Amniotic Membrane Market

The Amniotic Membrane Market Share & Trends Analysis Report, By Product Type (Cryopreserved Amniotic Membrane, Dehydrated Amniotic Membrane) By End-User (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics, Research Institutes) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

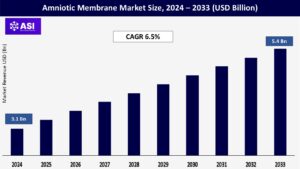

CAGR: 6.5%

Last Updated : August 29, 2025

The global Amniotic Membrane Market was valued at approximately USD 3.1 billion in 2024 and is projected to reach USD 5.4 billion by 2033, growing at a CAGR of 6.5% during the forecast period (2025–2033).

Amniotic membranes are known as biological tissues sourced from the placenta and are extensively utilized in the medical space because of their tissue anti-inflammatory, anti-scarring, and regenerative properties. Amniotic membranes are often used for wound care, surgical procedures, and ophthalmology, and provide support in healing and tissue repair. Amniotic membranes from different markets are primarily derived and practiced in two forms; cryopreserved and dehydrated membranes. Their uses range from chronic wound and burn care, to ocular surface defects, to surgical recovery. The vast majority of growth in the amniotic membrane market is driven by increasing rates of chronic wounds and ocular diseases, plus other factors such as growing knowledge of regenerative therapies, and advances in tissue preservation.

Furthermore, amniotic membrane use within the domains of orthopedics, dermatology, and gynecology are emerging, and expanding on the limited indications available. Finally, the market for amniotic membranes is growing from the increasing demands of minimally invasive treatment options.

The growing incidence of chronic wounds, such as diabetic foot ulcers, pressure ulcers, and venous leg ulcers, is significantly boosting the demand for amniotic membrane products. Chronic wounds affect millions globally and are particularly common among elderly individuals and patients with diabetes or vascular disorders. According to the American Diabetes Association, over 38 million Americans had diabetes in 2024, with 15% likely to develop foot ulcers during their lifetime.

Amniotic membranes, known for their anti-inflammatory, anti-fibrotic, and antimicrobial properties, support faster tissue repair and reduce healing time. Products like MiMedx’s EpiFix® and Organogenesis’ Affinity® are increasingly used in hospitals and outpatient wound centers to treat stubborn wounds. With U.S. Medicare spending over $30 billion annually on wound care, the economic burden is driving healthcare providers to adopt more effective regenerative therapies.

Additionally, as value-based care models prioritize better outcomes and lower readmission rates, the use of biologically active dressings like amniotic membranes is expected to expand rapidly, making chronic wound management one of the most influential application areas in this market.

Innovations in cryopreservation and lyophilization have significantly improved the usability, shelf life, and accessibility of amniotic membrane products, fueling their adoption across medical specialties. Earlier limitations in tissue viability and storage have been addressed by advanced preservation methods that retain key biological properties, such as growth factors and extracellular matrix proteins.

For instance, Integra’s AmnioGen® and Amnio Technology’s AmnioExcel® are dehydrated grafts that offer long-term storage and quick rehydration, enabling broader clinical use. Additionally, proprietary sterilization techniques—such as MiMedx’s PURION® Process—ensure safety without compromising bioactivity, making the products suitable for surgical and outpatient settings.

These advancements allow amniotic membranes to be applied beyond wound care, in areas like ophthalmology, orthopedics, and gynecology. The convenience of off-the-shelf availability, combined with consistent clinical outcomes, has encouraged surgeons and wound care specialists to adopt these biomaterials more widely. As regulatory bodies continue approving innovative formats and delivery systems, improved preservation technology is set to be a major driver of growth in the global amniotic membrane market.

A key limitation for the amniotic membrane market relates to the high treatment costs with limited reimbursement. Products that utilize amniotic membranes, especially cryopreserved and advanced dehydrated grafts, are considerably more expensive than a regular wound dressing or surgical material.

The manufacturers claim the cost of production can be so high because registered tissue banks are required to screen donors carefully, utilize advanced preservation technology and follow regulatory processes. In various countries worldwide – for example parts of Europe, Asia and Latin America – amniotic membrane products are not always reimbursed under publicly funded healthcare systems which place a burden on patients and healthcare providers.

Even in the United States, reimbursement can be inconsistent based on the indication for care, facility type, payer policies, etc. For example, some wound cares are reimbursed by Medicare while amniotic use in ophthalmology or elective surgery is often un-reimbursed. This uncertainty discourages adoption, particularly where outpatient or ambulatory care is facilitated.

As such, cost restrictions and inconsistent insurance support, directly impacts product coverage, particularly in developing regions, and restricts amniotic membrane use to high-income healthcare systems or specialty clinics with available resources.

| Report Metric | Details |

|---|---|

| By Product Type |

Cryopreserved Amniotic Membrane Dehydrated Amniotic Membrane

|

| By End-User |

Hospitals Ambulatory Surgical Centers (ASCs) Specialty Clinics Research Institutes

|

| Key Players |

MiMedx Group, Inc. Organogenesis, Inc. Celularity, Inc. BioLab Holdings, Inc. Integra LifeSciences Corporation Amnio Technology, LLC TissueTech, Inc. Osiris Therapeutics, Inc. Smith & Nephew plc MiMedx Holdings, Inc. |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Amniotic Membrane Market is segmented by product type and end-user. Each segment contributes significantly to the clinical utility and commercial success of amniotic membrane-based therapies across medical specialties.

Cryopreserved amniotic membranes had the largest market share at 62.1% in 2024, mainly because these membranes preserve a larger number of growth factors and extracellular matrix necessary for regenerative healing. Their application is also wide-ranging in the fields of ophthalmology and surgical (wound) applications where biological activity is important for healing.

Adoption of these membranes is supported by hospitals and outpatient specialty surgical centers with the capacity to accommodate the storage and utilization of cryogenic materials. Dehydrated (lyophilized) amniotic membranes will have a significantly increased growth rate over the forecast period for all regions.

The long shelf life, ease of handling and ability to use at ambient temperatures makes them very desirable especially for outpatient and ambulatory surgical centers. The ease of use and expanded indications in chronic wound care, orthopedics, and dermatology are important catalysts for growth in this segment.

Hospitals were the leading users of amniotic membranes, capturing 56.8% of the market share in 2024, primarily because hospitals are heavy users of surgical procedures, have enough storage capability, and access to the latest regenerative therapy. Hospitals have captured the market in their use of amniotic membranes in ophthalmic, reconstructive, and general surgeries.

Ambulatory Surgical Centers (ASCs) will show strong growth as they ramp up amniotic membrane products for minimally invasive procedures, wound care, and outpatient surgical procedures. ASCs lower costs and shorter turnaround times are making them the preferred environment for procedure types that have become routine.

Specialty clinics that provide care specifically for patients, encourage further market expansion. Markets for specialty clinics include, ophthalmology and wound care (careers will rapidly grow in developed countries). Specialty clinics value the regenerative and anti-inflammatory properties of amniotic membranes for treating more complicated cases, in a way that is targeted and greater efficiency of outpatient care.

Academic and research institutes represent a growing niche. Academic and research institutes have grown product volume in the amniotic membranes market as the interest in regenerative medicine for research and clinical trial applications expands into new therapeutic uses for amniotic tissues.

North America is projected to have the highest market share, at 41.2% in 2024 due to advances in healthcare infrastructure, high adoption of regenerative therapies, and growing incidence of chronic wounds. The U.S. holds the dominant position in this region due to having a greater presence of key manufacturers, spending large amounts on wound care and wound care and ophthalmology procedures, and positive reimbursement frameworks.

Products such as the EpiFix® from MiMedx and Affinity® from Organogenesis are commonly used across hospitals and outpatient clinics. The increasing diabetic population along with the aging population in North America, will also spur market growth due to increased approvals from the FDA for amniotic products.

Europe is a leading market with substantial contributions in market size from countries such as Germany, France, the UK, and Italy due to their well-structured healthcare systems, although each has in increasing aging population. A growing penetration of amniotic membranes in ophthalmology and reconstructive surgery has been contributing to the growth of the market share.

In addition, supportive public healthcare policies, plus ongoing clinical research targeting using regenerative medicine through amniotic products provides value and enhances penetration into the region. With the growing surgical procedures and chronic wounds, especially among the aging status, continue to grow among the elderly segments, the market expansion will continue to progress.

The Asia-Pacific region is expected to grow at the fastest rate, with the forecasted CAGR for the region being 7.9%. The key growth drivers include rising awareness of healthcare, increasing disposable incomes, and demand for advanced wound care, particularly in China, India, Japan, and South Korea.

Rising levels of diabetes and resulting trauma injuries are accelerating the introduction of amniotic membranes for chronic wounds. In addition, various governments are heavily investing in healthcare infrastructure improvements and local production capabilities in biotechnology, making the Asia-Pacific region a driver of market growth.

Latin America, along with the Middle East & Africa, are expected to moderate growth rates spurred by the gradual growth of healthcare infrastructure as well as increasing interest in biologic therapies. In particular, countries such as Brazil, Mexico, South Africa, and the UAE are seeing further adoption of amniotic membrane products in private hospitals and specialty clinics. Barriers to wider adoption exist in these regions, such as limited reimbursement and access to healthcare due to socioeconomic factors.

The market was valued at USD 3.1 billion in 2024.

The market is projected to grow at a CAGR of 6.5% from 2025 to 2033.

The Cryopreserved Amniotic Membrane hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include MiMedx Group, Inc., Organogenesis, Inc., Celularity, Inc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Amniotic Membrane Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Amniotic Membrane Market, By End-User

6.1 North America The Amniotic Membrane Market, By Country

6.1.1 Amniotic Membrane Market, By Product Type

6.1.2 Amniotic Membrane Market, By End-User

6.2 U.S.

6.2.1 Amniotic Membrane Market, By Product Type

6.2.2 Amniotic Membrane Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping