3D Bioprinting Market

3D Bioprinting Market Share and Trend Analysis, By Technology (Inkjet Based, Syringe Based, Laser Assisted, Magnetic Levitation), By Application (Medical, Dental, Biosensors, Consumer/Personal Product Testing, Bio Inks, Food and Animal Products), By End User (Hospitals and Clinics, Research Laboratories, Pharmaceutical and Biotechnology Companies, Contract Research Organizations) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033.

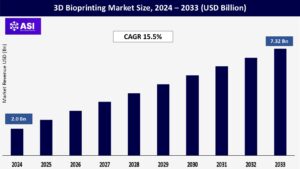

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 15.5%

Last Updated : May 9, 2026

The global 3D bioprinting market was valued at USD 2 billion in 2024 and is projected to reach USD 7.32 billion by 2033, expanding at a compound annual growth rate CAGR of 15.5% during the forecast period (2025 – 2033).

Fundamentally, 3D bioprinting is a cutting-edge fabrication method. It employs expert printers to carefully lay down layers of “bio-inks,” sophisticated mixtures of living cells, supportive biomaterials, and bioactive factors according to a digital plan. This deliberate strategy allows the building of complex, three-dimensional tissue-like patterns. First imagined to push the boundaries of tissue engineering, mainly for repair and replacement, the technology’s vision has grown exponentially. Its core ability to establish biologically meaningful, human-like tissues ex vivo has liberated transformative promise far greater than its beginning. This revolution has been driven by dramatic, concurrent progress over the past decade. Higher printer resolution enables unprecedented cellular accuracy and architectural sophistication.

The creation of an immensely wider range of biocompatible and functional biomaterials enables higher versatility in the mimicry of a wide variety of native tissues. In parallel, advanced software control systems enable higher fidelity recreation of digital designs as well as more reliable processes. These converging technologies have conclusively pushed bioprinting from promising proof-of-concept to genuine utility. Its use now firmly covers key areas such as sophisticated regenerative medicine approaches, very predictive drug discovery and toxicity screening platforms, and ethically robust cosmetic testing models. This path solidly places 3D bioprinting not just as a new methodology, but as an underlying pillar propelling the next revolution in biomedical research and therapeutic development.

Pharmaceutical R&D is being fundamentally revolutionized by the adoption of 3D bioprinting. The central driver is the ability of the technology to produce physiologically relevant human tissue constructs. These tissues, printed in the laboratory, provide an enhanced, human-specific platform for assessing drug candidates, directly targeting the shortcomings and ethical concerns that come with conventional animal testing. By enabling more predictive models of human response, bioprinting profoundly improves the validity of efficacy and toxicity predictions in preclinical phases. This translates directly to shorter development timetables and vast cost savings by catching failure earlier.

The ability to create intricate, vascularized tissues opens up more profound investigation in key therapeutic categories such as oncology and immunology. Noticing this strategic value, large pharmaceutical companies are proactively entering into partnerships with bioprinter companies to jointly develop tailored, application-tailored bioprinting platforms compatible with their drug discovery pipelines. The concrete result is a quantified reduction in failures in late-stage clinical trials, offering impressive proof and spurring greater in-house investment in bioprinting facilities throughout the sector.

Ongoing technological development is a key driver pushing the 3D bioprinting technology forward. Substantial advances in several print modalities – extrusion-based, inkjet, and laser-assisted – provide real-world benefits in resolution, rate of fabrication, and acceptability of a wider variety of biomaterials. At the same time, the emergence of highly advanced, next-generation bio-inks, with individually controlled mechanical properties and higher cell viability, facilitates the production of successively more intricate and realistic tissue structures.

It is driven by high levels of R&D effort across both legacy equipment makers and nimble start-ups, leading to the introduction of next-generation platforms featuring multi-nozzle printheads and onboard real-time monitoring systems for unmatched accuracy. In addition, collaborative partnerships between academia and the commercial world are giving rise to powerful open-source software tools, democratizing access to advanced design optimization and process control functions. These converging technology strides are quickly broadening the scope beyond mere tissue imitations to include complex organ-on-a-chip systems and patient-specified grafts, thereby enabling direct practical application across wider research and clinical use.

The most significant bottleneck limiting the wider adoption of 3D bioprinting is the severe lack of properly qualified people. The discipline necessitates an uncommon, multidisciplinary talent set where a profound understanding of cell biology, biomaterials science, and cutting-edge engineering practices must coexist. Proficiency in the operation of state-of-the-art bioprinters is more than rudimentary technical know-how; qualified experts are needed to design complex, biologically realistic digital models, carefully calibrate multi-axis printing systems, and skillfully develop or modify complex bio-inks specifically for certain cell types and structures. In addition, process consistency continues to be a major obstacle. Variability across equipment platforms, bio-ink batches, and even environmental conditions requires ongoing watchfulness and advanced troubleshooting skills.

Operators need to skillfully diagnose and solve varied problems, from printhead clogging and layer misalignment to unexplained drops in post-printing cell viability – issues that call for simultaneous engineering expertise and biological knowledge. Although specialized academic programs are starting to emerge, they are in their infancy and can currently not yet produce graduates at the scale or depth needed. As a result, research organizations, makers of biprinters, and end-user markets such as the pharma sector experience highly competitive vying for access to a finite talent base. This shortage directly constrains research throughput, retards optimization of protocols, and most critically, keeps one from scaling bioprinting from proofs-of-concept in the laboratory towards reproducible, standardized manufacturing for therapeutic or large-scale industrial use, e.g., high-volume drug screening.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Inkjet-Based Syringe-Based Laser-Assisted Magnetic Levitation

|

| By Application |

Medical Dental Biosensors Consumer/Personal Product Testing Bio-Inks Food and Animal Products

|

| By End User |

Hospitals and Clinics Research Laboratories Pharmaceutical and Biotechnology Companies Contract Research Organizations

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

3D bioprinting reaches beyond tissue creation to advanced drug delivery. Scaffold-based systems are a key segment, wherein bio-inks containing biodegradable polymers create porous matrices that encapsulate and control the release of therapeutic agents. Cell-laden bio-assemblies form another segment; in this case, printed living cells actively secrete therapeutic proteins on extended durations, providing dynamic delivery platforms. A fast-growing segment utilizes composite bio-inks, which combine natural polymers with nanoparticles or liposomes to provide highly localized, stimulus-responsive release profiles.

This technology division highlights the platform’s versatility: it makes implantable drug depots for local therapy, constructs pre-loaded tumor models for testing efficacy, and designs tailored delivery vehicles. Ongoing advances in biomaterials science, especially in bio-ink design with improved biocompatibility and adjustable degradation kinetics, are anticipated to further diversify these segments. This evolution holds the promise of major advances in customized therapeutic approaches, particularly in complex areas such as oncology (targeted cancer treatments) and endocrinology (prolonged hormone delivery), going beyond passive carriers to active, intelligent delivery systems.

3D bioprinting application segments encompass clinical and non-clinical arenas. In regenerative medicine, it prints patient-specific tissue grafts (dermis, cartilage, bone) for wound healing and organ reconstruction with the potential to recover function. Pharmaceutical research is a key segment, employing printed, physiologically relevant tissue models (e.g., liver, heart) for very predictive drug screening, toxicity evaluation, and disease modeling, far surpassing conventional 2D cell cultures. The cosmetic and food sectors represent an emerging segment, investigating bioprinted human skin equivalents for safety testing and edible meat alternatives to minimize animal use and maximize sustainability.

Educational institutions use the technology to create precise anatomical models and models for biological education and surgical training. One key trend is the scope expansion: uses are shifting from research-based tools to translational and commercially profitable products. Demand is especially increasing for patient-specific medical solutions and highly predictive models in drug development, securing bioprinting’s position as a convenient, multidisciplinary platform that connects laboratory innovation with real-world healthcare, industrial, and educational demands.

Hospitals and clinics mostly use bioprinting for point-of-care, with an emphasis on developing patient-specific anatomical models for surgical planning as well as custom implants or grafts to enhance procedural outcomes and recovery. Research and industrial academic laboratories are a central segment, utilizing the technology for basic biological research, disease mechanism studies, and highly stringent preclinical testing of therapeutics and materials, often closely working with bioprinter vendors. The pharmaceutical and biotechnology segments are a key driving segment, incorporating bioprinted tissue models into high-throughput drug discovery pipelines, toxicity screening, and sophisticated formulation development to drive greater efficiency and prediction.

Contract research organizations (CROs) and proprietary biomanufacturing service providers provide tissue model printing as a service for customers without in-house capability. Both classes have different requirements: clinical environments require strict regulatory compliance (GMP/GTP) and sterility assurance; academic researchers value experimental flexibility and access to new methodologies; industrial consumers value reproducibility, scalability, and transparent integration into current R&D processes. This diversity feeds ongoing, application-driven innovation throughout the entire bioprinting community.

North America dominates, propelled by superb R&D investment, top-tier academic-medical centers, and a high concentration of bioprinter innovators (Organovo, Aspect Biosystems) and end-users. Active FDA pilot programs enable clinical translation, and specialized biomanufacturing facilities drive feasibility studies. Venture capital investment supports strong startups, and regular industry-academia partnerships speed innovation. Breakthroughs, such as patient-specific implants, prove clinical utility. Strong healthcare infrastructure facilitates validation and adoption. This environment—uniting regulatory forward thinking, access to capital, and technology expertise solidifies the region’s leadership in creating and commercializing next-generation bioprinting technologies for research and therapy.

Europe’s progress is driven by the EU’s prohibition on cosmetics animal testing, generating pressing demand for human-relevant bioprinted models. Friendly Advanced Therapy Medicinal Product (ATMP) regulations offer routes for clinical adoption. Leading consortia (Germany, UK, Netherlands) and firms (CELLINK) drive printer and bio-ink innovation. Collaborative EU funding (Horizon Europe) accelerates standardization and complex tissue development. Strict medical device regulations (MDR) ensure safety frameworks. The region’s strong ethical research focus and sustainability goals align with bioprinting’s potential, boosting its use in pharma testing and regenerative medicine across academia and industry.

APAC is the most rapidly growing market, driven by government programs (China’s “Made in China 2025,” Japan’s regenerative medicine fast-tracks). The growth of healthcare investment aims at bioprinting commercialization. High patient base and interest in regenerative therapies accelerate hospital/research uptake. Domestic startups (Cyfuse, Pandorum) create cost-efficient systems, while collaboration with Western companies propels technology transfer. Growth in research infrastructure in China, Japan, India, and South Korea underpins innovation. This government-supported drive, complemented by clinical need and rising regional manufacturing capacity, makes APAC a pivotal future growth driver for research and therapeutic uses.

These markets are displaying early potential, centered in academic institutions (e.g., University of São Paulo), investing in foundational research. Drivers here are minimizing dependence on medical models imported from elsewhere and participating in international partnerships. Despite this, constrained infrastructure, low funding, and severe skills shortages limit scaling. Poorly developed regulatory channels for bioprinted goods offer further hindrances. Future adoption depends on more stringent animal testing regulations, higher healthcare modernization budgets, and continued knowledge transfer through international collaborations. Expansion remains incremental, focused on region-specific solutions where cost and infrastructure limitations can be surmounted.

The global 3D bioprinting market was valued at USD 2 billion in 2024.

The 3D bioprinting market is projected to grow at a CAGR of 15.5% from 2025 to 2033.

The Extrusion hold the largest 3D bioprinting market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Organovo Holding Inc., Luxexcel Group B.V., TeVido BioDevices LLC, 3Dynamics Systems Ltd., Cyfuse Biomedical K.K., Aspect Biosystems Ltd., Stratasys, Voxeljet A.G., Bio3D Technologies Pte. Ltd., Materialise N.V., Envision TEC.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 3D Bioprinting Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 3D Bioprinting Market, By Application

5.3 3D Bioprinting Market, By End User

6.1 3D Bioprinting Market, By Country Type

6.1.1 3D Bioprinting Market, By Technology

6.1.2 3D Bioprinting Market, By Application

6.1.3 3D Bioprinting Market, By End User

6.2 U.S.

6.2.1 3D Bioprinting Market, By Technology

6.2.2 3D Bioprinting Market, By Application

6.2.3 3D Bioprinting Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping