Oxygen Therapy Devices Market

Oxygen Therapy Devices Market Share and Trend Analysis, By Technology (Compressed Gas Cylinders, On-site Oxygen Generators, Stationary Concentrators, Portable Concentrators, High-Flow Delivery Systems), By Application (COPD, Asthma, Obstructive Sleep Apnea, Respiratory Distress Syndrome, Cystic Fibrosis, Pneumonia), By End User (Home Healthcare, Hospitals & Clinics, Ambulatory Surgical Centers, Long-Term Care Facilities) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

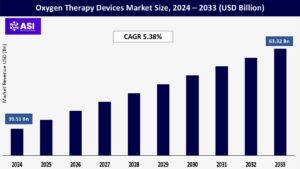

CAGR: 5.38%

Last Updated : April 6, 2026

The global oxygen therapy devices market size was valued at USD 39.51 billion in 2024 and is projected to reach USD 63.32 billion by 2033, expanding at a compound annual growth rate CAGR of 5.38 % during the forecast period (2025–2033).

Oxygen therapy equipment are medical device intended to provide supplemental oxygen to patients with hypoxemia resulting from respiratory conditions, including chronic obstructive pulmonary disease (COPD), asthma, pneumonia, obstructive sleep apnea, and acute respiratory distress syndrome.

The equipment varies from large, fixed oxygen concentrators and compressed oxygen cylinders employed in hospital and home healthcare facilities to portable oxygen concentrators for ambulatory patients that are light and compact.

Delivery interfaces are nasal cannulas, basic masks, non-rebreather masks, and high-flow nasal cannulas, each designed with particular flow-rate specifications and patient comfort in mind. Advances in technology like pulse-dose delivery, wireless communication, remote monitoring and energy-saving systems have improved patient compliance and facilitated care within as well as beyond the confines of conventional clinical settings.

The market is spurred by the growing global population with increasing incidence of chronic respiratory illnesses and by the increasing availability of home-based care.

Furthermore, the rising need for advanced respiratory support in surgical, critical care and emergency departments is driving growth overall, with strict regulatory requirements and the expense of the devices being ongoing limitations to mass adoption.

The global rise in long-term respiratory disease continues to be a pressing issue. Diseases such as chronic obstructive pulmonary disorder affect thousands of people worldwide. Rising older populations, continued exposure to contaminated air, and continued tobacco smoking all exacerbate this problem.

These ailments often lead to critically depleted levels of oxygen in patients’ bloodstreams, necessitating prolonged supplemental oxygen therapy. This treatment makes individuals feel more comfortable and live longer. As a result, oxygen delivery devices are increasingly being bought by hospitals and home care environments.

The recent worldwide health emergency even further highlighted the importance of readily available oxygen stores in times of crisis. The incident compelled medical infrastructures across the globe to significantly improve their oxygen equipment.

Increased awareness among medical practitioners and revised guidelines for using oxygen for prolonged durations indicate demand for various oxygen devices will continue to remain high in the years ahead. Large home use stationary machines, personal portable units, and high-flow sophisticated systems all experience increasing demand.

This chronic health issue continuously drives the marketplace for these essential devices. The sheer volume of individuals impacted guarantees continual investment in respiratory care technologies within medical institutions and private homes.

Premier manufacturers continually invest in research, providing significant advances in oxygen therapy devices. New portable oxygen concentrator generations offer more liberty and mobility for patients that need treatment while on the move.

Smarter devices now have wireless capabilities, allowing medical teams to monitor patient usage habits in real time, ensure proper adherence to therapy regimens, and remotely adjust oxygen administration as needed. This enables very personalized care strategies.

Contemporary nasal cannulae and non-invasive ventilation devices deliver more oxygen in comfortable amounts by providing heat and humidity. These advancements facilitate a significant reduction in respiratory work and overall comfort. Developments to decrease device weight and compactness have led to very portable units with a long battery life.

This enables users to maintain their independence and engage in activities for longer. All these more efficient, intelligent, and easier-to-use innovations together drive market growth and develop new applications in hospital settings and for long-term condition management in the home.

Ongoing improvement is targeted to make equipment less noisy, easier to use, and more reliable. These advances directly enhance patients’ quality of life while receiving necessary respiratory therapy. Combining increased functionality and patient-focused design promotes wider uptake of advanced oxygen solutions.

The high cost of advanced oxygen therapy devices inhibits widespread adoption. Offering obvious medical benefits, the premium initial cost and ongoing maintenance are a costly burden. Big floor units and complex high-flow systems are large expenditures that strain hospital and clinic budgets.

For home patients, particularly in poorer countries, such expense can be prohibitive, leading to hard decisions regarding fundamental care. Equipment maintenance contributes substantially to overall costs. Repeated tasks such as replacement of filters, technical maintenance, and calibration are sources of ongoing expenses.

Such a burden is acutest in areas with scarce healthcare financing and thus makes such equipment difficult to justify even in the face of patient demand. In addition, reimbursement or insurance coverage is highly variable. Some policies provide little support for home oxygen therapy, with patients being forced to bear substantial portions of the expense.

Where family budgets directly pay for medical expenses, this absence of support puts technology that’s needed beyond financial reach. As a result, high-cost devices, ongoing maintenance charges, and unreliable financial aid significantly hinder market expansion.

This holds back advanced solutions for reaching everyone who requires them, especially in environments with limited healthcare resources and high individual health expenditures. The financial barrier forestalls much-needed upgrades and continues disparate access to life-critical breathing assistance.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Compressed Gas Cylinders On-site Oxygen Generators Stationary Concentrators Portable Concentrators High-Flow Delivery Systems |

| By Application |

COPD Asthma Obstructive Sleep Apnea Respiratory Distress Syndrome Cystic Fibrosis Pneumonia |

| By End User |

Home Healthcare Hospitals & Clinics Ambulatory Surgical Centers Long-Term Care Facilities |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Oxygen therapy devices divide into two broad technology categories. The first category consists of devices that produce or store oxygen itself. These source devices range from compressed gas cylinders, on-site oxygen generators that produce gas from room air, to large stationary concentrators intended primarily for home use.

The second category consists of the equipment patients directly use to inhale the oxygen. These delivery devices cover simple low-flow models such as nasal tubes and basic face masks up to powerful high-flow devices such as rebreathing-preventing high-flow nasal cannulas and masks.

There are even specialized delivery devices, such as reservoir masks that contain additional oxygen or catheters directly placed in the windpipe. In the future, the delivery devices segment is expected to remain the biggest segment. It stems from their totally critical role: they are the critical connection delivering oxygen safely from the machine into the lungs of the patient at just the right rate.

Their construction also allows them to function effectively anywhere, from crowded hospital wards to a patient’s living room, so they are a necessity throughout the entire spectrum of the healthcare environment for efficient breathing assistance.

Various respiratory conditions dictate the necessity for oxygen machines. Chronic obstructive pulmonary disease, better known as COPD, is the largest individual cause of individuals requiring this equipment. Its sheer prevalence and the fact that keeping low levels of oxygen in the blood for long periods requires sustained therapy earn its position.

There are other serious conditions that are driving the use of devices, such as asthma and breathing complications caused by allergies, obstructive sleep apnea interrupting night breathing, respiratory distress syndrome in vulnerable newborns, and lung-scarring diseases like cystic fibrosis and interstitial lung disease.

Sudden, severe illnesses like severe pneumonia or severe COVID-19 lung injury also generate heavy, urgent demand for oxygen therapy, particularly in hospitals. All of these medical ailments need stable oxygen delivery to stabilize patients, alleviate breathing difficulties, and avert organ damage.

The needs are specialized—some need constant, lifetime oxygen at home, others need strong, instantaneous assistance in emergency situations but collectively they represent the fundamental medical uses driving the demand for these lifesaving machines.

Oxygen machines find their way to patients through a variety of important care settings. Hospitals and clinics are the biggest group utilizing this equipment. Their prominence is understandable since acute care settings deal with the most serious and diverse breathing emergencies.

They require a full line of devices available at all times for emergencies, surgery and post-operative periods, and in intensive care wards where accurate oxygen control is life-saving. Home care settings are another significant and rapidly increasing segment, fueled by the trend of treating long-term conditions such as advanced COPD in a non-hospital environment.

Patients are increasingly being treated with stationary concentrators or portable devices in their own homes. Ambulatory surgical facilities that perform day procedures that need temporary oxygen therapy and long-term care centers, such as nursing homes treating elderly patients with ongoing breathing problems, are other significant locations utilizing these machines.

Each environment has its unique requirements; hospitals require power and flexibility for life-threatening cases, whereas home care requires simplicity, safety, and independence for the patient. This distribution across environments underlines the importance of oxygen therapy across the entire spectrum of contemporary healthcare provision.

North America dominates the world oxygen therapy market. Its standing arises from the high incidence of chronic respiratory disorders such as COPD among the population and a highly developed home healthcare infrastructure.

It is favored by heavy investment in medical care and extensive insurance coverage policies, allowing advanced oxygen technology to become generally available. Patients and clinicians embrace new stationary and portable equipment backed by established distribution channels and clinical experience.

Europe demonstrates steady market expansion supported by extensive national health services and strict standards for the safety of medical equipment. Growing emphasis on the care of patients outside the hospital propels home oxygen therapy prescriptions.

The population aging and medical strategies designed to reduce hospital re-admissions add stimulus to demand further. These all combine to provide a solid setting for the use of oxygen devices in a variety of care settings.

The Asia Pacific market is growing rapidly with increasing rates of respiratory disease, enhanced availability of healthcare services, and significant investments in home care solutions.

Healthcare systems are evolving, with increased usage of portable concentrators and sophisticated delivery systems to treat both long-term and acute respiratory conditions. Enhanced government initiatives for oxygen supply, especially among rural populations, drive this positive trend.

These developing markets have increasing acknowledgement of the management of chronic respiratory disease and have increased private expenditure on health.

Market expansion is, however, hindered by limited insurance coverage for oxygen therapy, variable quality of medical infrastructure, and the prohibitive cost burden of devices. Collaborations between governments and producers, with local manufacturing initiatives, are strategies designed to enhance access to necessary breathing support devices.

The global Oxygen Therapy Devices Market was valued at USD 39.51 billion in 2024.

The market is projected to grow at a CAGR of 5.38 % from 2025 to 2033.

Chronic Obstructive Pulmonary Disease (COPD) hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Philips Healthcare, Linde Healthcare, Chart Industries, Invacare Corporation, ResMed, Fisher & Paykel Healthcare, Drägerwerk AG & Co., GE Healthcare, Smiths Medical, and CAIRE Inc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Oxygen Therapy Devices Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Oxygen Therapy Devices Market, By Application

5.3 Oxygen Therapy Devices Market, By End User

6.1 North America Oxygen Therapy Devices Market, By Country

6.1.1 Oxygen Therapy Devices Market, By Technology

6.1.2 Oxygen Therapy Devices Market, By Application

6.1.3 Oxygen Therapy Devices Market, By End User

6.2 U.S.

6.2.1 Oxygen Therapy Devices Market, By Technology

6.2.2 Oxygen Therapy Devices Market, By Application

6.2.3 Oxygen Therapy Devices Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping