Airway Management Devices Market

Airway Management Devices Market Share and Trend Analysis, By Product Type (Infraglottic Devices, Supraglottic Devices, Laryngoscopes, Resuscitators and Emergency Airway Kits, Pediatric & Neonatal Airway Solutions), By Application (Anesthesia, Emergency Medicine, Critical Care , Neonatal and Pediatric Care, Home Healthcare), By End User (Hospitals, Ambulatory Surgical Centers, Emergency Medical Services, Home Healthcare Providers, Military & Disaster Response Units) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

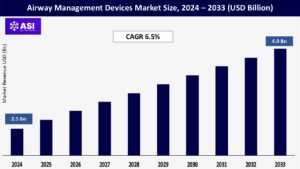

CAGR: 6.5%

Last Updated : August 1, 2025

The global Airway Management Devices Market was valued at USD 2.5 billion in 2024 and is projected to reach USD 4.0 billion by 2033, expanding at a compound annual growth rate CAGR of 6.5% during the forecast period (2025 – 2033).

Airway management devices are essential medical devices designed to restore or preserve patient ventilation during surgery, emergencies, and intensive care. Such products prevent there being insufficient ventilation by creating and sustaining an open airway for air to enter the lungs without the complications associated with compromised airways. There are many products found in the marketplace ranging from infraglottic devices such as endotracheal tubes and tracheostomy tubes, supraglottic devices such as laryngeal mask airways, laryngoscopes for visualization during intubation, and resuscitators for urgent ventilation. The increase in incidence of respiratory conditions, more surgeries under anesthesia, and better emergency care admissions have been major drivers for market growth. Furthermore, technological innovations aimed at patient safety with low complication rates and enhanced clinical outcomes continue to propel innovation in this market with a specific focus on non-invasive treatments and disposable equipment to reduce the risk of infection.

Development of higher disease burden of chronic respiratory diseases worldwide necessitated the expansion of airway management devices market. Growing incidences of chronic obstructive pulmonary disease (COPD), asthma, and sleep apnea have witnessed high rates of growth globally, necessitating sophisticated airway management devices for both short-term and long-term treatment. Based on the recent health statistics, COPD takes the third position in terms of the most common cause of death worldwide, impacting millions of patients who often need immediate treatment and respiratory care. The World Health Organization has alerted towards the strong burden that these conditions place on the healthcare system given the fact that respiratory conditions contribute to a high percentage of hospitalization and emergency admissions.

This is compounded by an increasingly large population of elderly patients, who are more vulnerable to respiratory complications and are more likely to need repeated airway interventions throughout the course of medical therapy. Physiology that varies with age, such as decreased lung compliance and decreased respiratory muscle strength, all contribute to increased airway complication rates with surgical procedures and critical care situations. Healthcare professionals are therefore investing in cutting-edge airway management technologies to tackle these challenges in the most optimal way possible, propelling incredible market growth in developing and emerging economies as well.

The airway management devices market has been led by ongoing technological advancements that have focused on device performance enhancement, safety profiles, and user-friendliness. These past few days have seen rigorous development of video laryngoscopy, a imaging modality with superior visualization of the airway during intubation, significantly lowering the risk of failed intubation and its consequences. These gadgets have high-definition screens and cameras, enabling physicians to intubate difficult airways more accurately and with increased confidence. Parallel to this, the creation of sensor-equipped smart tracheal tubes to track airflow, pressure, and oxygen saturation rates has transformed patient monitoring capacity in critical care areas.

Coupling with artificial intelligence and real-time feedback loops also improved the performance of these devices to deliver effective intervention during complications. Parallel to this, the growth in surgical procedures performed under general anesthesia at the global level has generated regular demand for safe airway management equipment. Expansion of ambulatory surgery centers and increased need for minimally invasive procedures have expanded the usage base of devices beyond conventional hospital environments. Moreover, the pandemic-facilitated rebound in elective procedures has driven market expansion as healthcare facilities aim towards clearing the backlog of suspended procedures while continuing stringent safety measures most likely to encompass dedicated airway management practices.

Even with immense opportunities for expansion, the airway management devices market is afflicted by some severe issues of cost limitations and shortage of trained professionals. The newer airway management devices, especially the video laryngoscopes and the high-end intubating devices, are extremely costly and can be outside the reach of financially strained healthcare facilities. Such a budget constraint is very essential in developing countries where the construction of the health infrastructure is a continuous process and resource allocation towards necessary medical needs becomes a priority over specialist apparatus. Compounded to the intricacies is a lack of medical personnel with special skills for managing advanced airway management. Utilization of advanced airway equipment needs specialized skills and competence that are not present in every healthcare facility.

The curve of learning the new technologies is steep and will cause resistance from practitioners who are used to traditional methods. Simulation education and training programs, though a good thing in the long run, are ancillary costs that hospitals must weigh. In addition, the perpetual global shortage of health care professionals has worsened the issue at hand, as numerous facilities have been unable to provide satisfactory critical care and emergency room staffing levels at which airway management skills are required the most. The multi-dimensional nature of these hindrances poses insurmountable barriers to entry into such markets and health care facilities, which can discourage the adoption rate of new airway management solutions for their worth in clinical applications.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Infraglottic Devices Supraglottic Devices Laryngoscopes Resuscitators and Emergency Airway Kits Pediatric & Neonatal Airway Solutions

|

| By Application |

Anesthesia Emergency Medicine Critical Care Neonatal and Pediatric Care Home Healthcare

|

| By End User |

Hospitals Ambulatory Surgical Centers Emergency Medical Services Home Healthcare Providers Military & Disaster Response Units

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Airway management devices market segmentation by product type reveals clear classes that address particular clinical requirements in different healthcare environments. Infraglottic devices such as endotracheal tubes and tracheostomy tubes constitute the biggest market segment because of their pivotal role to establish definitive airways in complicated surgeries and emergencies. They offer uninterrupted access to the trachea with normal ventilation and aspiration protection in risky cases. Endotracheal tubes, in forms such as oral, nasal, and double-lumen tubes, continue to be the gold standard for airway management under general anesthesia and critical care. The most rapidly growing segment are the supraglottic airway devices due to the fact that they are less invasive in nature and better designed by experts to provide patient comfort with optimal ventilation.

Laryngeal mask airways (LMAs) and the like have become common usage in ambulatory operating rooms as well as rescue devices in situations of difficult intubation. Laryngoscopes, both traditional and video laryngoscopes, are another extremely critical sector that has seen phenomenal technological growth. Video laryngoscopes, for example, have changed entirely the management of difficult airways by enabling much superior glottic opening visualization, first-attempt success significantly enhanced during intubation. Resuscitators and emergency airway devices round out the product line to cover immediate ventilation requirements for pre-hospital and emergency room situations. Growing demand is also being reported for specialized pediatric and neonatal airway management products, driven by the distinctive anatomical realities and safety considerations of these at-risk patient populations.

Application-oriented segmentation of the market for airway management devices considers the variety of clinical environments where the devices are required. Anesthesia dominates the market because airway management is an integral component of anesthetic practice in all fields of surgery. The controlled setting of the operating room requires trustworthy airway devices to be applied for changing periods of time with optimum ventilation parameters and very little room for complications. Anesthesiologists utilize a complete range of airway management devices, from basic face masks to advanced combination devices, choosing the best one according to patient type and procedure need. Emergency medicine is another important application area with unique needs of rapid intervention in unforeseen and frequently complex scenarios.

Emergency airway management is also often performed in sub-optimal surroundings with limited knowledge of the patient, so equipment that provides flexibility, convenience, and stress tolerance is important. The pre-hospital emergency environment also widens this spectrum of uses, where paramedics and first responders need compact, rugged airway management devices to be used in field environments. Critical care uses are a rapidly expanding market, fueled by the increasingly critically ill patients entering intensive care units who are frequently on the airway and in need of longer durations of ventilation assistance. The distinct requirements of this group have necessitated some innovations in tracheostomy tubes, speaking valves, and other devices intended to be used over the long term. In addition, novel applications in pediatric and neonatal medicine, home ventilation of chronically ventilated patients, and procedural sedation outside operating rooms broadened the applications, leading to device manufacturers creating specialized devices for these new clinical situations.

The end-user market for airway management devices is an image of the varied healthcare environments in which airway intervention procedures are performed, each with different needs and implications. Hospitals form the largest end-user market with the largest market share because they offer complete ranges of services under emergency care, surgery, and intensive care management. Within hospital settings, operating rooms, emergency departments, and intensive care units are the main locations of use of high-tech airway management technology. Training facilities and university medical centers will be most likely to be early adopters of new devices as locations for testing new technology with subsequent entry into broader markets. Ambulatory surgery centers represent a fast-expanding end-user market based on the worldwide trend towards outpatient care and efficient models of health care delivery.

They are likely to concentrate in specialized forms of airway management devices appropriate for short-procedure duration and high-speed patient throughput, with particular focus on supraglottic airways and video laryngoscopy devices facilitating efficient workflows. Emergency medical services are also a highly important end-user segment whose particular demands revolve around portability, durability, and user-friendliness under unforgiving field conditions. Pre-hospital airway management frequently takes place in less-than-ideal settings with the requirement for strong equipment capable of functioning effectively under varied conditions. Home care is a niche but growing market as increasing numbers of patients with chronic respiratory disease are being cared for outside the standard healthcare setting. This has driven production of simple-to-use equipment that is appropriate for non-professional use, such as tracheostomy care products and home rescue airway kits. Military and disaster relief groups complete the end-use environment, necessitating specialty airway management products that function in austere conditions.

North America is the leading regional market for airway management products due to advanced healthcare infrastructure, supportive reimbursement practices, and high levels of healthcare spending. The United States is the leading regional consumer due to high surgical volumes and growing incidence of chronic respiratory disease. Early uptake of advanced technologies, including video laryngoscopy and advanced intubation equipment, by the region has set a benchmark for future airway management practices. Strict patient safety protocols and infection control measures have also fueled the adoption of single-use devices in all healthcare units in the region.

Europe is the second-largest market for airway management devices in the world, and there are well-developed healthcare systems in the region with increased focus on minimally invasive care. It is characterized by special excellence in employing supraglottic airway devices, and nations such as the United Kingdom and Germany are at the forefront of embracing premium airway management technologies. Markets in the European continent have increasingly turned towards devices that provide enhanced patient comfort and fewer complications, fueling materials and design innovation. The high percentage of aging population and thereby the high percentage of surgical intervention remains a driving force in maintaining market growth irrespective of economic downturns in many countries.

Asia Pacific holds the best growth opportunities in the airway management devices market due to rapidly evolving healthcare infrastructure, growing healthcare spending, and heightened awareness of advanced medical technologies. The key growth opportunities among them are China, India, and Japan, with growing surgical volumes and rising rates of respiratory diseases. The region is also becoming a production center for some airway management items, notably Malaysia and Thailand, with cost benefits that can expedite market penetration. Additionally, emergent development of emergency medical services in the major cities is driving new demand for pre-hospital airway management solutions.

Airway management devices demand is increasing unbalanced but has strong prospects in urban and market regions. Mexico and Brazil spearhead Latin America, driving the adoption of state-of-the-art intubation and ventilation products as healthcare facilities upgrade. High healthcare investments across the Gulf states drive adoption of video laryngoscopes and single-use airway kits, while Dubai and Abu Dhabi medical tourism lifts demand. In contrast, much of Africa is under-equipped with specialized equipment and relies on simple resuscitators and hand-operated devices. Opportunity for providers and manufacturers lies in providing cost‑effective, long-lasting solutions that meet infrastructure and economic realities.

The global airway management devices market was valued at USD 2.5 billion in 2024.

The airway management devices market is projected to grow at a CAGR of 6.5% from 2025 to 2033.

The Infraglottic devices hold the largest airway management devices market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Medtronic plc, Teleflex Incorporated, ICU Medical, Ambu A/S, KARL STORZ SE & Co. KG, Vyaire Medical, Intersurgical Ltd., Flexicare Medical, Verathon Inc., SunMed LLC.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Airway Management Devices Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Airway Management Devices Market, By Application

5.3 Airway Management Devices Market, By End User

6.1 North America Airway Management Devices Market, By Country

6.1.1 Airway Management Devices Market, By Product Type

6.1.2 Airway Management Devices Market, By Application

6.1.3 Airway Management Devices Market, By End User

6.2 U.S

6.2.1 Airway Management Devices Market, By Product Type

6.2.2 Airway Management Devices Market, By Application

6.2.3 Airway Management Devices Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping