Industrial Water Treatment Chemicals Market

Industrial Water Treatment Chemicals Market Share & Trends Analysis Report, By Type (Coagulants & Flocculants, Corrosion Inhibitors, Scale Inhibitors, Biocides & Disinfectants, Chelating Agents), By End-Use Industry (Generation of Power, Petrochemical and Chemical, Food and Drink, Mining, Paper and Pulp, Other People), By Treatment Type (Treatment of Boiler Water, Treatment of Cooling Water, Treatment of Raw Water)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

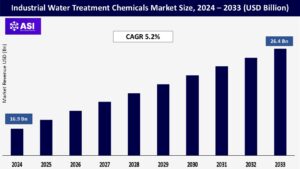

CAGR: 5.2%

Last Updated : March 16, 2026

The global Industrial Water Treatment Chemicals Market size was valued at approximately USD 16.9 billion in 2024 and is projected to reach USD 26.4 billion by 2033, growing at a CAGR of 5.2% during the forecast period (2025–2033).

These chemicals are critical for optimizing the performance and longevity of water systems across industrial facilities by removing contaminants, preventing scaling and corrosion, and maintaining operational efficiency.

Stringent regulatory standards, industrial expansion in emerging markets, and growing water scarcity are among the key factors driving market demand. Moreover, companies are focusing on advanced water treatment programs to reduce downtime, improve energy efficiency, and comply with environmental mandates.

The need for process and utility water is rapidly increasing in emerging nations due to rapid industrial growth, particularly in the manufacturing, petrochemical, and power generation sectors. At the same time, growing urban populations are putting pressure on municipal systems to efficiently treat wastewater and provide clean water.

These factors are speeding up the usage of treatment chemicals to guarantee water quality and reuse, especially in fracking activities that require a lot of water.

Tighter regulations on wastewater disposal, reuse, and chemical composition are being enforced by international regulatory agencies. Operators are being pushed to use more sophisticated and ecologically friendly treatment chemicals by standards established by organizations like the Central Pollution Control Board (CPCB) in India, the Registration, Evaluation, Authorization and Restriction of Chemicals (REACH) in Europe, and the U.S. Environmental Protection Agency (EPA).

This is particularly critical in hydraulic fracturing, where water management is under increasing environmental scrutiny.

Implementing cutting-edge water treatment technologies, like zero-liquid discharge (ZLD) solutions, real-time monitoring systems, and high-performance chemical formulations, frequently requires a substantial capital investment.

For small and medium-sized businesses (SMEs), this can be a major obstacle, particularly in sectors where prices are tight. Due to a lack of funding, these operators would resort to traditional or less-than-ideal treatment techniques, which would hinder the adoption of creative alternatives.

While maintaining fluid quality and avoiding operational problems requires the use of water treatment chemicals, some types—specifically, coagulants, corrosion inhibitors, and biocides—may be harmful to aquatic ecosystems and human health if improperly handled.

Traditional chemical suppliers are under pressure to reformulate or phase out several commonly used chemicals as a result of growing public awareness and regulatory scrutiny, which is fueling demand for greener, biodegradable alternatives.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Coagulants & Flocculants Corrosion Inhibitors Scale Inhibitors Biocides & Disinfectants Chelating Agents |

| By End-Use Industry |

Generation of Power Petrochemical and Chemical Food and Drink Mining Paper and Pulp Other People |

| By Treatment Type |

Treatment of Boiler Water Treatment of Cooling Water Treatment of Raw Water |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Industrial Water Treatment Chemicals Market is segmented by Type (Coagulants & Flocculants, Corrosion Inhibitors, Scale Inhibitors, Biocides & Disinfectants, Chelating Agents), By End-Use Industry (Generation of Power, Petrochemical and Chemical, Food and Drink, Mining, Paper and Pulp, Other People), By Treatment Type (Treatment of Boiler Water, Treatment of Cooling Water, Treatment of Raw Water).

Each factor plays a crucial role in enhancing patient safety, increasing the adoption of self-administered anticoagulant therapies, and supporting the development of more convenient, prefilled drug-delivery systems that streamline treatment for thromboembolic and cardiovascular conditions.

Coagulants & Flocculants

These chemicals are vital for removing suspended solids and particulate matter from water during the sedimentation and clarification stages. They help aggregate fine particles into larger flocs, improving water clarity and treatment efficiency.

Corrosion Inhibitors

Corrosion inhibitors are used to protect metal surfaces in pipelines, heat exchangers, and cooling systems from degradation due to water and oxygen exposure. Their use helps extend equipment life and minimize maintenance costs.

Scale Inhibitors

These agents prevent the formation of mineral scale deposits, such as calcium carbonate or sulfate salts, which can clog pipelines, reduce heat transfer efficiency, and impair flow rates in water systems.

Biocides & Disinfectants

Biocides are essential for controlling microbial growth, including bacteria, fungi, and algae, which can otherwise lead to biofouling, corrosion, or contamination of treated water. They ensure biological stability in both process and wastewater systems.

Chelating Agents

Chelating agents bind to metal ions such as calcium, magnesium, and iron, preventing them from forming scale or interfering with treatment processes. They are also used to enhance cleaning effectiveness in industrial systems.

Generation of Power

The greatest end-use segment is the power industry, which is fueled by significant water use in boilers, steam generation, and cooling systems. Maintaining thermal efficiency, avoiding scaling, and minimizing corrosion in high-pressure equipment all depend on maintaining water quality.

Petrochemical and Chemical

In order to guarantee process stability, safety, and product purity, water treatment is essential in this industry. To control complicated water streams and avoid fouling, scaling, or contamination in reactors and heat exchangers, high-performance treatment chemicals are needed.

Food and Drink

In the production of food and beverages, water purity is crucial since it has a direct impact on product safety, flavor, and legal compliance. Treatment chemicals are used to guarantee the quality of drinkable water and to uphold hygienic requirements during cleaning procedures.

Mining

Water is essential to the mining sector for dust control, slurry transportation, and ore processing. Particularly in areas with water scarcity or pollution issues, water treatment is essential for both operational effectiveness and adherence to environmental discharge standards.

Paper and Pulp

For pulping, bleaching, washing, and equipment cleaning, this industry uses a lot of water. To increase water reuse, safeguard equipment, and reduce environmental discharge, proper water treatment is crucial.

Other People

This group include sectors including metal processing, textiles, and pharmaceuticals, all of which need specialized water treatment systems to guarantee product quality, operational effectiveness, and regulatory compliance.

Treatment of Boiler Water

Precise chemical conditioning is necessary for boiler water to avoid scaling, corrosion, and carryover, which can harm machinery and lower efficiency. In order to preserve boiler performance and integrity, treatment chemicals like pH adjusters, scale inhibitors, and oxygen scavengers are frequently utilized.

Treatment of Cooling Water

The corrosion, scaling, and biofouling that cooling systems are susceptible to can reduce the effectiveness of heat exchange and encourage the growth of microorganisms. For systems to last a long time and function at their best thermally, chemical treatments such as dispersants, corrosion inhibitors, and biocides are necessary.

Treatment of Raw Water

Before being used in industrial operations, raw water is pre-treated to remove dissolved minerals, organic pollutants, and suspended particles. To make sure the water satisfies the quality requirements needed for certain applications, coagulants, flocculants, and filtration aids are used.

Asia-Pacific Due to the fast industrial growth in nations like China, India, and Southeast Asia, Asia-Pacific has the greatest market share. The need for water treatment chemicals is rising sharply as a result of government-led programs encouraging water conservation, reuse, and the recycling of industrial effluent. Growing populations and urbanization also increase the need for water treatment.

Technologically advanced industries, particularly in the US and Canada, are driving the North American market. The extensive use of automated water treatment technologies and strict environmental restrictions are advantageous to the area. Consistent market expansion is also supported by the existence of well-known chemical manufacturers and advancements in environmentally friendly formulations.

Europe is a developed market with a significant trend toward environmentally friendly and sustainable water treatment methods. Leading nations in the adoption of environmentally friendly technologies and circular water usage practices include Germany, France, and the United Kingdom. The switch to low-toxicity chemicals is further promoted by regulatory frameworks like REACH.

Industries in Brazil, Mexico, and Argentina are modernizing water treatment infrastructure, especially in food, mining, and petrochemicals.

The region faces chronic water scarcity, leading to a high reliance on desalination and water recycling. Countries like Saudi Arabia, the UAE, and South Africa are investing heavily in high-performance water treatment chemicals to support water-intensive sectors such as oil & gas, power generation, and municipal utilities

The industrial water treatment chemicals market was valued at USD 16.9 billion.

The projected CAGR of industrial water treatment chemicals market is 5.2%.

The dominant end-use segment of industrial water treatment chemicals market is Power Generation.

The Asia-Pacific and Middle East & Africa region is expected to witness fastest growth in industrial water treatment chemicals market.

Ecolab, BASF, Kemira, Solenis, Suez, Dow, SNF Group.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Industrial Water Treatment Chemicals Market, By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Industrial Water Treatment Chemicals Market, By End-Use Industry

5.3 Industrial Water Treatment Chemicals Market, By Treatment Type

6.1 North America Industrial Water Treatment Chemicals Market , By Country

6.1.1 Industrial Water Treatment Chemicals Market, By Type

6.1.2 Industrial Water Treatment Chemicals Market, By End-Use Industry

6.1.3 Industrial Water Treatment Chemicals Market, By Treatment Type

6.2 U.S.

6.2.1 Industrial Water Treatment Chemicals Market, By Type

6.2.2 Industrial Water Treatment Chemicals Market, By End-Use Industry

6.2.3 Industrial Water Treatment Chemicals Market, By Treatment Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping