Automotive Drive Shaft Market

Automotive Drive Shaft Market Size, Share & Trends Analysis Report By Design Type (Hollow Shaft, Solid Shaft), By Application Type (Rear Axle, Front Axle), By Vehicle Type (Passenger Car, Commercial Vehicles) Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

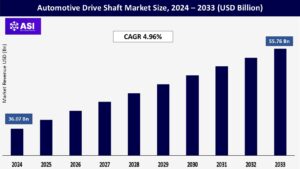

CAGR: 4.96%

Last Updated : June 15, 2026

The global Automotive Drive Shaft Market size was valued at USD 36.07 billion in 2024 and is expected to grow from USD 37.85 billion in 2025 to reach USD 55.76 billion by 2033, growing at a CAGR of 4.96% during the forecast period (2025-2033).

A drive shaft, also known as a propeller or Cardan shaft, is a mechanical part used to deliver torque and power to a vehicle’s powertrain, more especially to the vehicle’s back wheels. Drive shafts’ primary function is to transfer torque from one or more vehicle components to other parts of the vehicle.

Driveshafts for automobiles are more reliable and rarely need maintenance. Automotive drive shafts also provide low maintenance costs, smooth operation, no oil leaks, reliability, and clean operation. Different drive shaft arrangements are used in vehicles with independent front-wheel drive, four-wheel drive, and front-engine rear-wheel drive.

The automotive industry is witnessing a significant transformation with the rising adoption of electric and hybrid vehicles, driven by increasing environmental concerns and stringent emission regulations.

According to the International Energy Agency, electric car sales demonstrated robust growth of approximately 25% in Q1 2024 compared to Q1 2023, with China commanding the largest market share at 45%, followed by Europe at 25%.

This surge in electric vehicle adoption has prompted automotive drive shaft manufacturers to develop specialized components that can handle the unique characteristics of electric powertrains, including high torque output at low speeds and the need for lightweight components to maximize vehicle range and efficiency.

The regulatory landscape is playing a crucial role in accelerating this transition, particularly in Europe where the EU Council’s “Directive 96/62/EC on ambient air quality assessment and management” has established strict emission targets.

The European Commission has set an ambitious target of having at least 30 million electric vehicles on European roads by the end of this decade, representing a substantial increase from the current 1.4 million EVs. In response to these evolving market demands, manufacturers are innovating their automotive powertrain technologies.

For instance, in January 2023, Kalyani Mobility Drivelines (KMD) introduced a new lineup of constant-velocity (CV) driveshafts specifically designed for EVs and specialty vehicles, demonstrating the industry’s commitment to supporting the electric vehicle transition with advanced drivetrain solutions.

The global automotive market is experiencing a substantial shift in consumer preferences towards SUVs and light trucks, driven by demands for increased versatility, comfort, and performance capabilities.

This trend is exemplified by the introduction of high-performance models such as the Land Rover Range Rover Sport SV in May 2023, which features a powerful 635 hp supercharged 5-liter V8 engine, demonstrating the growing consumer appetite for premium SUVs with enhanced performance characteristics.

The increasing demand for these larger vehicles has prompted automotive drive shaft manufacturers to develop more robust and sophisticated components capable of handling higher torque requirements while maintaining efficiency and reliability.

The high replacement cost and the erratic prices of the raw materials used to make vehicle drive shafts in high-volume markets will act as market restraints and slow the industry’s growth.

The complex process of installing and reinstalling drive shafts is one of the main factors impeding the market’s expansion. Additionally, the damaged system is beyond repair and requires a complete replacement.

Automotive drive shafts are made from a wide variety of raw metals such as steel, iron, and even titanium alloys. The price of these raw materials is subject to extreme volatility due to changes in the commodity market, which makes it challenging for automotive drive shaft companies to develop products with a defined profit margin.

There is a huge number of companies that provide drive shafts of various shapes, sizes, and functionality, which has created a highly saturated market for any kind of drive shaft. This saturation is estimated to create pricing pressure and even hurt automotive drive shaft market growth to a certain extent in the future.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Design Type |

Hollow Shaft Solid Shaft |

| By Application Type |

Rear Axle Front Axle |

| By Vehicle Type |

Passenger Cars Commercial Vehicle |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The solid shaft segment continues to dominate the automotive driveshaft market, commanding approximately 66% market share in 2024. This significant market position is attributed to solid shafts’ superior capabilities in power transfer and enhanced bending properties.

Solid shafts are particularly preferred for torque transmission applications like crankshafts and driveshafts due to their higher torsional stiffness. The segment’s dominance is further reinforced by its widespread adoption in commercial vehicles and heavy-duty applications where reliability and durability are paramount.

Solid shafts have established themselves as the go-to choice for high-performance vehicles, sports cars, and luxury vehicles that require robust driveshafts capable of handling high torque while delivering a smoother driving experience. Their proven track record in off-road vehicles such as SUVs and trucks has also contributed to their market leadership.

The hollow shaft segment is emerging as the fastest-growing segment in the automotive driveshaft market, projected to grow at approximately 7% during 2025-2033. This growth is primarily driven by the increasing demand for lightweight vehicle components that enhance fuel efficiency without compromising performance.

The segment’s expansion is further accelerated by stringent carbon emission regulations and the growing adoption of electric and hybrid vehicles. Manufacturers are increasingly investing in R&D activities to improve hollow shaft designs, focusing on enhanced flexibility and high-performance characteristics.

The technological advancements in hollow shaft manufacturing, particularly in cold extrusion processes, are enabling the production of shafts that weigh significantly less than traditional options while maintaining structural integrity.

This innovation trajectory, coupled with the automotive industry’s shift towards more fuel-efficient and environmentally friendly vehicles, is positioning hollow shafts as a crucial component in modern vehicle design.

The rear axle segment continues to dominate the automotive driveshaft market, commanding approximately 54% of the market share in 2024. This significant market position is primarily attributed to the segment’s crucial role in rear-wheel drive vehicles and its widespread application in heavy-duty vehicles.

Rear axle driveshafts are particularly essential in vehicles requiring high torque transmission and improved traction capabilities, making them indispensable in SUVs, trucks, and high-performance vehicles. The placement of rear axles in automobiles is strategically determined by the gross weight of the vehicle, with large heavy-duty vehicles weighing over 8,500 lb typically equipped with two rear axles.

This configuration is particularly beneficial for large-weight hauling applications and has become increasingly important with the growing demand for commercial vehicles and logistics operations of heavy-weight equipment. The front axle segment is emerging as the fastest-growing segment in the automotive driveshaft market, projected to grow at approximately 7% CAGR from 2025 to 2033. This growth is primarily driven by the increasing demand for SUVs and crossovers, which require front axle driveshafts to transfer power from the engine to the front wheels.

The segment’s growth is further accelerated by changing consumer preferences and lifestyles, leading to a shift towards larger and more versatile vehicles. Technological advancements have also contributed significantly to this growth, with modern front axle driveshafts being designed to be more robust, lightweight, and fuel-efficient. The segment is particularly benefiting from the rising adoption of electric vehicles, as manufacturers focus on developing specialized front axle driveshafts that can handle the unique torque characteristics of electric powertrains while maintaining optimal performance and efficiency.

The passenger cars segment continues to dominate the automotive driveshaft market, commanding approximately 58% market share in 2024, driven by increasing global vehicle production and stringent regulations related to vehicular and passenger safety across major economies.

This segment’s leadership position is reinforced by the growing adoption of electric and hybrid vehicles in the passenger car category, which require specialized automotive drivetrain components to handle their unique powertrain configurations.

The segment is also experiencing the fastest growth trajectory, projected to expand at around 7% through 2025-2033, propelled by technological innovations in driveshaft design for electric vehicles and the rising demand for all-wheel-drive passenger vehicles. The commercial vehicles segment represents a significant portion of the automotive driveshaft market, driven by the expanding e-commerce sector and increasing demand for logistics and transportation services globally.

This segment is characterized by the need for heavy-duty and highly durable driveshaft systems that can withstand intense usage patterns and heavy loads. The growth in this segment is being fueled by the increasing adoption of electric commercial vehicles, with companies like Tesla, BYD, Volvo, and Mercedes-Benz developing electric truck models that require specialized automotive axle shaft solutions.

The segment is also benefiting from technological advancements in driveshaft materials and designs, specifically engineered to enhance the performance and reliability of commercial vehicles.

In 2024, Asia-Pacific accounted for the largest market share of over 36.4%. Asia Pacific is the dominant regional split in the automotive drive shaft market due to high-speed industrialization, urbanization, and increased vehicle manufacturing in nations such as China, India, Japan, and South Korea.

Asia Pacific is home to some of the world’s largest auto manufacturing bases that are backed by robust government policies for increasing local production and export capacities.

The demand for electric vehicles, commercial trucks, and passenger cars—all of which require reliable and efficient drive shafts—has increased due to inflating income levels and sizable middle classes. Furthermore, the growing uptake of electric vehicles in Asia Pacific is driving faster demand for customized drive shafts to cater to electric powertrains.

Europe is showing heightened automotive drive shaft adoption due to growing vehicle ownership across the region. For instance, in 2024, there were 12,963,614 new passenger cars registered in Europe (EU, EFTA, UK), with an increase of 0.9%.

The increase in personal transportation needs, combined with expanding suburban populations, is contributing to elevated vehicle purchases. Demand for passenger and commercial vehicles is translating into a greater need for efficient and durable drive shafts. As consumers seek high-performance and fuel-efficient vehicles, drive shaft manufacturers are optimizing materials and design to meet evolving standards.

Middle East and Africa is experiencing growth in automotive drive shaft adoption owing to growing urban population and rising demand in electric and autonomous vehicles. For example, it is anticipated that there would be 7,331 electric cars (EVs) in the United Arab Emirates as of 2023, with the majority of them being in Dubai.

This number is anticipated to increase dramatically, with estimates putting the number of EVs at 12,852 by 2025. The need for both private and shared transportation options is rising as metropolitan areas expand.

The market is expected to grow CAGR of 4.96 % from 2025 to 2033.

The current market size is USD 36.07 Billions in 2024.

Asia Pacific currently holds the largest market shares.

Some of the major players in the automotive drive shaft market include Advanced Composite Products & Technology Inc., American Axle & Manufacturing Inc., Dana Incorporated, Hyundai Wia Corporation (Hyundai Motor Group), IFA Group, JTEKT Corporation, Melrose Industries PLC, Meritor Inc. (Cummins Inc.), Neapco Inc., Nexteer Automotive, NKN Ltd., NTN Corporation, etc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Automotive Drive Shaft Market, By Design Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Automotive Drive Shaft Market, By Application Type

5.3 Automotive Drive Shaft Market, By Vehicle Type

6.1 North America Automotive Drive Shaft Market, By Country

6.1.1 Automotive Drive Shaft Market, By Design Type

6.1.2 Automotive Drive Shaft Market, By Application Type

6.1.3 Automotive Drive Shaft Market, By Vehicle Type

6.2 U.S.

6.2.1 Automotive Drive Shaft Market, By Design Type

6.2.2 Automotive Drive Shaft Market, By Application Type

6.2.3 Automotive Drive Shaft Market, By Vehicle Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping