3D Medical Imaging Market

3D Medical Imaging Market Share & Trends Analysis Report, By Modality / Device Type (X‑Ray, CT, MRI, Ultrasound, Hybrid Imaging), By Component (Hardware, Software, Services (e.g., 3D Scanning, Rendering, Modeling)), By Application (Oncology, Cardiology, Orthopedics, Obstetrics & Gynecology, Neurology, Others), By End‑User (Hospitals, Diagnostic Imaging Centers, Research Institutes, Other Healthcare Providers), By Deployment / Platform (On‑Premise, Cloud‑Based, Web‑Based) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

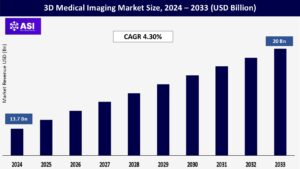

CAGR: 4.30%

Last Updated : December 3, 2025

The global 3D Medical Imaging Market size was valued at approximately USD 13.7 billion in 2024 and is projected to reach USD 20 billion by 2033, growing at a CAGR of 4.30% during the forecast period (2025–2033).

The 3D Medical Imaging Market, on the other hand, involves technologies that create three-dimensional visual representations of internal body structures using modalities such as MRI (Magnetic Resonance Imaging), CT (Computed Tomography), ultrasound, PET (Positron Emission Tomography), and 3D mammography.

These systems are extensively used in diagnosing, planning, and monitoring a wide range of conditions, including cancer, neurological disorders, musculoskeletal injuries, and vascular diseases. The key properties of 3D imaging systems include high-resolution visualization, depth perception, and the ability to rotate and reconstruct images from multiple angles, providing a comprehensive view of anatomical structures.

This enables earlier and more accurate diagnoses, better surgical planning, and improved treatment outcomes. Technological advancements such as AI-based image reconstruction, real-time rendering, and integration with robotic surgery and telemedicine platforms are further driving demand. Together, both markets underscore the healthcare industry’s shift toward precision diagnostics, preventive care, and patient-centric solutions.

Early detection and precise visualization of diseases are crucial for effective treatment planning, particularly in oncology, neurology, and orthopedics. 3D medical imaging technologies, such as 3D MRI, CT, and PET scans, allow clinicians to view organs and tissues in high resolution and from multiple angles, enabling better assessment of abnormalities like tumors, fractures, or vascular lesions.

This leads to quicker clinical decisions, more targeted therapies, and improved patient outcomes. As health systems globally shift toward value-based care, the demand for advanced diagnostic tools that support early intervention continues to rise.

Artificial Intelligence (AI) is transforming 3D medical imaging by enhancing image reconstruction speed, improving diagnostic accuracy, and reducing interpretation errors. AI algorithms can analyze thousands of images rapidly, detect subtle patterns missed by the human eye, and provide decision support for radiologists.

Additionally, AI-enabled imaging systems can reduce radiation exposure and shorten scan times. The integration of AI with 3D imaging is being widely adopted in hospitals and diagnostic centers, driving market growth by increasing efficiency, improving workflow, and enabling personalized medicine.

3D medical imaging systems such as 3D MRI, CT, and PET scanners involve significant upfront investment in terms of procurement, installation, and facility setup. Advanced imaging equipment can cost millions of dollars, and requires dedicated space, shielding infrastructure, and climate control. Moreover, the operation and maintenance of these systems demand highly skilled personnel, regular calibration, and costly service contracts, all of which add to the total cost of ownership.

These financial barriers limit the adoption of 3D imaging technology, particularly in small hospitals, diagnostic labs, and rural healthcare settings, where budget constraints and infrastructure limitations are common. As a result, the high cost restricts widespread deployment and contributes to regional disparities in access to advanced imaging.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Modality / Device Type |

X‑Ray CT MRI Ultrasound Hybrid Imaging |

| By Component |

Hardware Software Services (e.g., 3D Scanning, Rendering, Modeling) |

| By Application |

Oncology Cardiology Orthopedics Obstetrics & Gynecology Neurology Others |

| By End-User |

Hospitals Diagnostic Imaging Centers Research Institutes Other Healthcare Providers |

| By Deployment / Platform |

On‑Premise Cloud‑Based Web‑Based |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The 3D Medical Imaging Market is segmented by Modality / Device Type, Component, Application, End User and Deployment / Platform. Each factor influencing the growth of the 3D Medical Imaging Market contributes significantly to improving diagnostic precision, treatment planning, and patient outcomes across a wide range of medical specialties.

The shift toward high-resolution, multi-angle imaging enhances clinicians’ ability to visualize complex anatomical structures and detect abnormalities at earlier stages. Moreover, the integration of AI and automation not only streamlines workflow but also supports more personalized and data-driven care.

The market includes X-ray, Computed Tomography (CT), Magnetic Resonance Imaging (MRI), Ultrasound, and Hybrid Imaging systems. CT and MRI dominate the market due to their ability to provide highly detailed, multi-plane images of internal organs and tissues, essential in diagnosing complex conditions.

3D ultrasound is gaining traction in obstetrics, cardiology, and emergency medicine for its non-invasive, real-time imaging capabilities. X-ray imaging remains widely used due to its cost-effectiveness and broad applications in orthopedics and chest imaging, while hybrid imaging technologies such as PET/CT and PET/MRI are revolutionizing cancer diagnostics by combining anatomical and functional imaging in a single scan.

The market is divided into Hardware, Software, and Services (including 3D scanning, rendering, and modeling). Hardware comprises the physical imaging systems and accounts for a large share of the market due to their critical role in capturing high-resolution images.

However, software solutions—which include 3D reconstruction, visualization, and AI-driven analysis—are rapidly expanding, enabling enhanced interpretation, workflow automation, and image sharing across platforms.

Services such as rendering and 3D modeling are becoming increasingly valuable in surgical planning, prosthetic design, and educational visualization, contributing to improved precision and personalized treatment approaches.

The market includes Oncology, Cardiology, Orthopedics, Obstetrics & Gynecology, Neurology, and Others. Oncology holds the largest share due to the growing global cancer burden and the critical need for early and accurate tumor localization, staging, and treatment monitoring.

Cardiology benefits from 3D imaging to assess structural heart diseases and guide interventional procedures. In orthopedics, 3D imaging aids in diagnosing fractures, joint abnormalities, and planning surgeries.

Obstetrics & gynecology utilizes 3D ultrasound for fetal development tracking, while neurology relies heavily on 3D MRI and CT scans to detect stroke, tumors, and degenerative diseases.

The market is segmented into Hospitals, Diagnostic Imaging Centers, Research Institutes, and Other Healthcare Providers. Hospitals are the leading adopters of 3D imaging technologies due to their broad patient base, multidisciplinary applications, and access to capital investment.

Diagnostic imaging centers are growing rapidly, especially in urban areas, offering outpatient services with fast turnaround and high-quality diagnostics. Research institutes use advanced 3D imaging for clinical trials, anatomical studies, and innovation in AI-integrated medical imaging. Other healthcare providers, such as specialty clinics and mobile units, are increasingly integrating portable 3D imaging for remote and point-of-care diagnostics.

The market is categorized into On-Premise, Cloud-Based, and Web-Based solutions. On-premise systems are common in large hospitals and facilities with in-house IT infrastructure and data storage capabilities.

However, cloud-based platforms are witnessing rapid growth due to their scalability, remote access capabilities, lower upfront costs, and ease of integration with telemedicine services.

Web-based deployment models are gaining popularity for their flexibility, browser accessibility, and ease of use in multi-location healthcare networks and collaborative diagnostics.

Leads the 3D Medical Imaging Market due to its advanced diagnostic infrastructure, strong presence of global imaging companies, and early adoption of AI-integrated imaging platforms.

The United States dominates with large-scale use of MRI, CT, and PET/CT in oncology, neurology, and orthopedics, supported by high healthcare spending and ongoing innovation in imaging software and cloud platforms. Canada is also seeing steady growth due to national investments in imaging research and digitization of healthcare services.

Holds a substantial share, with Germany, the UK, France, and Italy being key contributors. The region benefits from comprehensive public healthcare systems, high imaging volumes, and increased demand for precision diagnostics.

EU-wide initiatives like Horizon Europe and digital health integration policies are enhancing the use of 3D imaging tools for both clinical and research applications. However, regulatory complexity and budget constraints in some Eastern European countries may limit uniform growth across the continent.

A rapidly expanding market, fueled by increased healthcare expenditure, growing chronic disease prevalence, and improved access to diagnostic facilities. Japan leads in advanced imaging use, while China is investing heavily in AI-powered imaging and expanding radiology infrastructure across Tier 1 and Tier 2 cities.

India is also growing, driven by government-backed screening programs and public-private partnerships aimed at boosting diagnostic access. Increasing medical tourism and urban healthcare expansion further support growth across the region.

Shows steady development, particularly in Brazil, Argentina, and Chile, where hospitals are upgrading imaging facilities and adopting digital radiology systems. Nonetheless, overall market penetration is hindered by economic fluctuations, healthcare inequality, and a lack of trained radiologists in some rural and semi-urban areas.

countries like Saudi Arabia, UAE, and South Africa are leading adoption due to healthcare reforms, expanding hospital networks, and strategic investments in diagnostic imaging. The growing prevalence of cancer and neurological disorders is prompting the adoption of 3D imaging technologies.

However, large parts of Africa still face challenges due to poor infrastructure, limited budgets, and lack of skilled professionals, which restrict widespread deployment.

The 3D Medical Imaging market was valued at USD 13.7 billion in 2024.

The market is projected to grow at a CAGR of 4.30% from 2025 to 2033.

X‑Ray hold the largest market share.

The North America region is expected to witness the highest growth rate.

Major players include GE Healthcare, Siemens Healthineers and Philips Healthcare

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 3D Medical Imaging Market, By Modality / Device Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 3D Medical Imaging Market, By Component

5.3 3D Medical Imaging Market, By Application

5.4 3D Medical Imaging Market, By End‑User

5.5 3D Medical Imaging Market, By Deployment / Platform

6.1 North America 3D Medical Imaging Market , By Country

6.1.1 3D Medical Imaging Market, By Modality / Device Type

6.1.2 3D Medical Imaging Market, By Component

6.1.3 3D Medical Imaging Market, By Application

6.1.4 3D Medical Imaging Market, By End‑User

6.1.5 3D Medical Imaging Market, By Deployment / Platform

6.2 U.S.

6.2.1 3D Medical Imaging Market, By Modality / Device Type

6.2.2 3D Medical Imaging Market, By Component

6.2.3 3D Medical Imaging Market, By Application

6.2.4 3D Medical Imaging Market, By End‑User

6.2.5 3D Medical Imaging Market, By Deployment / Platform

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping