Automotive Blockchain Market

Automotive Blockchain Market Size, Share & Trends Analysis Report By Function (Smart Contracts, Supply Chain), By Provider (Middleware Provider, Infrastructure & Protocol Provider, Application & Solution Provider), By Mobility (Personal Mobility, Shared Mobility, Commercial Mobility) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

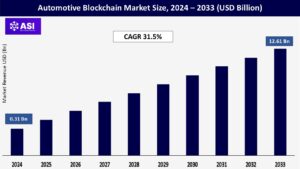

CAGR: 31.5%

Last Updated : June 12, 2026

The global Automotive Blockchain Market Size was valued at USD 0.31 billion in 2024 and is expected to grow from USD 0.44 billion in 2025 to reach USD 12.61 billion by 2033, growing at a CAGR of 31.5% during the forecast period (2025-2033).

Blockchain is characterized as a technology that is transparent to the public and uses decentralized unanimity to maintain a network. The absence of centralized management by organizations like businesses, governments, or banks introduces high levels of data transmission security.

This technology is being used by many industries, including BFSI, manufacturing, telecom, and healthcare, to improve cost and accountability. A few sectors that have benefited from Blockchain (BC) technology include manufacturing, commerce, finance, healthcare, automotive, and supply chain.

Automotive professionals are interested in what blockchain might do for the automotive ecosystem, including how it might simplify participant engagement and open the door to new mobility business models. In addition to offering a single data source, blockchain can support device-to-device transactions, smart contracts, real-time processing, and settlement.

Gains and increased operational effectiveness result in supply chain transparency, financial transactions among ecosystem participants, confirming vehicle access, and improved customer satisfaction and loyalty in the automotive industry. The development of new industrial business models, such as those involving alternative ownership, car usage, rewards programs, and other mobility services that boost brand appeal and loyalty, can also be aided by blockchain technology.

Porsche, for instance, is testing blockchain applications for use in cars, including the ability to lock and unlock the car using an app, grant temporary access permissions, and look into new business models based on encrypted data logging. Blockchain features, such as consumer authentication and usage tracking across numerous mobility services, allow businesses to design customized customer experiences that result in lifelong customers.

In the automotive sector, blockchain technology is still in its infancy, and governing bodies worldwide have historically found it challenging to keep up with these developments. Since this technology is decentralized, no government, organization, or person can control and impose regulations on the blockchain.

The General Data Protection Regulation (GDPR) was implemented across all of the European Union’s (EU) member states. The “right to be forgotten” is allowed under this regulation, as is data privacy. This calls into question the technology’s immutability and decentralization. Thus, regulatory ambiguity is a constraining factor that slows market expansion.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Function Type |

Smart Contracts Supply Chain |

| By Provider Type |

Middleware Provider Infrastructure & Protocol Provider Application & Solution Provider |

| By Mobility Type |

Personal Mobility Shared Mobility Commercial Mobility |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The supply chains segment is the highest 35% contributor to the market and is expected to grow at a CAGR of 32.1% during the forecast period. This is a result of rising auto sales and the development of electric vehicles, which are anticipated to strengthen the supply chain industry globally.

Furthermore, the market for smart contracts is anticipated to grow at a rapid rate. The automotive industry, where smart contracts are used for B2B contracts, dealership management, and title transfer, is primarily responsible for the segment’s fastest growth.

In 2024, the Smart Contracts segment held a dominant market position in the automotive blockchain market, capturing more than a 35% share. This leading stance is attributed primarily to the inherent benefits of smart contracts in automating and streamlining transactions and operations across the automotive industry.

These blockchain-based contracts execute automatically when agreed-upon conditions between parties are met, thereby minimizing the need for intermediaries and reducing administrative costs and time.

Application and solution lead the market in 2024 due to its broad utility across various industry processes. This segment includes blockchain-enabled solutions for supply chain management, secure payment systems, and vehicle identity verification.

Its capability to streamline operations, reduce fraud, and enhance data accuracy has driven widespread adoption. Additionally, the integration of blockchain in applications such as smart contracts for leasing agreements and warranty management underscores its transformative potential.

In 2024, the Infrastructure and Protocols segment held a dominant market position within the Automotive Blockchain Market, capturing more than a 44% share. This segment’s leadership stems from its critical role in providing the foundational technologies necessary for implementing blockchain across various automotive applications.

Infrastructure and Protocols segment includes the core technologies that enable blockchain’s functionality: distributed ledger technology (DLT), consensus algorithms, and cryptographic security. The middleware segment is expected to grow significantly from 2025 to 2033.

The middleware segment is evolving to address the complexities of integrating blockchain technology with existing IT infrastructures. Middleware solutions act as intermediaries between applications and infrastructure components, facilitating data exchange and communication across diverse platforms.

Personal mobility is projected to be the largest segment of the blockchain market for automotive, by mobility type. Strong economic growth, increasing population, rapid urbanization, and growing purchasing power have triggered the demand for personal mobility across the globe.

As passenger car production and sales constitute the largest share of the revenue generated by all industry participants, the applications of blockchain are also projected to generate maximum revenues from the production, sales, and services related to passenger cars or personal mobility.

The commercial mobility segment has the highest growth rate. Although its current level of implementation might be slightly lower than the case with the shared mobility, the segment has steadily been receiving more attention and has been implementing more of the blockchain solutions.

Shared mobility, which encompasses ride-hailing, car sharing and carpooling services, involve multiple stakeholders who transact securely through an online platform, including service providers, drivers, and consumers.

This sector is dominant because many travels and shared trips occur globally, and blockchain provides efficient transactions, identity verification, and hence enhances the trust of the parties using shared mobility systems.

APAC is holds the 29% market shares of the global market. Asia Pacific is expected to grow at a CAGR of 32% during the forecast period. China, India, Japan, Australia, and the rest of Asia-Pacific are all included in the analysis of the Asia-Pacific automotive blockchain market.

The area has transformed into a hub for the manufacture of automobiles in recent years. The region’s demand for automobiles has been fueled by the region’s rapid economic growth, expanding population, growing urbanization, and greater purchasing power.

The expanding automotive industry will use blockchain technology in the Asia Pacific to increase transparency and thwart fraud. However, China and India, the two largest markets for transportation products, can integrate blockchain technology into ridesharing apps.

The Europe is the most 32% significant global automotive blockchain market shareholder. The rapid growth in electric vehicle adoptions in Europe is a significant growth driver for the automotive blockchain market.

According to International Energy Agency, new registrations of electric cars in Europe exceeded nearly 3.2 Million for 2024, showing an approximate 20% increase as compared with 2023.

North America is the largest 37% shares of the global automotive blockchain market shareholder and is expected to grow at a CAGR of 31.1% during the forecast period. The U.S. and Canada are included in the analysis of the automotive blockchain market in North America.

The growth would typically be fueled by two significant factors: the growing demand for immutability and transparency in business processes and significant investments in the blockchain platform by software providers.

SHIFTMobility unveiled the first blockchain-powered platform for the automotive industry. The platform would enable connection, comprehension, and harness demand from various vehicles and supply chain apps, commerce channels, better diagnostics, and transportation logistics both now and in the autonomous future.

Rising government efforts to construct electric vehicle (EV) charging infrastructure in the Middle East and Africa (MEA) will significantly increase the automotive blockchain market. For instance, as of August 2022, Saudi Arabia’s Ministry of Industry and Mineral Resources announced an investment of over USD 6 Billion to enhance battery mineral mining and support the EV supply chain.

This initiative promotes the expansion of the EV ecosystem, requiring the need for blockchain solutions for more transparency, security, and efficiency in tracking EV parts and transactions.

The market is expected to grow CAGR of 31.5% from 2025 to 2033.

The current market size is USD 0.31Billions in 2024.

North America currently holds the largest market shares.

Asia Pacific has the highest growth in the global market.

IBM Corporation, Microsoft, Carvertical, Helbiz, Tech Mahindra, HCL Technologies, Xain.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Automotive Blockchain Market, By Function Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Automotive Blockchain Market, By Provider Type

5.3 Automotive Blockchain Market, By Mobility Type

6.1 North America Automotive Blockchain Market , By Country

6.1.1 Automotive Blockchain Market, By Function Type

6.1.2 Automotive Blockchain Market, By Provider Type

6.1.3 Automotive Blockchain Market, By Mobility Type

6.2 U.S.

6.2.1 Automotive Blockchain Market, By Function Type

6.2.2 Automotive Blockchain Market, By Provider Type

6.2.3 Automotive Blockchain Market, By Mobility Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping