Space propulsion systems Market

Space Propulsion Systems Market Size, Share & Trends Analysis Report by Propulsion Type (Chemical, Electric), by Application (Satellite, Launch Vehicle, Deep Space), by Component (Thrusters, Propellant Tanks, Power Processing Units), by End-User (Commercial, Government & Military), by Region – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

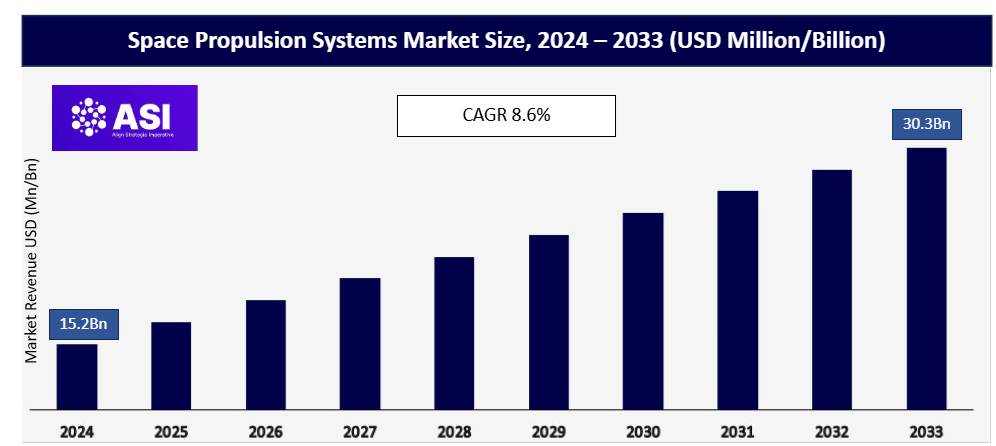

CAGR: 8.6%

Last Updated : April 2, 2026

The space propulsion systems market is experiencing significant market growth due to the increasing demand for satellite launches and advancements in propulsion technology. In 2024, the space propulsion systems market size was valued at USD 15.2 billion and is projected to reach USD 30.3 billion by 2033, with a CAGR of 8.6%. Space propulsion systems are crucial for maneuvering satellites and spacecraft, providing the necessary thrust to navigate in space. They are used in various applications, including communication, earth observation, and scientific missions. The space propulsion systems market size is driven by the rising number of satellite constellations being deployed for global internet coverage and the exploration of deep space missions. As the demand for efficient and eco-friendly propulsion systems grows, companies are investing in developing innovative technologies, such as electric propulsion and hybrid systems, to meet the industry’s evolving needs. The strong market growth trajectory, combined with increasing private participation and government support, positions the Space Propulsion Systems Market as an attractive investment avenue. Strategic investments aligned with high-growth segments and technological innovation are expected to yield substantial returns over the coming decade.

Market Drivers

Growing Satellite Launches

The space industry is witnessing an unprecedented surge in the number of satellite launches, driven by both commercial and governmental needs. This growth is fueled by the demand for global connectivity, earth observation, and scientific research. Companies like SpaceX and Blue Origin are leading the charge with reusable rockets that reduce launch costs, making space access more feasible for numerous entities. The rise in small satellite constellations, aimed at providing internet to remote areas, is further boosting the market for space propulsion systems. These satellites require efficient propulsion solutions to maintain and adjust their orbits, ensuring optimal performance and coverage.

Advancements in Propulsion Technologies

Technological advancements in space propulsion are significantly impacting the market. Traditional chemical propulsion systems are being complemented by electric propulsion options, which offer higher efficiency and lower fuel consumption. This shift is critical as it allows for longer missions and reduces the weight of the spacecraft, enabling more payload capacity. Companies are exploring hybrid propulsion systems that combine the benefits of both chemical and electric propulsion. Innovations such as ion thrusters and plasma propulsion systems are gaining traction, providing more sustainable and economically viable solutions for long-term space missions.

Market Opportunities

Emergence of New Space Markets

The emergence of new space markets presents significant opportunities for the space propulsion systems industry. As space tourism, asteroid mining, and lunar exploration gain attention, the demand for advanced propulsion systems is expected to rise. These new markets require technologies that are not only efficient but also adaptable to various mission profiles. The development of reusable propulsion systems for space travel and exploration is a promising area, offering cost-effective solutions for frequent space missions. The increasing interest in Mars colonization and deep space exploration further underscores the need for robust and innovative propulsion technologies.

Market Restraints

High Costs of Development

One of the primary challenges facing the space propulsion systems market is the high cost of development and deployment. Creating advanced propulsion technologies involves significant investment in research and development, as well as rigorous testing to ensure reliability and safety. The high costs associated with space missions can be a barrier for new entrants and smaller companies, limiting innovation to well-funded entities. Additionally, the long development cycles and regulatory approvals required for space technologies can delay market entry, impacting the overall growth potential of the industry.

| Report Metric | Details |

|---|---|

| By Propulsion Type |

Chemical, Electric |

| By Application |

Satellite, Launch Vehicle, Deep Space |

| By Component |

Thrusters, Propellant Tanks, Power Processing Units |

| By End-User |

Commercial, Government & Military |

| Key Players |

Aerojet Rocketdyne, SpaceX, Blue Origin, Northrop Grumman, Boeing, Airbus, Safran, Lockheed Martin, Rocket Lab, Thales Group, Moog Inc., OHB SE, IHI Corporation, Mitsubishi Heavy Industries, Sierra Nevada Corporation |

| North America |

U.S., Canada, Mexico |

| Europe |

U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe |

| Asia Pacific |

China, South Korea, Japan, India, Australia, Taiwan, South East Asia, Rest of Asia-Pacific |

| Middle East and Africa |

UAE, Saudi Arabia, South Africa, Rest of MEA |

| South America |

Brazil, Argentina, Chile, Rest of South America |

By Propulsion Type, the market is divided into chemical and electric propulsion systems. Chemical propulsion remains dominant due to its high thrust capability, essential for launch vehicles, despite electric propulsion gaining traction for in-orbit applications due to its efficiency. By Application, satellites represent the largest segment, driven by the boom in communication and earth observation satellites requiring precise orbital adjustments. Launch vehicles also hold a significant market share, propelled by the rise in commercial space activities. By Component, thrusters are the most critical component, as they provide the necessary thrust for maneuvering and altitude adjustments. Propellant tanks and power processing units are also crucial, ensuring the effective storage and management of propulsion resources. By End-User, the commercial sector dominates the market, with a growing number of private companies investing in satellite constellations and launch services. Government and military applications also contribute significantly, focusing on defense satellites and space exploration initiatives.

North America leads the space propulsion systems market, driven by the presence of major players like SpaceX and Aerojet Rocketdyne, as well as significant government investments in space exploration and defense. The U.S. plays a pivotal role with its advanced space infrastructure and continuous innovation in propulsion technologies. Europe is also a key region, with countries like France and Germany contributing to the market through companies like Airbus and Safran, focusing on sustainable space technologies. In Asia-Pacific, China and India are making substantial advancements in space capabilities, investing heavily in launch vehicles and satellite technologies. The Middle East and Africa region is gradually entering the space race, with UAE and Saudi Arabia investing in space programs to diversify their economies. South America, led by Brazil, is exploring satellite technologies to enhance communication and earth observation capabilities, albeit at a smaller scale compared to other regions.

The Space Propulsion Systems Market size was valued at USD 15.2 billion in 2024.

The market is projected to grow at a CAGR of 8.6% from 2025 to 2033.

The satellite application segment leads the market, driven by the increasing number of communication and observation satellites.

North America dominates the market, with significant contributions from the U.S. space industry.

Key players include Aerojet Rocketdyne, SpaceX, Blue Origin, Northrop Grumman, and Boeing.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Space propulsion systems Market, By Propulsion Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Space propulsion systems Market, By Application

5.3 Space propulsion systems Market, By Component

5.4 Space propulsion systems Market, By End-User

6.1 North America Space propulsion systems Market, By Country

6.1.1 Space propulsion systems Market, By Propulsion Type

6.1.2 Space propulsion systems Market, By Application

6.1.3 Space propulsion systems Market, By Component

6.1.4 Space propulsion systems Market, By End-User

6.2 U.S.

6.2.1 Space propulsion systems Market, By Propulsion Type

6.2.2 Space propulsion systems Market, By Application

6.2.3 Space propulsion systems Market, By Component

6.2.4 Space propulsion systems Market, By End-User

6.3 Canada

6.4 Mexico

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Saudi Arabia

9.3 South Africa

9.4 Rest of MEA

10.1 Brazil

10.2 Argentina

10.3 Chile

10.4 Rest of South America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping