Automotive Airbag Market

Automotive Airbag Market Share & Trends Analysis Report By Airbag Type (Frontal Airbags, Side Airbags, Knee Airbags, Curtain Airbags), By Vehicle Type (Passenger Cars, Commercial Vehicles, Electric Vehicles), By Distribution Channel (OEM, Aftermarket), By Region (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2024–2032

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code : ASIATR1004

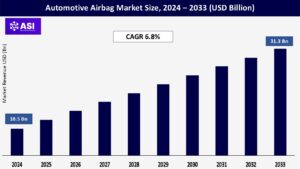

CAGR: 6.8%

Last Updated : May 19, 2026

The global Automotive Airbag Market size was valued at approximately USD 18.5 billion in 2024 and is expected to reach USD 31.3 billion by 2033, growing at a CAGR of 6.8% during the forecast period (2026–2033).

Automotive Airbag are inflatable cushions built into a vehicle that protect occupants from hitting the vehicle interior or objects outside the vehicle (for example, other vehicles or trees) during a collision. The instant a crash begins, sensors start to measure impact severity.

The increasing demand for vehicle safety features is primarily driven by stringent government regulations and growing consumer awareness regarding passenger safety. The market is witnessing advancements in airbag technologies, with manufacturers focusing on lightweight materials and smart deployment systems.

The Automotive Airbag Market Growth is further fueled by the increasing sales of passenger vehicles and commercial vehicles, along with the rising adoption of electric vehicles (EVs). Moreover, growing investments in R&D for advanced airbag systems, such as external airbags and pedestrian protection airbags, are contributing to market expansion.

Governments worldwide are implementing strict safety norms that mandate the installation of airbags in vehicles. According to the World Health Organization (WHO), approximately 1.35 million people die each year due to road accidents, and an additional 20-50 million suffer non-fatal injuries.

To combat this, regulatory bodies such as the National Highway Traffic Safety Administration (NHTSA) in the U.S. have made it mandatory for all passenger vehicles to be equipped with airbags. The European New Car Assessment Programme (Euro NCAP) has also established strict crash safety standards, pushing automakers to integrate advanced airbag systems.

For instance, in 2022, India’s Ministry of Road Transport and Highways (MoRTH) mandated six airbags for passenger vehicles carrying up to eight passengers, a move aimed at improving crash safety in the country.

Additionally, the UN Economic Commission for Europe (UNECE) has introduced Regulation No. 94, which makes frontal crash protection, including airbags, compulsory in new vehicles. These regulations are compelling automakers worldwide to invest in next-generation airbag systems, accelerating market growth.

Regulatory bodies such as the National Highway Traffic Safety Administration (NHTSA) in the U.S. and the European New Car Assessment Programme (Euro NCAP) have introduced stringent crash safety ratings, influencing automakers to integrate advanced airbag systems. The growing focus on pedestrian safety has also led to the development of external airbags and advanced airbag modules.

Automotive manufacturers are investing in innovative airbag technologies, such as smart airbags with advanced sensors, adaptive deployment mechanisms, and AI-based crash detection systems.

These innovations are improving the efficiency of airbag deployment, reducing injury risks, and enhancing overall vehicle safety. Smart airbags, which adjust inflation levels based on crash severity and occupant position, are becoming standard in high-end SUVs and electric vehicles.

Automakers such as Honda, BMW, and Ford have developed motorcycle airbags, further expanding the airbag market beyond passenger vehicles. Modern vehicles are being equipped with multiple airbags, including frontal airbags, side airbags, curtain airbags, and knee airbags, to enhance occupant protection during collisions.

Additionally, the introduction of rear-seat airbags by Mercedes-Benz and Hyundai is expected to revolutionize safety in premium and family-oriented cars.

Airbag system malfunctions, including improper deployment and sensor failures, have resulted in major product recalls in the past. Such incidents impact consumer trust and pose challenges for manufacturers in ensuring product reliability.

Despite their benefits, advanced airbag systems increase the overall cost of vehicles, which may impact their adoption in price-sensitive markets. The development and integration of intelligent airbag modules require substantial investments, limiting their penetration in low-cost vehicle segments.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Airbag Type |

Frontal Airbags Side Airbags Knee Airbags Curtain Airbags |

| By Vehicle Type |

Passenger Cars Commercial Vehicles Electric Vehicles |

| By Distribution Channel |

OEM Aftermarket |

| Key Players |

Autoliv Inc. ZF Friedrichshafen AG Toyoda Gosei Co., Ltd. Hyundai Mobis Co., Ltd. Joyson Safety Systems Nihon Plast Co., Ltd. Ashimori Industry Co., Ltd. Daicel Corporation Continental AG Denso Corporation |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The global automotive airbag market is segmented based on airbag type, vehicle type, distribution channel, and regional analysis. Each segment contributes significantly to the market’s overall growth and revenue generation.

Frontal airbags accounted for the largest market share of approximately 42.6% in 2024, as they are mandated in most vehicles worldwide. Designed to protect drivers and front-seat passengers in frontal collisions, these airbags deploy from the steering wheel and dashboard.

The growing emphasis on driver and passenger safety continues to drive demand for frontal airbags in both passenger and commercial vehicles. The side-impact airbag segment held a market share of XX% in 2024, with increasing adoption in compact and mid-sized vehicles.

These airbags provide protection against side collisions and are often installed in doors or seats. The rising number of side-impact crashes has led to a surge in demand for these airbags, particularly in urban environments.

Curtain airbags deploy from the roof lining and cover the vehicle’s side windows to protect occupants’ heads in rollover or side-impact crashes. Their growing incorporation in SUVs and high-end sedans is fueling segment growth.

Knee airbags protect passengers’ lower limbs in frontal crashes and are increasingly included in premium and luxury vehicles. Automakers like Mercedes-Benz, Audi, and BMW are actively integrating knee airbags to enhance safety ratings.

Although currently a niche segment with 6.2% market share, pedestrian airbags are gaining traction, particularly in regions emphasizing pedestrian safety regulations. These airbags deploy externally to reduce impact severity in pedestrian collisions. European countries, in particular, are seeing increased adoption due to regulatory policies.

The passenger vehicle segment dominated the market, accounting for 68.2% of total revenue in 2024. Increasing consumer preference for enhanced safety features in sedans, hatchbacks, and SUVs is driving airbag installation. In particular, SUVs are witnessing the highest growth, with manufacturers equipping them with multiple airbags for better occupant protection.

The HCV segment constituted xx% of the market. Although traditionally lagging in airbag adoption, growing safety awareness and stricter road safety laws are leading to increased integration in buses and trucks.

The OEM segment dominates market share in 2024, as most airbags are factory-installed in new vehicles. Automakers are actively collaborating with airbag manufacturers to integrate advanced safety systems and comply with regulatory standards.

Increasing vehicle recalls, replacements due to wear and tear, and growing consumer preference for retrofitted safety enhancements contribute to aftermarket demand.

North America accounted for 32.1% of the global automotive airbag market in 2024, driven by stringent NHTSA safety regulations and high consumer awareness. The presence of key players like Autoliv Inc., ZF Friedrichshafen AG, and Joyson Safety Systems supports regional market growth.

Europe captured significant market share in 2024, with Germany, France, and the UK leading in airbag adoption. Euro NCAP safety ratings and stringent EU regulations are key drivers, compelling automakers to incorporate advanced airbag systems in vehicles.

Asia-Pacific is the fastest-growing region, with a CAGR of 7.2% in 2024. Rising vehicle production, government mandates in countries like India and China, and growing consumer demand for safer vehicles are fueling market expansion.

MEA and Latin America held 13.2% of the market. Although airbag adoption is lower compared to other regions, growing regulatory efforts and luxury vehicle demand are supporting steady growth. Brazil and Mexico being major contributors due to increasing vehicle production and safety regulations.

The Global Automotive Airbag Market was valued at USD 18.5 billion in 2024.

The market is projected to grow at a CAGR of 6.8% from 2026 to 2033.

The Passenger Vehicle segment holds the largest market share.

The Asia-Pacific region is expected to witness the highest growth.

Major players include Autoliv Inc., ZF Friedrichshafen AG, and Toyoda Gosei Co., Ltd.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Automotive Airbag Market, By Airbag Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Automotive Airbag Market, By Vehicle Type

5.3 Automotive Airbag Market, By Distribution Channel

6.1 North America Automotive Airbag Market, By Country

6.1.1 Automotive Airbag Market, By Airbag Type

6.1.2 Automotive Airbag Market, By Vehicle Type

6.1.3 Automotive Airbag Market, By Distribution Channel

6.2 U.S.

6.2.1 Automotive Airbag Market, By Airbag Type

6.2.2 Automotive Airbag Market, By Vehicle Type

6.2.3 Automotive Airbag Market, By Distribution Channel

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping