Artillery Market

Artillery Market Size, Market Share & Trends Analysis Report By Type (Howitzers, Mortars, Rocket Launchers, Anti-air Weapons, Naval Artillery, Coastal Artillery), By Range (Short-range, Medium-range, Long-range) By Region (North America, Europe, Asia-Pacific, Middle East and Africa, Latin America) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code : ASIADR1005

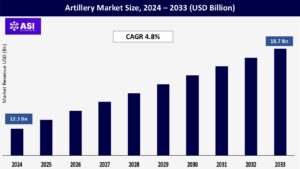

CAGR: 4.8%

Last Updated : May 8, 2026

The global Artillery Market size was valued at approximately USD 12.3 billion in 2024 and is projected to reach USD 18.7 billion by 2033, growing at a steady CAGR of 4.8% during the forecast period (2026–2033).

The market is witnessing strong demand driven by increasing geopolitical tensions, modernization of defense forces, and the need for advanced firepower solutions in both combat and non-combat operations.

Key growth drivers include the rising focus on military modernization programs, increasing defense budgets in emerging economies, and the development of next-generation artillery systems with enhanced precision, range, and mobility. The integration of advanced technologies such as automation, GPS-guided munitions, and modular designs is also shaping the future of the artillery industry.

The artillery market is experiencing growth due to increasing geopolitical tensions and the subsequent rise in defense spending across the globe. Nations are investing heavily in modernizing their armed forces to enhance operational capabilities and address evolving security threats.

The demand for advanced howitzers, multiple rocket launchers, and anti-air weapons is particularly high, as these systems play a critical role in providing firepower support in ground combat operations.

The modernization of aging artillery fleets is a key priority for many countries, especially in regions such as Asia-Pacific, the Middle East, and Eastern Europe.

For instance, countries like India, China, and South Korea are investing in indigenous artillery manufacturing capabilities, while NATO members are upgrading their artillery systems to meet modern battlefield requirements. Additionally, the increasing focus on precision strikes and long-range engagements is driving demand for advanced artillery systems.

Innovations in artillery design, automation, and munitions are significantly enhancing the performance and operational efficiency of artillery systems. Manufacturers are focusing on developing systems with modular designs, automated loading mechanisms, and advanced targeting systems to improve accuracy and reduce crew workload.

The integration of GPS-guided munitions and advanced fire control systems is revolutionizing the artillery market. These technologies enable precise targeting and reduce collateral damage, making artillery systems more effective in modern combat scenarios.

Additionally, the development of lightweight and mobile artillery systems is gaining traction, driven by the need for rapid deployment and maneuverability in diverse terrains.

Despite the advantages of advanced artillery systems, high development, acquisition, and maintenance costs pose a challenge to market expansion. The incorporation of cutting-edge technologies and the use of high-strength materials significantly increase the overall cost of artillery systems, limiting their adoption in budget-constrained regions.

Stricter export controls and regulatory challenges related to the transfer of defense technologies are impacting the global artillery market. Governments are increasingly scrutinizing defense exports to ensure compliance with international arms control agreements, which could hinder market growth.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

|

| By Application |

|

| Key Players |

BAE Systems plc Lockheed Martin Corporation General Dynamics Corporation Rheinmetall AG Hanwha Defense Nexter Group NORINCO Group Elbit Systems Ltd. IMI Systems Rostec |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The artillery market is segmented by type and range, covering a diverse set of systems designed for both offensive and defensive operations.

Howitzers remain essential for long-range, indirect fire support and are evolving with self-propelled variants and precision-guided munitions. Small, medium, and large caliber systems cater to different combat needs, with small and medium calibers often used in infantry and vehicle-mounted roles, while large calibers dominate in heavy firepower and armored platforms.

Mortars provide high-angle fire and portability, making them crucial for infantry support in rough terrain.

Rocket launchers and multiple launch rocket systems (MLRS) are valued for area saturation and extended reach, increasingly enhanced with GPS-guided munitions.

MANPADS, anti-air weapons, and air defense guns play critical roles in countering aerial threats, especially UAVs and low-flying aircraft. The growing threat from drones has also driven the adoption of C-RAM systems.

Naval and coastal artillery remain important for maritime and littoral defense, integrating modern fire control systems for improved accuracy and range.

Short-range systems (up to 20 km) such as mortars and MANPADS are ideal for mobile and urban operations.

Medium-range artillery (20–50 km) includes towed howitzers and standard MLRS, balancing firepower and maneuverability.

Long-range systems (over 50 km), like self-propelled howitzers and advanced MLRS, are increasingly prioritized for precision strike capabilities and battlefield dominance. Global demand is driven by modernization efforts, regional conflicts, and the evolving nature of hybrid warfare.

North America accounted for 36.5% of the global artillery market share in 2024, supported by the strong presence of defense contractors such as Lockheed Martin, BAE Systems, and General Dynamics. The U.S. leads the region, with high defense spending and ongoing modernization programs.

Europe holds a xx% market share, with growing demand for next-generation artillery systems in countries like the UK, Germany, and France. The region is also focusing on collaborative defense projects under the European Defence Fund (EDF).

Asia-Pacific is projected to witness the highest CAGR of 6.2% during the forecast period, fueled by rising defense budgets in China, India, and South Korea. The region is also witnessing increasing investments in indigenous artillery manufacturing capabilities.

The Middle East and Africa are emerging markets, driven by strong demand for artillery systems in Gulf countries such as Saudi Arabia and the UAE. High defense spending and ongoing conflicts are key contributors to market expansion.

Latin America is seeing steady growth, with Brazil and Mexico leading the market. The region is focusing on upgrading its artillery fleets to address internal security challenges.

The global artillery market was valued at approximately USD 12.3 billion in 2024.

The market is projected to grow at a CAGR of 4.8% from 2026 to 2033.

Key drivers include rising geopolitical tensions, defense modernization programs, and technological advancements.

Howitzers hold the largest market share due to their versatility and firepower.

The defense sector leads the market, followed by logistics and transportation.

North America holds the largest market share at 36.5%.

The Asia-Pacific region is expected to grow at a CAGR of 6.2% from 2026 to 2033.

Major players include BAE Systems, Lockheed Martin, Rheinmetall, and Hanwha Defense.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Artillery Market, By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Artillery Market, By Range

6.1 North America Artillery Market, By Country

6.1.1 Artillery Market, By Type

6.1.2 Artillery Market, By Range

6.2 U.S.

6.2.1 Artillery Market, By Type

6.2.2 Artillery Market, By Range

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping