is mostly used in crop protection, namely to suppress grassy and broadleaf weeds in the production of sugar beet, soybean, maize, cotton, and canola.

It is extensively used in genetically modified (GM) and conventional crop systems, particularly in regions where glyphosate resistance is a problem. It is perfect for pre-plant, post-emergence, and pre-harvest weed control due to its non-selective, contact herbicide qualities.

NonCrop Applications

Used in industrial weed control, forestry, and the upkeep of public areas like parks, railroads, and roadways. It is a good option for environmentally sensitive locations since it effectively suppresses invasive plant species without generating long-term soil persistence.

Horticulture & Plantation Crops

Used to produce decorative plants, control weeds in orchards, vineyards, and tea plantations. Its worth in these high-value agricultural sectors is increased by its capacity to eradicate weeds without harming woody perennial crops.

China, India, Japan, and Australia dominate consumption due to expanding agricultural acreage, rising incidences of herbicide-resistant weeds, and increasing adoption of glufosinate-tolerant GM crops in certain countries. Government support for modern crop protection technologies and the rapid expansion of horticulture and plantation crop production further boost demand.

The U.S. and Canada have strong adoption rates, driven by high GM crop penetration in soybeans, maize, and canola, along with integrated weed management programs. Widespread glyphosate resistance in key agricultural regions has accelerated glufosinate usage as a complementary herbicide.

A more mature market with moderate growth, shaped by strict environmental regulations and a push toward sustainable farming practices. Farmers increasingly integrate L-glufosinate ammonium into precision agriculture systems and targeted weed control programs to meet EU sustainability goals.

Brazil and Argentina are witnessing strong demand growth, particularly in soybean and maize production. In the GCC, adoption is primarily in landscaping, infrastructure maintenance, and non-agricultural weed control due to its effectiveness and relatively low soil persistence.

The current L-Glufosinate Ammonium market size is USD 2.1 billion in 2024.

The L-Glufosinate Ammonium market is expected to grow CAGR of 7.1% from 2025 to 2033.

Liquid formulations dominates the market.

Asia-Pacific shows the highest growth potential.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 L-Glufosinate Ammonium Market, By Form

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 L-Glufosinate Ammonium Market, By Application

6.1 North America L-Glufosinate Ammonium Market, By Country

6.1.1 L-Glufosinate Ammonium Market, By Form

6.1.2 L-Glufosinate Ammonium Market, By Application

6.2.1 L-Glufosinate Ammonium Market, By Form

6.2.2 L-Glufosinate Ammonium Market, By Application

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping