Aerospace Plastics Market

Aerospace Plastics Market Size, Market Share & Trends Analysis Report By Polymer Type (PMMA, PC, ABS, PEEK, PPS, Others), By Aircraft Type (Commercial Aircraft, General & Business Aircraft, Military Aircraft, Rotary Aircraft, Others, UAV, Spacecraft), By Application (Cabin Windows & Windshields, Cabin Lighting, Overhead Storage Bins, Aircraft Panels, Aircraft Canopy, Others, Cabin Seat Components, Lavatory Fixtures), By Region (North America, Europe, Asia-Pacific, Middle East and Africa, Latin America) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code : ASIADR1001

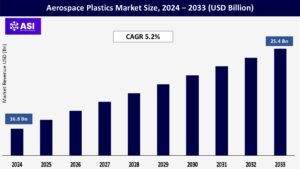

CAGR: 5.2%

Last Updated : May 14, 2026

The global Aerospace Plastics Market size was valued at approximately USD 16.8 billion in 2024 and is projected to reach USD 25.4 billion by 2033, growing at a steady CAGR of 5.2% during the forecast period (2026–2033).

The market is witnessing strong demand driven by the increasing use of lightweight materials in aircraft manufacturing, rising demand for fuel-efficient aircraft, and advancements in plastic technologies.

Key growth drivers include the growing focus on reducing aircraft weight to improve fuel efficiency, stringent environmental regulations, and the development of high-performance plastics with enhanced durability and thermal resistance.

The integration of advanced polymers such as PEEK, PPS, and PMMA in aircraft interiors, exteriors, and structural components is also shaping the future of the aerospace plastics industry.

The aerospace plastics market is experiencing growth due to the rising demand for lightweight materials in aircraft manufacturing. Plastics and composites are increasingly replacing traditional materials such as aluminum and steel to reduce aircraft weight, improve fuel efficiency, and lower operational costs.

Lightweight materials are particularly critical in the production of commercial and military aircraft, where every kilogram saved translates to significant fuel savings over the aircraft’s lifespan.

The growing emphasis on sustainability and reducing carbon emissions is further driving the adoption of aerospace plastics. Manufacturers are focusing on developing high-performance plastics that offer superior strength-to-weight ratios, thermal stability, and resistance to corrosion and fatigue.

Innovations in plastic technologies, such as the development of advanced polymers like PEEK, PPS, and PMMA, are significantly enhancing the performance and application scope of aerospace plastics. These materials are gaining traction due to their high strength, chemical resistance, and ability to withstand extreme temperatures.

The integration of nanotechnology and fiber-reinforced plastics is revolutionizing the aerospace plastics market. These materials offer enhanced mechanical properties, such as increased tensile strength and impact resistance, making them ideal for use in critical aircraft components.

Additionally, the development of flame-retardant and self-healing plastics is expanding their application in aircraft interiors and electrical systems.

Despite the advantages of aerospace plastics, high development and manufacturing costs pose a challenge to market expansion. The production of high-performance plastics requires advanced technologies and specialized equipment, which significantly increases the overall cost of materials. This limits their adoption in budget-constrained regions and among smaller aircraft manufacturers.

The aerospace industry is subject to stringent regulatory standards and certification requirements, which can delay the adoption of new materials. Plastics used in aircraft must meet rigorous safety and performance standards, which can increase the time and cost associated with material development and testing.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Polymer Type |

PMMA PC ABS PEEK PPS Others (Nylon 6, POM-C and PES) |

| By Aircraft Type |

Commercial Aircraft General & Business Aircraft Military Aircraft Rotary Aircraft Others UAV Spacecraft |

| By Application |

Cabin Windows & Windshields Cabin Lighting Overhead Storage Bins Aircraft Panels Aircraft Canopy Others Cabin Seat Components Lavatory Fixtures |

| Key Players |

Solvay S.A. SABIC BASF SE Victrex plc Evonik Industries AG Toray Industries, Inc. Hexcel Corporation Ensinger GmbH Covestro AG PPG Industries, Inc. |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Aerospace Plastics market is segmented by polymer type, aircraft type, and application, each contributing uniquely to the market’s growth.

The high-performance materials such as PEEK, PPS, and PMMA dominate due to their exceptional strength, thermal stability, and chemical resistance. PEEK is widely used in structural components and electrical systems, while PMMA is preferred for cabin windows and windshields due to its transparency and impact resistance.

ABS and Nylon 6 are popular in cabin interiors, such as overhead storage bins and seat components, owing to their durability and ease of molding. POM-C and PES are gaining traction for precision components and high-temperature applications, respectively.

Commercial Aircraft: Dominated the market in 2024, accounting for over 39.3% of the market share. The growing demand for fuel-efficient and lightweight aircraft is driving the adoption of aerospace plastics in this segment. General and business aircraft are also witnessing steady growth, with increasing use of plastics in luxury interiors.

Military aircraft utilize advanced plastics for stealth technology, radar systems, and structural components, while rotary aircraft and UAVs are adopting plastics for weight reduction and enhanced performance. Spacecraft applications are emerging, with high-performance plastics being used for thermal protection and structural integrity.

Cabin windows and windshields represent a significant segment, with PMMA and PC being the preferred materials due to their transparency and strength. Cabin lighting relies on PES and PC for their thermal stability, while overhead storage bins and lavatory fixtures commonly use ABS for its durability.

Aircraft panels and structural components increasingly incorporate PPS and PEEK for their flame retardancy and chemical resistance. Cabin seat components and other interior applications utilize Nylon 6 and POM-C for their toughness and wear resistance. Each segment highlights the critical role of aerospace plastics in enhancing aircraft performance, safety, and efficiency.

North America accounted for 40.2% of the global aerospace plastics market share in 2024, supported by the strong presence of aircraft manufacturers such as Boeing, Lockheed Martin, and General Dynamics. The U.S. leads the region, with high demand for commercial and military aircraft.

Europe holds a xx% market share, with growing demand for aerospace plastics in countries like the UK, France, and Germany. The region is also focusing on sustainable aviation initiatives, driving the adoption of lightweight materials.

Asia-Pacific is projected to witness the highest CAGR of 6.5% during the forecast period, fueled by rising demand for commercial aircraft in China, India, and Japan. The region is also witnessing increasing investments in aerospace manufacturing capabilities.

The Middle East and Africa are emerging markets, driven by the growing aviation industry in Gulf countries such as the UAE and Saudi Arabia. High defense spending and increasing air travel are key contributors to market expansion.

Latin America is seeing steady growth, with Brazil and Mexico leading the market. The region is focusing on upgrading its aviation infrastructure and expanding its fleet of commercial and military aircraft.

The global aerospace plastics market was valued at approximately USD 16.8 billion in 2024.

The market is projected to grow at a CAGR of 5.2% from 2026 to 2033.

The Key drivers include the increasing demand for lightweight materials, advancements in plastic technologies, and stringent environmental regulations.

PEEK and PMMA hold significant market shares due to their high performance and versatility.

Cabin windows and windshields lead the market, followed by cabin lighting and overhead storage bins.

North America holds the largest market share at 40.2%.

The Asia-Pacific region is expected to grow at a CAGR of 6.5% from 2026 to 2033.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Aerospace Plastics Market, By Polymer Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Aerospace Plastics Market, By Aircraft Type

5.3 Aerospace Plastics Market, By Application

6.1 North America Aerospace Plastics Market, By Country

6.1.1 Aerospace Plastics Market, By Polymer Type

6.1.2 Aerospace Plastics Market, By Aircraft Type

6.1.3 Aerospace Plastics Market, By Application

6.2 U.S.

6.2.1 Aerospace Plastics Market, By Polymer Type

6.1.2 Aerospace Plastics Market, By Aircraft Type

6.2.3 Aerospace Plastics Market, By Application

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping