Artificial Insemination Market

Artificial Insemination Market Share & Trends Analysis Report, By Type (Intrauterine Insemination, Intracervical Insemination, Intratubal Insemination By End User (Fertility Clinics, Hospitals, Homecare Settings, Others) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

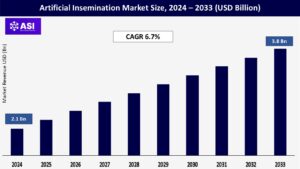

CAGR: 6.7%

Last Updated : August 13, 2025

The global Artificial Insemination Market was valued at approximately USD 2.1 billion in 2024 and is projected to reach USD 3.8 billion by 2033, growing at a CAGR of 6.7% during the forecast period (2025–2033).

Artificial insemination is an assisted reproductive method that involves the direct introduction of sperm into the cervix, uterus, or fallopian tubes to facilitate fertilization. It is the most common assisted reproductive technique across the globe for different applications in humans (infertility treatments) and animals (breeding). In humans, it is often referred to as intrauterine insemination (IUI), where sperm is introduced into the uterus, and applied when the cause for the inability to conceive in a heterosexual couple is unknown, either because of male infertility or when infertility is unexplained, or a cervical problem exists. In animals, assisted reproductive techniques (ARTs) include artificial insemination (and embryo transfer), which is important for genetic improvement and reproductive efficiency in livestock. The market is expanding due to increasing infertility rates across the global population, as well as an increasing acceptance of assisted reproductive technologies (ARTs), technology advancements in insemination devices, and an increasing use of artificial insemination in the practice of animal husbandry for reproduction management to improve breeding and overall productivity.

The increase in infertility in every country in the world is one of the most influencing factors for the growth of the artificial fertilization market. The World Health Organization (WHO) claims that approximately 1 in every 6 person in the world will face infertility at some point during their lifetime.

The increase in infertility cases is largely attributed to lifestyle factors, such as stress, poor diet, smoking, consumption of alcohol, obesity and environmental pollutants. There is also a global trend to delay parenthood, especially in urban areas, which is contributing to natural fertility rates decreasing. Many couples, like in Japan, South Korea, Italy and the U.S, are delaying having babies until their 30s or 40s because of priorities for career or finances.

The movement towards ART and artificial insemination is now dramatically increasing due to this need. For example, in January 2024 the Indian Council of Medical Research (ICMR) estimated a 12% increase from the previous year in ART procedures, with artificial insemination being amongst the most common procedures used.

Fertility clinics throughout urban areas of the Asia-Pacific, North America and Europe are increasing their programs to accommodate the increased demand for ART. Due to the lower cost, lower invasiveness, and similar success rates compared to in vitro fertilization (IVF), artificial insemination, especially intrauterine insemination (IUI), was favored because a wider population would be eligible.

The rise in the use of artificial insemination across the animal husbandry sector has now become the largest growth segment for the market, especially in countries which are mainly dependent on agriculture and livestock-based industries for their economic viability.

Artificial insemination is instrumental in enhancing the genetic quality of livestock, coupled with improving fertility rates and managing deliveries to control the spread of venereal diseases. Nations with dominating agriculture-based economies, such as Brazil, India, China, and the USA, have significantly invested in improving the utilization of artificial insemination for cattle, pigs and livestock to maintain food security, and driving increased efficiency in both dairy and meat production.

For example, in March 2024, the Ministry of Agriculture in Brazil introduced a national plan in partnership with private agribusiness companies to provide state-subsidized artificial insemination services to over 1.2 million cattle ranchers in rural Brazil; moreover, in India, the Rashtriya Gokul Mission (2023-2024) was able to perform over 21 million artificial insemination procedures with the purpose of improving the indigenous cow breeds as well as milk yield and production; in addition, technological development of AI based heat detection systems (with increased accuracy) and mobile insemination services have eased the transportability and broadened access for farmers in remote areas; all of which have become important realities in the sector.

As implementation of precision livestock farming technologies becomes increasingly commonplace, increased demand for inseminate media, catheters and cryopreserved semen is anticipated worldwide.

Even with advances in technology and some public awareness of the benefits of artificial insemination, there remains considerable reluctance to understand and accept its use, mainly in low- and middle-income countries where ethical, cultural, and religious issues prevail.

For example, social norms and religious beliefs in much of Africa, the Middle East, and South Asia, actively discourage the use of any assisted reproductive technology (ART) including artificial insemination, based on the perception of it being ‘fraudulent’ and therefore morally objectionable. For instance, some Islamic and Orthodox Christian communities condemn and sanction the use of donor sperm, directly inhibiting any potential use of intrauterine or intracervical insemination by a third-party donor `sperm, egg, or embryo’.

In addition, the emergence of ethical issues surrounding the commercialization of human reproduction, compounded by a lack of governance in some jurisdictions, has made the ethical questions surrounding artificial insemination even harder to resolve. A 2023 report by the Center for Genetics and Society announces concerns related to the commercialization and unregulated application of ART procedures (including artificial insemination) in many Southeast Asian countries, where evidence suggests many clinics are offering ART services with either no proper donor screening or no informed consent. Each of these controversial issues contributes to an overall lack of trust in ART, or willingness to proceed with artificial insemination for legitimate medical need.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Intrauterine Insemination Intracervical Insemination Intratubal Insemination

|

| By End User |

Fertility Clinics Hospitals Homecare Settings Others

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Artificial Insemination Market is segmented by type, end-user, product, animal type, and region. Each segment contributes uniquely to the advancement of reproductive technologies in both human and animal healthcare sectors.

Intrauterine Insemination (IUI) had the largest market share of 42.8% in 2024 due to its effectiveness, affordability, and less invasive procedures. IUI is generally considered the first line in treatment of mild male infertility, unexplained infertility, and cervical factor infertility, and it is especially appealing as it is most easily accessible in specialized but many fertility clinics in North America and Europe.

Intracervical Insemination (ICI) continues to exist in unique clinical scenarios and home insemination mainly due to its simplicity and relative low cost, however the success rate for ICI is generally lower than that of IUI, so its growth in a clinical environment is limited. Nevertheless, it does continue to have demand in developing areas, where the access of advanced reproductive technologies are limited.

Intratubal Insemination (ITI) despite exhibiting modest growth is a niche segment that is primarily performed at specialty within fertility centers. In practice there is potential for ITI in variable fertility therapies, however it limits itself due to the invasive procedure and cost. That said there is ongoing research to improve tubal insemination, so there is the possibility of growth in this area.

Fertility Clinics account for the majority of the artificial insemination market in 2024, with a 54.6% market share. Fertility clinics are predominant concentrated areas of assisted reproductive technology (ART), providing specialized care, access to trained professionals, and advanced tools to perform insemination procedures.

Additionally, the growth of private fertility centers, particularly in the urban areas of Asia-Pacific and Europe, will enhance segment growth. Hospitals constitute a notable portion of the market with their reproductive health departments and access to extensive diagnostic capabilities. As institutional investment continues to rise in reproductive healthcare services, hospitals are expected to play an increasing role, especially in public healthcare systems in China and Brazil.

Homecare Settings would represent a rapidly growing segment, with the availability of home insemination kits and interest on the part of patients for affordable, private fertility solutions. In developed countries such as the U.S. and Canada, a number of companies offer home and mail-order insemination kits, making self-managed insemination an option for select patient demographics.

Veterinary Clinics and Animal Breeding Centers represent another important category, primarily in the livestock and dairy sectors. Veterinary end-users are a significant driver of market revenues, particularly as countries such as India, Brazil, and the U.S. assume large-scale artificial insemination programs.

North America is expected to hold the greatest market share of 35.1% in 2024, due to a high prevalence of infertility, improved fertility treatment capabilities, and improved reimbursement policies. The United States is expected to account for most of this regional market share, with continuously increasing awareness and acceptance of assisted reproductive technologies (ART), a growing availability of fertility clinics, an increased desire for sperm donation and sperm cryopreservation, and the increased acceptance of artificial insemination as a common practice.

Artificial insemination is also widely accepted for livestock breeding, particularly in the dairy and beef industries. The presence of leading companies such as CooperSurgical, Inc. and Hamilton Thorne Ltd. will also positively impact innovation and adoption of new technologies for human and livestock fertility.

Europe represents a well-established regional market for artificial insemination due to progressive healthcare systems, favorable rules and regulations, and an increased acceptance of delayed parenthood. Major contributors include Germany, France, UK, Austria, and the Netherlands where all have a strong commitment towards fertility care and public funding for ART procedures. The region has created large artificial insemination programs, particularly in dairy food production, and have also adopted ART usage such as IVF.

According to Eurostat, ART and fertility treatments within the EU market have grown steadily over the past few years, suggesting acceptance by society and a strong government investment in fertility care and ART. These factors combined with an aging population and increased infertility rates are expected to yield substantial long-term growth in the male fertility market within Europe.

The Asia-Pacific region is forecasted to be the fastest growing thorughout the forecast period, with a CAGR of 8.3%, due to several factors prompting an increase in infertility, improved access to healthcare and increased investment from governments in livestock genetic enhancement program. China, India and Japan are the larger contributors to the region’s market growth.

In India, over 80 million cattle have been inseminated under the National Artificial Insemination Programme run by the government in 2023 demonstrating huge uptake in the veterinary sector. The human fertility sector is also experiencing a boom, with valuable opportunities arising from urbanization, cheaper services, and an increase in education around reproductive health.

Latin America and the Middle East & Africa (MEA) are emerging markets that show moderate growth, as they are beginning to invest in fertility services and agricultural development. Brazil, Argentina, and South Africa are leading the way in livestock artificial insemination programs aimed at improving the efficiency of animal production in terms of meat and milk.

Similar developments are now being seen in the human segment with people becoming more aware of fertility treatment and improving in healthcare structures although Brazil, Argentina, and South Africa have the added problem of wealth disparities and access to ART services in communities. Cultural aspects of assisted reproduction as well as ART are also a challenge for most of the countries and markets in these regions.

The market was valued at USD 2.1 billion in 2024.

The market is projected to grow at a CAGR of 6.7% from 2025 to 2033.

The Intrauterine Insemination hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include CooperSurgical, Hamilton Thorne and Irvine Scientific.

1.1 Summary

1.2 Research methodology

2.1 Particulate Adjuvants

2.2 Aluminum-Based Adjuvants

2.3 Toll- Like Receptor Agonists

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Artificial Insemination Market, By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Artificial Insemination Market, By End User

6.1 North America Artificial Insemination Market, By Country

6.1.1 Artificial Insemination Market, By Type

6.1.2 Artificial Insemination Market, By End User

6.2 U.S

6.2.1 Artificial Insemination Market, By Type

6.2.2 Artificial Insemination Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping