Advanced Wound Dressing Market

Advanced Wound Dressing Market Share & Trends Analysis Report, By Product Type (Moist Wound Dressings, Antimicrobial Dressings, Active Wound Care), By Application Type (Chronic Wounds, Acute Wounds), By End-User (Hospitals, Home Healthcare, Specialty Clinics, Ambulatory Surgical Centers (ASCs))– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

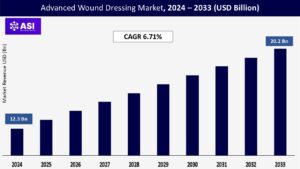

CAGR: 6.71%

Last Updated : January 21, 2026

The global advanced wound dressing market size was valued at approximately USD 12.3 billion in 2024 and is projected to reach USD 20.2 billion by 2033, demonstrating a compound annual growth rate (CAGR) of 6.71% during the forecast period of 2025–2033.

The advanced wound dressing market is an evolving and increasingly vital part of the healthcare industry, marked by the use of cutting-edge materials and technologies designed to support faster, more effective healing. These dressings go beyond traditional bandages, offering solutions that help manage complex wounds, reduce the risk of infection, and improve overall patient care—especially for those dealing with chronic conditions like diabetes or pressure ulcers.

With a growing focus on improving outcomes and quality of life for patients, the demand for advanced wound care products is on the rise. From 2024 to 2033, the market is expected to see strong and sustained growth, driven by innovations in healthcare, an aging population, and a greater emphasis on personalized, efficient wound management solutions.

One of the most powerful forces driving the advanced wound dressing market is the growing global burden of diseases that lead to complex, slow-healing wounds. As chronic health conditions such as diabetes, obesity, and vascular diseases become more prevalent worldwide, the number of patients suffering from chronic wounds is rising sharply. Diabetic foot ulcers (DFUs), for example, are a direct consequence of poorly managed diabetes and are notoriously difficult to heal, often requiring long-term, specialized care with advanced wound dressings. Similarly, pressure ulcers also known as bedsores are becoming more common as the global elderly population grows and more individuals face mobility challenges or spinal cord injuries. Venous leg ulcers (VLUs), caused by poor blood circulation, are another significant concern, often recurring and demanding targeted treatment strategies.

Beyond chronic wounds, there’s also a rising need for effective wound care in acute cases. The increasing number of surgical procedures, along with a global uptick in traumatic injuries and burn cases, is driving demand for dressings that not only speed up healing but also protect wounds from infection. Altogether, this growing complexity and volume of wounds across various patient populations highlight the urgent and expanding need for advanced wound care solutions.

The aging global population is playing a crucial role in driving the demand for advanced wound dressings and contributing to the expansion of the advanced wound dressing market size. As people grow older, their skin naturally becomes thinner and more delicate, making it more vulnerable to injuries, even from minor bumps or prolonged pressure. At the same time, older adults are more likely to live with chronic health conditions such as diabetes, poor circulation, and reduced mobility that slow down the body’s ability to heal. These factors combine to create a greater risk for developing complex wounds that are difficult to manage with traditional care methods.

Advanced wound dressings offer tailored solutions to support healing in this vulnerable group, helping to reduce pain, prevent complications, and improve overall quality of life. As the elderly population continues to grow worldwide, so too does the need for sophisticated, effective wound care products that can meet the challenges of aging skin and chronic conditions.

While advanced wound dressings offer significant benefits in terms of healing and infection control, their high cost remains a major barrier for many healthcare providers and patients. Products that incorporate cutting-edge technologies such as bioengineered skin substitutes, antimicrobial agents like silver, or smart sensors that monitor wound conditions are often priced far higher than traditional dressings. For hospitals and clinics, especially those operating with limited budgets, the cost of regularly using these premium products can be difficult to justify.

For patients, particularly those without strong insurance coverage, the out-of-pocket expenses can be overwhelming. In many developing countries and even in some developed ones reimbursement policies for advanced wound care products are limited or nonexistent. This lack of financial support often forces healthcare providers to choose less expensive, traditional wound care methods, even when more advanced solutions could offer better outcomes. As a result, access to the best possible care becomes uneven, with cost acting as a barrier to innovation and improved healing for many who need it most.

In many emerging economies, the adoption of advanced wound dressings is significantly hindered by a widespread lack of awareness and understanding. Both healthcare professionals and the general public are often unfamiliar with the benefits these modern dressings offer such as improved healing times, better infection control, and enhanced patient comfort. Traditional wound care methods, which are more affordable and have been relied upon for generations, continue to dominate treatment practices. This deep-rooted reliance on familiar, low-cost approaches makes it difficult for newer, more effective solutions to gain traction.

Adding to this challenge is a noticeable shortage of trained wound care professionals. Advanced dressings, especially those used for treating complex chronic wounds, require a certain level of skill and knowledge to apply correctly and monitor effectively. In many regions, however, there simply aren’t enough specialists or properly trained nurses to ensure optimal use. When these products are not applied or managed appropriately, their effectiveness can be compromised leading to disappointing outcomes and reduced confidence in their value.

This combination of limited knowledge and a lack of skilled professionals presents a major barrier to the broader adoption of advanced wound care, particularly in settings where modern solutions could make a significant difference.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product |

Moist Wound Dressings Antimicrobial Dressings Active Wound Care |

| By Application Type |

Chronic Wounds Acute Wounds |

| By End- User |

Hospitals Home Healthcare Specialty Clinics Ambulatory Surgical Centers (ASCs) |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Advanced Wound Dressing Market is categorized by product type, by patient and by end-user. Each segment is rapidly evolving, with different areas of the industry growing at their own pace and shifting in how much of the market they represent. The advanced wound dressing market is a complex and highly segmented sector. Understanding these segments is crucial for companies to develop targeted strategies, innovate products, and effectively reach different end-users while strengthening their market share across segments.

The advanced wound dressing market is primarily segmented based on the materials and technologies used, with each type playing a specific role in supporting the healing process. Moist wound dressings make up the largest and most widely used segment, holding a significant market share, as they are designed to maintain an optimal moist environment that promotes faster and more effective healing.

Among these, foam dressings are especially popular due to their high absorbency and versatility, making them ideal for wounds with moderate to heavy exudate. Hydrocolloid dressings, which form a gel-like substance when in contact with wound fluid, are well-suited for light to moderately draining wounds and help create a protective, healing environment. For dry wounds, hydrogel dressings provide much-needed hydration and support the body’s natural ability to remove dead tissue. Alginate dressings, made from seaweed, are another excellent option for highly exuding wounds due to their superior absorbency. Film dressings, known for their thin, transparent nature, are breathable and protective, often used as secondary coverings or on wounds with minimal drainage.

Collagen dressings play a more regenerative role by stimulating new tissue growth, especially helpful in chronic wound care. Antimicrobial dressings, infused with infection-fighting agents like silver or iodine, are critical in managing infected or high-risk wounds, and they held a strong market share in 2023 a trend expected to continue. Additionally, the active wound care segment, which includes advanced therapies like bioengineered skin substitutes and growth factors, is emerging as a powerful solution for severe or non-healing wounds, pushing the boundaries of traditional wound management and offering new hope for complex cases.

The advanced wound dressing market is also segmented based on the type of wound being treated, with each category presenting unique challenges and driving specific product demand. Chronic wounds make up the largest and most rapidly growing segment of the market. These are wounds that do not heal in a typical, timely fashion and often require long-term care. Among them, diabetic foot ulcers (DFUs) are a leading concern, driven by the rising global incidence of diabetes. As more people face complications related to diabetes, the need for specialized dressings that promote healing and prevent infection continues to grow.

Pressure ulcers, or bedsores, are another major sub-segment and hold a notable market share, especially prevalent among elderly or immobile patients who require constant care and preventative measures. Venous leg ulcers (VLUs), which result from poor blood circulation, also represent a significant portion of chronic wounds and are contributing to overall market growth as awareness and diagnosis improve.

On the other hand, acute wounds those that heal in a more predictable, straightforward manner still make up a vital part of the market. These include surgical wounds and traumatic injuries, both of which are on the rise due to increasing surgical procedures and higher rates of accidents worldwide. Advanced wound dressings are increasingly being used in these cases to accelerate recovery and reduce the risk of complications. Burn care is another key area within acute wounds, with growing demand for advanced dressings that not only promote healing but also minimize pain and scarring. Together, these wound types shape a diverse and expanding market, highlighting the need for tailored solutions that address specific healing needs and patient outcomes.

The advanced wound dressing market is also shaped by the type of healthcare setting in which these products are used, reflecting different levels of care and patient needs that collectively drive the advanced wound dressing market size. Hospitals remain the largest end-user segment, as they handle a high volume of both acute and chronic wounds from surgical incisions to complex, non-healing ulcers. With access to specialized staff and resources, hospitals are primary consumers of advanced wound care products that support faster healing and reduce complications. However, home healthcare is quickly emerging as the fastest-growing segment.

As more patients with chronic wounds opt for or are prescribed at-home treatment, there’s a growing demand for dressings that are easy to apply, comfortable, and effective outside of a clinical setting. This shift is largely driven by cost savings, convenience, and a growing preference for recovery in the comfort of one’s home. Specialty clinics, such as wound care centers, are also gaining traction, offering targeted treatment for complex or slow-healing wounds that require ongoing monitoring and specialized care. Additionally, ambulatory surgical centers (ASCs) are contributing to market growth, as the number of outpatient surgeries continues to rise.

These centers rely on advanced dressings to support efficient post-operative healing while minimizing the need for extended hospital stays. Together, these settings illustrate how the demand for advanced wound care is expanding across the healthcare landscape, from traditional hospitals to more flexible, patient-centered environments.

North America especially the United States leads the global advanced wound dressing market, accounting for over 40% of the total market share in 2024. This dominance is driven by a combination of demographic, medical, and economic factors. The region faces a high burden of chronic wounds, largely due to an aging population and the widespread prevalence of conditions like diabetes and obesity. As a result, there’s a significant need for advanced wound care solutions to manage complications such as diabetic foot ulcers and pressure sores. North America also benefits from a robust healthcare infrastructure that supports the rapid adoption of new technologies and innovative treatment methods. In the U.S., favorable reimbursement policies make these advanced products more accessible to patients, reducing out-of-pocket costs and encouraging wider use.

Additionally, the region’s high healthcare expenditure allows for substantial investment in top-tier wound care solutions, further fueling market growth. Together, these factors create an environment where advanced wound dressings are not only in high demand but also widely available and integrated into standard care practices.

Europe represents a mature but steadily growing market for advanced wound dressings, holding the second-largest market share globally after North America. Much like its transatlantic counterpart, Europe is seeing a steady rise in chronic wounds driven by an aging population, with more elderly individuals experiencing conditions that require ongoing wound care, such as pressure ulcers and diabetic foot ulcers.

The region’s strong and well-established healthcare systems both public and private prioritize clinical effectiveness and evidence-based treatments, creating a supportive environment for the adoption of advanced wound care products. As chronic diseases continue to rise across the continent, the demand for effective wound management solutions grows alongside them. Additionally, Europe’s stringent regulatory environment and strong emphasis on product safety and quality ensure that only high-standard, proven products reach the market, further reinforcing consumer and clinician trust in advanced dressings. Together, these factors contribute to the region’s steady and reliable market performance.

The Asia-Pacific region stands out as the fastest-growing market for advanced wound dressings, with a strong projected CAGR over the coming years. This rapid growth is fueled by a combination of demographic and economic factors. With a vast and expanding population particularly in countries like China and India the region presents a massive and increasingly health-conscious consumer base.

One of the most pressing health challenges is the sharp rise in diabetes, which is contributing to a growing number of chronic wounds, especially diabetic foot ulcers, creating a significant need for effective wound care solutions. At the same time, healthcare infrastructure across the region is improving rapidly.

Increased government spending, private investments, and rising disposable incomes are making advanced medical products more accessible than ever before. Awareness of modern wound care practices is also growing, helping to drive demand. Additionally, the region’s thriving medical tourism sector particularly in countries like India and Thailand is boosting the use of high-quality wound dressings for post-surgical recovery, further accelerating market growth. Altogether, Asia-Pacific is transforming from an emerging market into a major force in the global wound care landscape.

The Middle East & Africa region represents a developing but promising market for advanced wound dressings. Growing awareness around health, hygiene, and modern medical care both among the public and through government initiatives is beginning to drive demand for more effective wound treatment options. In particular, countries in the Gulf region, along with select areas in Africa, are seeing increased investment in healthcare infrastructure, including new hospitals, clinics, and training programs, all of which are helping to create a foundation for the adoption of advanced wound care products.

However, the region also faces notable hurdles. Limited reimbursement systems make these products less affordable for many patients, and in rural or underserved areas, access to quality healthcare remains a challenge. Additionally, traditional wound care practices are still common, which can slow the shift toward more modern solutions. Despite these barriers, ongoing improvements in healthcare delivery and infrastructure suggest that this market is on a gradual but steady upward path, with growing potential over the long term.

The advanced wound dressing market was valued at USD 12.3 billion in 2024.

The advanced wound dressing market is projected to grow at a CAGR of 6.71% from 2025 to 2033.

Chronic wounds Segment holds the largest market share.

Asia-Pacific region is expected to witness the highest growth rate.

Major players include 3M, Coloplast Corp., Medline Industries, Smith & Nephew, ConvaTec Group PLC, Derma Sciences (Integra LifeSciences), Ethicon (Johnson & Johnson), Baxter International, Mölnlycke Health Care AB, and Medtronic.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Advance Wound Dressing Market, By Product

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Advance Wound Dressing Market, By Application type

5.3 Advance Wound Dressing Market, By End-User

6.1 North America Printed Electronics Market , By Country

6.1.1 Printed Electronics Market, By Product Type

6.1.2 Printed Electronics Market, By Application Type

6.1.3 Printed Electronics Market, By End-User

6.2 U.S.

6.2.1 Printed Electronics Market, By product

6.2.2 Printed Electronics Market, By Application Type

6.2.3 Printed Electronics Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America