Automotive Acoustic Material Market

Automotive Acoustic Material Market Size, Share & Industry Analysis, By Material Type (Polyurethane, Fiberglass), Vehicle Type (Passenger Cars, Commercial Vehicles), Application (Bonnet Liner, Door Trim, Other Applications) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

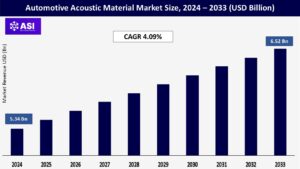

CAGR: 4.09%

Last Updated : June 12, 2026

The Automotive Acoustic Material Market size is estimated at USD 5.34 billion in 2024, and is expected to reach USD 6.52 billion by 2033, at a CAGR of 4.09% during the forecast period (2025-2030).

The automotive acoustic materials market is experiencing significant transformation driven by evolving vehicle interior design trends and changing consumer preferences.

Vehicle interiors are undergoing substantial modifications as customization and autonomous driving capabilities become increasingly prevalent, with the traditional driver role gradually transitioning into that of a passenger.

The rapid growth in electric vehicle adoption globally has emerged as a major driver for automotive acoustic materials, as EVs require specialized automotive sound dampening materials solutions. Electric powertrains consist of fewer moving parts but generate different types of noise and vibrations compared to conventional vehicles, creating unique acoustic challenges that need to be addressed.

The absence of engine noise in EVs makes other sounds more noticeable, such as road noise, wind noise, and electrical system sounds, driving the demand for advanced acoustic materials that can effectively manage these noise sources while maintaining the vehicle’s lightweight characteristics.

The automotive industry’s shift toward electrification has prompted OEMs to invest heavily in R&D for innovative acoustic material products specifically designed for electric vehicles.

The increasing consumer preference for premium and luxury vehicles has significantly boosted the demand for high-performance acoustic materials in the automotive sector. Luxury vehicle manufacturers are placing greater emphasis on interior comfort and noise reduction, making advanced acoustic solutions a crucial component of their vehicle design.

This trend is evidenced by recent developments such as the next-generation Rolls-Royce Ghost, which incorporates more than 220 pounds of sound-absorbing materials in various areas including the roof, doors, trunk, and floor to enhance the ownership experience and interior comfort.

The market’s growth is expected to be constrained by growing worries about the misuse of environmentally friendly bio-based products instead of synthetic materials that can replace current acoustic materials.

The market growth for automotive acoustic materials is being hampered by volatility in raw material prices. The price-setting procedure for every related component of an automobile is heavily influenced by the raw materials utilised in it. Likewise, the variable cost of the raw materials used to make acoustic insulators can hinder economic growth.

The raw material of an automotive component plays an important role in setting the price of the component. The price of crude oil and raw material varies across the globe. Acrylonitrile, ethylene, rubber, polyurethane, polypropylene, and fiberglass are some of the key raw materials used in the manufacturing of acoustic components.

A slowing global economy is expected to cause a declining trend in the industry. The situation has worsened due to the closure of manufacturing operations. For the past ten years, original equipment manufacturers (OEMs) have faced a matured and competitive market in all developed automotive markets, including those in Western Europe, Japan, and the United States.

These markets are characterized by stagnant demand, a proliferation of products, and price competition. Over the past few years, the need for new automobiles has decreased by less than 1% annually, and this trend is anticipated to continue.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Material Type |

Polyurethane Fiberglass |

| By Interface Type |

Passenger Cars Commercial Vehicles |

| By Access Type |

Bonnet Liner Door Trim Other Applications |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The polyurethane segment maintains its dominant position in the automotive acoustic material market, commanding approximately 35% market share in 2024. This significant market presence is attributed to polyurethane’s superior soundproofing capabilities and its extensive application in both conventional and electric vehicles.

Engine soundproofing remains a predominant application for combustion vehicles, while electric vehicles utilize this material for reducing rolling and wind noises in the passenger compartment.

Fiberglass materials are particularly valued for their durability and excellent thermal insulation properties alongside acoustic benefits, making them ideal for high-temperature applications in vehicles. The textile segment offers unique advantages in terms of lightweight solutions and flexibility in design, particularly beneficial for electric vehicle applications.

Both materials contribute to the overall acoustic performance of vehicles through different mechanisms—fiberglass through its dense structure providing automotive sound barrier, and textiles through their sound absorption capabilities.

The passenger car segment dominates the automotive acoustic material market, commanding approximately 78% of the total market share in 2024. This significant market position is driven by increasing consumer demand for quieter and more comfortable vehicle interiors, particularly in premium and luxury vehicles.

The segment’s growth is further bolstered by stringent noise regulation standards in major automotive markets and the rising adoption of electric vehicles, which require specialized acoustic solutions to address unique noise challenges.

The commercial vehicle segment plays a crucial role in the automotive acoustic material market, with manufacturers focusing on creating comfortable and noise-optimized driver cabins to enhance operator productivity and safety.

This segment has seen significant technological advancements in acoustic solutions, particularly for long-haul trucks and buses where driver comfort is paramount for extended periods of operation.

Door trim represents the largest application segment in the automotive acoustic material market, holding approximately 32% market share in 2024. The segment’s dominance is driven by increasing consumer demand for enhanced interior comfort and noise reduction in vehicles.

Modern vehicle door upholstery has evolved from being a luxury feature to becoming a standard offering in mid-segment vehicles, with manufacturers incorporating advanced acoustic materials to improve the overall driving experience.

The bonnet liner segment is emerging as the fastest-growing application segment in the automotive acoustic material market, projected to grow at approximately 4% from 2025 to 2033.

This growth is primarily attributed to the increasing focus on engine noise reduction and thermal management requirements in modern vehicles. Sound absorbers for engine covers are gaining prominence as they serve the dual purpose of dampening engine noise while functioning as heat insulators.

Other application types in the automotive acoustic material market encompass various components such as headliners, floor insulation, trunk liners, and engine compartment insulators. These applications play a crucial role in creating a comprehensive acoustic solution for vehicles, contributing to overall noise reduction and passenger comfort.

The diversity of these applications reflects the complex nature of automotive acoustic management, requiring different material properties and installation techniques depending on the specific area of application.

The Asia-Pacific region represents a dynamic market for the automotive acoustic materials market, encompassing major automotive manufacturing hubs across China, Japan, India, and South Korea.

The region’s rapid industrialization and increasing vehicle production have created substantial demand for acoustic materials. The growing middle class and increasing consumer preferences for comfortable vehicles have driven manufacturers to incorporate better acoustic solutions in their vehicles.

The European automotive acoustic materials market maintains a strong position with 23% market shares globally, supported by the presence of major automotive manufacturers across Germany, the United Kingdom, and France.

The region’s stringent noise emission regulations and high consumer expectations for vehicle comfort have created a sophisticated market for acoustic materials. The increasing focus on electric vehicle production has led to new developments in acoustic solutions specifically designed for electric powertrains. The region’s emphasis on sustainable manufacturing practices has also influenced innovation in eco-friendly acoustic materials.

The United States leads the North American market with approximately 64% market share in 2024. The country’s market is driven by strong domestic automotive production and increasing consumer preference for quieter vehicle cabins.

Major global players are actively investing in the region to expand their market presence and stay ahead of competitors. The country’s push towards electric vehicles has created new opportunities for automotive acoustic insulation manufacturers, as EVs require specialized solutions for road noise and vibration control.

The current market size is USD 5.34 Billions in 2024.

The HMI Market is growing at a CAGR of 6.52% during forecasting period 2025-2033.

Asia Pacific region held the highest share in 2025.

Dow Chemicals, 3M Acoustics, BASF SE, Covestro and Henkel Adhesive Technologies are the major companies operating in the Automotive Acoustic Material Market.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Automotive Acoustic Material Market, By Material Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Automotive Acoustic Material Market, By Interface Type

5.3 Automotive Acoustic Material Market, By Access Type

6.1 North America Automotive Acoustic Material Market, By Country

6.1.1 Automotive Acoustic Material Market, By Material Type

6.1.2 Automotive Acoustic Material Market, By Interface Type

6.1.3 Automotive Acoustic Material Market, By Access Type

6.2 U.S.

6.2.1 Automotive Acoustic Material Market, By Material Type

6.2.2 Automotive Acoustic Material Market, By Interface Type

6.2.3 Automotive Acoustic Material Market, By Access Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping