Antibody Drug Conjugates Market

Antibody Drug Conjugates Market Share & Trends Analysis Report, By Product (Adcertis, Kadcyla, Others), By Technology (Cleavable Linker, Non-Cleavable Linker), By Payload (MMAE, MMAF, DM1, DM4, Others), By Application (Breast Cancer, Blood Cancer, Lung Cancer, Urothelial Cancer, Others), By End User (Hospitals, Specialty Cancer Centers, Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

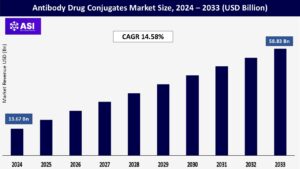

CAGR: 14.58%

Last Updated : December 16, 2025

The global antibody drug conjugates market size was valued at approximately USD 13.67 billion in 2024 and is projected to reach USD 58.83 billion by 2033, growing at a CAGR of 14.58% during the forecast period (2025–2033).

The Antibody Drug Conjugates (ADCs) market is all about making and selling a special type of medicine used mainly to treat cancer. These medicines are made by combining three parts: an antibody that finds and attaches to cancer cells, a powerful drug that kills the cancer cells, and a connector that links them together. This design helps the drug go straight to the cancer cells without harming healthy cells too much.

ADCs are known for being very accurate, releasing the drug in a controlled way, and working better than regular chemotherapy in many cases. Because of these benefits, they are being used more and more to treat cancers like breast, blood, and lung cancer. The market for ADCs is growing fast due to the increasing number of cancer cases, better technology to make these drugs, and more money being invested in this kind of treatment.

The rising global prevalence of cancer, which has created an urgent demand for more effective and targeted treatment options. Traditional cancer therapies like chemotherapy often damage healthy cells along with cancer cells, leading to severe side effects.

ADCs offer a solution by precisely targeting cancer cells and delivering powerful drugs directly to them, minimizing harm to normal tissues. As the number of cancer patients continues to grow worldwide, healthcare providers and pharmaceutical companies are increasingly turning to ADCs as a more advanced and safer alternative, which is significantly boosting the market.

The rapid advancement in biotechnology and antibody engineering. Innovations in this field have improved the stability, safety, and effectiveness of ADCs. For example, newer linkers and cytotoxic agents have made it possible to better control when and where the drug is released in the body, reducing side effects and improving patient outcomes.

Additionally, improvements in antibody selection and design have enhanced the targeting ability of ADCs, making treatments more personalized and precise. These scientific breakthroughs are encouraging pharmaceutical companies to invest heavily in ADC research and development, leading to a surge in new product approvals and market expansion.

The Antibody Drug Conjugates (ADCs) market is the high cost and complexity of development and manufacturing. ADCs are intricate molecules that require advanced technologies and highly specialized processes to produce.

Each component the monoclonal antibody, the cytotoxic drug, and the chemical linker must be carefully designed and precisely connected to ensure safety and effectiveness. This complexity leads to long development timelines and substantial research and production costs. Additionally, the regulatory approval process for ADCs is rigorous, as both the biological and chemical components must meet strict safety and efficacy standards.

These factors make it difficult for smaller biotech firms to enter the market and can limit the affordability and accessibility of ADC treatments, especially in low- and middle-income countries. As a result, despite their therapeutic potential, the widespread adoption of ADCs remains a challenge.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product |

Adcertis Kadcyla Others |

| By Technology |

Cleavable Linker Non-Cleavable Linker |

| By Payload |

MMAE MMAF DM1 DM4 Others |

| By Application |

Breast Cancer Blood Cancer Lung Cancer Urothelial Cancer Others |

| By End User |

Hospitals Specialty Cancer Centers Others |

| By Distribution Channel |

Hospital Pharmacies Retail Pharmacies Online Pharmacies |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Antibody Drug Conjugates Market is segmented by product, Technology, Payload, Application, End User and Distribution Channel. Each segment plays a vital role in enhancing patient outcomes, ensuring timely drug availability, and meeting therapeutic standards in the ticagrelor market.

Adcetris (Brentuximab Vedotin) targets CD30-positive cancers such as Hodgkin lymphoma and anaplastic large cell lymphoma. One of the first ADCs approved and widely adopted, contributing significantly to market share. Kadcyla (Trastuzumab Emtansine) approved for HER2-positive breast cancer.

Combines the HER2-targeting ability of trastuzumab with the cytotoxic agent DM1. Kadcyla remains one of the top-selling ADCs globally. Others (Enhertu, Trodelvy, Polivy, Padcev, etc.) this category includes newer ADCs with increasing clinical acceptance and use across multiple cancer types, adding diversity and innovation to the market.

Cleavable Linker dominates the market due to its ability to release the cytotoxic payload once inside the cancer cell. This type allows for more effective drug delivery and improved therapeutic outcomes. Widely used in ADCs like Adcetris and Enhertu.

Non-Cleavable Linker used in drugs like Kadcyla, these linkers require the entire antibody to degrade within the cell to release the drug. They offer better plasma stability and reduced off-target toxicity.

MMAE (Monomethyl Auristatin E) a potent antimitotic agent commonly used in ADCs such as Adcetris and Padcev. Known for high cytotoxicity and effective tumor cell killing. MMAF(Monomethyl Auristatin F) Similar to MMAE but with a lower permeability, it is designed to minimize by standard effects and increase targeted killing.

DM1 (Emtansine) used in Kadcyla, this maytansinoid inhibits microtubule formation, stopping cancer cell division. DM4 similar in function to DM1, used in experimental and emerging ADCs for improved efficacy. Others Includes new payload classes like DNA alkylating agents and topoisomerase inhibitors (e.g., deruxtecan), offering novel mechanisms for targeting and killing cancer cells.

Breast Cancer the leading application area, especially HER2-positive types. ADCs like Kadcyla and Enhertu have proven effectiveness here, driving this segment’s dominance. Blood Cancer (Hematologic Malignancies) includes leukemia, lymphoma, and multiple myeloma. ADCs like Adcetris and Polivy are standard treatments. Lung Cancer Emerging focus area with growing clinical trials and approvals, particularly in non-small cell lung cancer (NSCLC).

Urothelial Cancer Padcev has shown significant efficacy in treating bladder and urothelial cancers, contributing to the segment’s rapid growth. Others Includes solid tumors such as gastric, ovarian, and pancreatic cancers. The pipeline is expanding rapidly for these applications.

Hospitals the largest end-user segment. Due to the complexity of ADC administration and need for oncology care infrastructure, most treatments are hospital-based. Specialty Cancer Centers Provide advanced, focused cancer treatment, often using the latest ADCs as part of precision oncology approaches. Others Includes outpatient clinics and research institutions where ADCs are used in clinical trials and limited treatment settings.

Hospital Pharmacies the main distribution channel. These pharmacies handle ADCs due to the need for controlled storage and on-site administration. Retail Pharmacies used less frequently, but may be involved in outpatient ADC regimens or refills under medical supervision.

Online Pharmacies a growing segment offering convenience in ADC supply chain, especially for less complex regimens or follow-up doses, although regulatory and handling concerns still limit widespread use.

North America holds the largest share of the ADCs market, primarily due to a high prevalence of cancer, robust research and development activities, and the early adoption of innovative cancer therapies.

The presence of key pharmaceutical companies and favorable regulatory support from agencies like the U.S. FDA contribute significantly to market growth. The U.S. dominates the regional market, with a strong pipeline of clinical trials and a well-established healthcare infrastructure.

Europe is the second-largest market for ADCs, driven by strong healthcare systems, growing demand for targeted therapies, and a rising cancer burden. Countries such as Germany, France, and the United Kingdom are major contributors to the regional market. Additionally, collaborations between biotech firms and academic research institutions are accelerating product development. However, stringent regulatory approvals and pricing constraints can slow down new product launches.

Latin America is an emerging market for ADCs, with growth primarily centered in Brazil, Mexico, and Argentina. Improvements in cancer care services, rising awareness, and government-led health programs are key drivers. However, high treatment costs, limited access to biologics, and slower regulatory processes continue to pose challenges to market penetration.

The Middle East & Africa region represents a nascent but promising market for ADCs. Growth is driven by the increasing burden of cancer, expanding private healthcare investment, and advancements in medical infrastructure, especially in Gulf countries like the UAE and Saudi Arabia. In contrast, many African nations face challenges due to limited access to advanced therapies and underdeveloped healthcare systems, which hinders broader market expansion.

The antibody drug conjugates market was valued at USD 13.67 billion in 2024.

The antibody drug conjugates market is projected to grow at a CAGR of 14.58% from 2025 to 2033.

The Adcertis hold the largest antibody drug conjugates market share.

The North America and Europe region is expected to witness the highest growth rate.

Major players include Seagen Inc., Roche Holding AG (Genentech) and AstraZeneca plc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Antibody Drug Conjugates Market, By Product

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Antibody Drug Conjugates Market, By Technology

5.3 Antibody Drug Conjugates Market, By Payload

5.4 Antibody Drug Conjugates Market, By Application

5.5 Antibody Drug Conjugates Market, By End User

5.6 Antibody Drug Conjugates Market, By Distribution Channel

6.1 North America Antibody Drug Conjugates Market, By Country

6.1.1 Antibody Drug Conjugates Market, By Product

6.1.2 Antibody Drug Conjugates Market, By Technology

6.1.3 Antibody Drug Conjugates Market, By Payload

6.1.4 Antibody Drug Conjugates Market, By Application

6.1.5 Antibody Drug Conjugates Market, By End User

6.1.6 Antibody Drug Conjugates Market, By Distribution Channel

6.2 U.S.

6.2.1 Antibody Drug Conjugates Market, By Product

6.2.2 Antibody Drug Conjugates Market, By Technology

6.2.3 Antibody Drug Conjugates Market, By Payload

6.2.4 Antibody Drug Conjugates Market, By Application

6.2.5 Antibody Drug Conjugates Market, By End User

6.2.6 Antibody Drug Conjugates Market, By Distribution Channel

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping