Agricultural Adjuvants Market

By Application Type (Insecticide, Fungicide, Herbicide), By Crop Type (Cereals and Grains, Fruits and Vegetables), By Function Type (Activator Modifiers, Utility Modifiers), By Region (North America, APCA, South America, Europe, Middle East and Africa) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2024–2032.

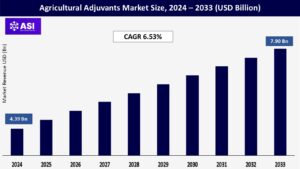

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 6.53%

Last Updated : March 20, 2026

The global Agricultural Adjuvants Market was valued at approximately USD 4.39 Billion in 2024 and projected to reach USD 7.90 Billion by 2032, growing at a C`AGR of 6.53% during the forecast period (2024–2032).

Farming operations, including soil testing, crop scouting, yield monitoring, and field georeferencing, are being performed with the assistance of agricultural technologies. Growing higher yields was made possible for farmers by introducing agricultural adjuvants. In the farm sector, adjuvants are primarily used to increase the effectiveness of insecticides, fungicides, fertilizers, plant growth regulators (PGRs), and herbicides. They also improve the solution’s efficacy and aid in better distribution and drift reduction.

The increase in the use of natural and sustainable adjuvants is emerging as a major driver in the growth of the agricultural adjuvant market. Adjuvants are substances added to pesticides or herbicides to enhance their performance, and the growing focus on environmental safety has spurred interest in natural and eco-friendly alternatives. Traditionally, many adjuvants have been petroleum-based, raising concerns over soil contamination, water pollution, and harm to non-target organisms. However, natural adjuvants derived from sources such as soy lecithin, coconut oil, castor oil, and other plant-based or biodegradable materials offer a safer and more sustainable solution.

One of the key factors driving this trend is the increasing consumer demand for organically produced food and sustainable farming practices. As awareness of climate change, environmental degradation, and food safety grows, there is mounting pressure on the agriculture industry to reduce its reliance on synthetic chemicals. Natural adjuvants are favoured for their low environmental footprint, non-toxic nature, and compatibility with Integrated Pest Management (IPM) and organic certification programs. These factors make them especially attractive in both developed and developing agricultural economies. Furthermore, many governments and regulatory bodies are implementing stricter rules on the use of synthetic agrochemicals, which is accelerating the transition towards green chemistry in agriculture. Natural adjuvants also help improve the efficiency of active ingredients in pesticides and fertilisers, which can reduce overall chemical use and input costs, benefiting farmers economically.

Advances in formulation technologies and increased R&D investments are also expanding the range of applications for sustainable adjuvants across various crop types. As sustainability becomes a central focus in modern agriculture, the demand for natural adjuvants is expected to grow steadily, driving innovation and reshaping the competitive landscape of the global agricultural adjuvant market.

During the 1950s and 1960s, resolving pesticide wastage issues was a significant undertaking. Most insecticides were not intended to be used with water in combination. However, most insecticides today are made to be mixed with water. Many fungi, plants, and pests have waxy surfaces, which makes it challenging for water-based sprays to achieve their objectives efficiently. Adjuvants are proving to be a blessing in overcoming this obstacle. Any substance that is added to a spray tank to improve the effectiveness of a pesticide is referred to as an adjuvant. Surfactants, spreaders, stickers, crop oils, anti-foaming materials, and buffering agents are examples of adjuvants.

Surfactants are adjuvants that support and enhance a fluid’s ability to emulsify, scatter, spread, wet, or exhibit other surface-altering properties. It has been discovered that applying fungicides, insecticides, or herbicides without the recommended adjuvant results in a 30% to 50% reduction in pesticide action and a significant amount of pesticide waste. Thickeners that act as a drift control agent in tank-mix application sprays, stickers, and spreaders are the most popular and widely used adjuvants for reducing pesticide wastage.

In addition to their contribution to pollution and ecological harm, petroleum-oil-based adjuvants are increasingly viewed as unsustainable due to their origin from finite fossil fuel resources. These adjuvants, commonly used to enhance the efficacy of pesticides and herbicides, often leave behind residues that do not break down easily in the environment. Over time, this leads to the accumulation of toxic substances in soil and water bodies, which can affect biodiversity and disrupt ecosystems. For instance, runoff from agricultural fields containing petroleum-based adjuvants can pollute nearby water sources, harming aquatic organisms and contaminating drinking water supplies. Moreover, the volatility and flammability of petroleum derivatives pose safety hazards during handling, storage, and application, adding to the operational risks for farmers and applicators.

With increasing public pressure and environmental advocacy, governments and regulatory bodies across the globe are implementing stricter regulations on the use of synthetic and oil-based agricultural inputs. This has led to higher compliance costs for manufacturers and has created market entry barriers for products based on petroleum chemistry. Furthermore, the growing consumer demand for organic and sustainably produced food has encouraged farmers to seek alternatives to petroleum-based adjuvants, such as those derived from plant oils, natural surfactants, and other biodegradable materials. These factors collectively restrain the growth potential of petroleum-oil-based adjuvants and are driving innovation and investment in the development of natural, bio-based adjuvant solutions.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Application Type |

Insecticide Fungicide Herbicide |

| By Crop Type |

Cereals and Grains Fruits and Vegetables |

| By Function Type |

Activator Modifiers Utility Modifiers |

| Key Players |

Clariant AG Solvay SA The Dow Chemical Company Huntsman International LLC Evonik Industries AG Ingevity Nufarm Limited Corteva Agriscience Croda International PLC BASF SE Miller Chemical & Fertilizer, LLC. Agricultural Adjuvants Market Report Segmentation |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Insecticide-based adjuvants are specifically formulated to improve the spreading, sticking, and penetration of insecticide formulations on crop surfaces, leading to better pest control outcomes and reduced chemical wastage. The rising global demand for high agricultural productivity, coupled with the need to protect crops from a wide range of insect pests, has led to increased adoption of these adjuvants. Moreover, the growing awareness among farmers about the benefits of using adjuvants with insecticides, such as improved spray coverage, rain fastness, and increased efficacy, further drives market growth.

Technological advancements in formulation science and the shift toward integrated pest management (IPM) practices are also contributing to the expansion of this segment. Fungicides play a significant role in enhancing the efficacy and performance of fungicidal products. Adjuvants such as surfactants, spreaders, and stickers are commonly added to fungicides to improve their adhesion, spreading ability, and penetration into plant tissues. This results in better coverage and increased absorption of the active ingredient, leading to more effective control of fungal pathogens. The growing prevalence of fungal diseases in crops such as cereals, fruits, and vegetables has increased the demand for efficient fungicidal treatments, subsequently driving the use of adjuvants. Moreover, the shift toward precision farming and sustainable agriculture practices has further fuelled the adoption of adjuvants to maximize fungicide efficiency while minimizing environmental impact.

The herbicide segment is the highest contributor to the market and is expected to grow at a CAGR of 6.95% during the forecast period. Chemicals known as herbicides are employed to manage undesirable vegetation. The most frequent use of herbicides is in farming fruits, vegetables, oilseeds, and row crops, and is applied before or during planting to increase crop productivity by reducing other vegetation. In addition to glyphosate, 2,4-D, atrazine, dicamba, cyanazine, and trifluralin, the farmers also use different herbicides. Using a selective herbicide prevents the growth of a particular weed while leaving the other plants unharmed. The rising herbicide consumption will drive the agricultural adjuvants market during the forecasted period.

The cereals and grains segment owns the highest market share and is expected to grow at a CAGR of 6.58% during the forecast period. The rising population and rising per capita consumption of cereals and grains are the main factors driving the growth of the market for agricultural adjuvants. Farmers are looking for a way to increase yield as the demand for different grains and cereals rises. Due to their properties, agricultural adjuvants with crop protection chemicals improve the production of cereals and grains. Agrochemical adjuvants are applied to various cereal crops, such as wheat, maize, rice, barley, oats, rye, and sorghum, to increase yield. The agricultural adjuvants market is anticipated to generate most of its revenue from the segment of cereals and grains.

The Fruits & Vegetables category is a high-value and rapidly expanding segment within the agricultural adjuvants market. This sector demands intensive crop protection due to its vulnerability to pests and diseases, combined with consumer demand for pristine, high-quality produce. Adjuvants, including spreaders, stickers, surfactants, and drift-control agents, play a critical role by improving adhesion, coverage, rain fastness, and systemic absorption of herbicides, fungicides, and insecticides on leaves and fruits.

High value produces such as apples, grapes, tomatoes, and lettuce relies heavily on these products to ensure uniform application and minimize chemical usage. Market forecasts from sources like Markets Project that, of all crop types, fruits & vegetables will experience the fastest growth between 2022 and 2027, fuelled by rising consumer demand for fresh and nutritious produce. Globally, this segment represents over a third of the adjuvant market share, about 34% in 2024, driven by intensifying adoption of eco-friendly and organic farming practices, which Favor biobased and environmentally benign adjuvants.

The activator modifiers segment is the highest contributor to the market and is expected to grow at a CAGR of 7.19% during the forecast period. These are the most typical kinds of adjuvants used in agriculture. Surface tension, density, volatility, and solubility are just a few of the physical and chemical characteristics of the spray solution that are improved by activator modifier adjuvants. Additionally, adjuvants with activator modifiers enhance the biological effectiveness of crop protection chemicals. These modifiers increase the action of fungicides, insecticides, and herbicides by altering features such as particle size, spray dispersion on the plant, spray viscosity, chemical uptake rate, and crop protection chemicals’ solubility in the spray solution.

Adjuvants used to improve the spray formulation applied to all plants are called utility modifiers. These modifiers alter adjuvants’ physical and chemical characteristics in a way that makes it simpler to reduce the adverse effects, resulting in an effective formulation for fungicides, insecticides, and herbicides. Adjuvants and utility modifiers aid in more effective product application across leaves. Examples include emulsifiers, stabilizing substances, dispersants, coupling, compatibility, and buffering substances.

It is the most significant shareholder in the global agricultural adjuvants market and is expected to grow at a CAGR of 6.71% during the forecast period. In terms of revenue, North America is the region that contributes most to the market for agricultural adjuvants. In the upcoming years, there will be a rise in the use of agricultural adjuvants for crop protection due to the rising demand for organic products. The strict regulatory framework prohibiting the use of pesticides has helped the regional market growth. The high usage of agrochemicals in the area, typically used through adjuvants, is the reason behind the expansion of the North American agricultural adjuvants market.

Japan is expected to grow at a CAGR of 7.63%, generating USD 1,435.43 million during the forecast period. A growing population and agricultural yield will increase demand for agricultural adjuvants in the Asia-Pacific and Japan. Japan leads this area in agricultural adjuvant consumption. Globalization of the crop protection chemical industry has impacted the Asia-Pacific and Japan markets. The market for herbicides, fungicides, insecticides, fertilizers, and plant growth regulators (PGRs) is expected to grow faster in the Americas and Europe than in the Asia-Pacific and Japan due to population growth, increased cereal and grain production, and economic development.

It is one of the agrochemical markets with the fastest growth in Brazil and Argentina. Argentina, followed by Brazil, holds a significant share of the region’s growing agricultural market. The market for agricultural adjuvants in South America is anticipated to be driven by rising global food demand and growing knowledge of how agricultural adjuvants can increase agricultural fields’ yields. Adjuvants are also proving to be an effective solution to the problem of water scarcity in some areas of the region because they spread over more expansive areas while using fewer pesticides and other crop protection chemicals.

It is expected to experience significant growth over the forecast period. Although crop production has been declining in some European countries in recent years, several nations have shown growth in specific crop sectors. For instance, a USDA report from November 2021 noted that Russia’s total wheat production reached 74.5 million metric tons, reflecting an increase in the country’s wheat output. The market’s growth is largely driven by the need to enhance crop yields and production efficiency due to a rising population and decreasing farmland. Consequently, the region’s increasing agricultural production and diminishing arable land are driving demand for crop protection chemicals, which in turn fuels the demand for related products.

The agricultural adjuvants market in the Middle East and Africa is anticipated to experience substantial growth over the forecast period. This expansion is driven by rising pesticide consumption in countries such as Saudi Arabia and Oman, and is expected to continue in South Africa, Kuwait, and Qatar. The growing need for food crops, along with increased use of pesticides and insecticides, is contributing to the heightened demand for agricultural adjuvants in the region. These adjuvants play a crucial role in optimizing the effectiveness of crop protection products and supporting agricultural productivity.

The current market size is approximately USD 4.39 billion 2024 and projected to reach USD 7.90 billion by 2032.

The market is projected to grow at a CAGR OF 6.53 % of Agricultural Adjuvants Market.

North America holds the largest market share of Agricultural Adjuvants Market.

The herbicide segment is the highest contributor to the market and is expected to grow at a CAGR of 6.95% during the forecast period.

Clariant AG, Solvay SA, The Dow Chemical Company, Huntsman International LLC

Evonik Industries AG, Ingevity, Nufarm Limited Corteva Agriscience are the top players in the Agricultural Adjuvants Market.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Agricultural Adjuvants Market, By Application Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Agricultural Adjuvants Market, By Function Type

5.3 Agricultural Adjuvants Market , By Crop Type

6.1 North America Agricultural Adjuvants Market, By Country

6.1.1 Agricultural Adjuvants Market, By Application Type

6.1.2 Agricultural Adjuvants Market, By Function Type

6.1.3 Agricultural Adjuvants Market, By Crop Type

6.2 U.S.

6.2.1 Agricultural Adjuvants Market, By Application Type

6.2.2 Agricultural Adjuvants Market, By Function Type

6.2.3 Agricultural Adjuvants Market, By Crop Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping