Automotive Fuel Cell Market

The Automotive Fuel Cell Market report segments the industry into Electrolyte Type (Polymer Electronic Membrane Fuel Cell, Direct Methanol Fuel Cell, Alkaline Fuel Cell), Vehicle Type (Passenger Cars, Commercial Vehicles), Fuel Type (Hydrogen, Methanol), Power Output (Below 100 KW, 100-200 KW, Above 200 KW) market Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

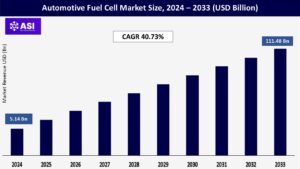

CAGR: 40.73%

Last Updated : January 16, 2026

The global automotive fuel cell system market size was valued at USD 5.14 billion in 2024 and is expected to grow from USD 7.24 billion in 2025 to reach USD 111.48 billion by 2033, growing at a CAGR of 40.73% during the forecast period (2025-2033).

A fuel cell vehicle is a type of electric vehicle that powers its onboard electric motor using a fuel cell, alone or in conjunction with a battery or supercapacitor. The motor is powered by electricity from a fuel cell as well. In order to function, fuel cells typically require compressed hydrogen and airborne oxygen.

Fuel cells typically produce heat and water, so these fuel cell cars are referred to as zero-emission cars. Automakers see automotive fuel cell technology as an appealing proposition, enabling them to produce high-energy cells that can power automobiles. Methane or hydrogen is the primary source of energy for fuel cells.

Governments and environmental agencies are passing strict emission norms and laws in response to growing environmental concerns, which is anticipated to drive up the cost of producing fuel-efficient diesel engines in the future. As a result, the new commercial vehicle diesel engine segment is anticipated to experience slow growth soon.

Additionally, traditional commercial vehicles powered by fossil fuels, trucks, and buses are to blame for increased transportation emissions. Heavy commercial vehicle emissions are expected to decrease with fuel-cell commercial vehicles, regarded as zero-emission or low-emission vehicles.

A significant factor anticipated to propel the market for fuel cell commercial vehicles is initiatives by government bodies around the world to choose green energy mobility to curtail and curb transportation pollution.

Government initiatives worldwide are playing a crucial role in accelerating the adoption of automotive fuel cell systems through various support mechanisms and infrastructure development programs.

In February 2022, Japan’s Ministry of the Environment announced its support for establishing hydrogen business consortiums, implementing a hydrogen supply chain platform that generates low-carbon hydrogen.

Similarly, the Indian Ministry of New and Renewable Energy has implemented the ‘Renewable Energy Research and Technology Development’ program, supporting research in hydrogen-based transportation and fuel cell development, including the establishment of production facilities for high-purity hydrogen generation.

The commitment to hydrogen infrastructure development is further evidenced by substantial investments and research initiatives. The German government’s support for the CryoTRUCK project, with a budget exceeding EUR 25 million, demonstrates the focus on developing advanced hydrogen storage and refueling systems for heavy-duty fuel cell trucks.

In Europe alone, there are over 314 hydrogen-related project proposals, with approximately 268 aiming for full or partial commissioning through 2030, representing about 30% of proposed hydrogen investments globally (approximately USD 76 billion).

These initiatives are complemented by programs like H2BusEurope, which aims to deploy 1,000 hydrogen buses and supporting infrastructure, showcasing the comprehensive approach to developing the hydrogen mobility ecosystem.

The absence of a hydrogen infrastructure is the main barrier preventing the introduction of various fuel cell vehicles on the international market. One of the reasons there aren’t as many hydrogen refueling stations worldwide is that producing hydrogen using traditional methods requires much money and produces many emissions, making it challenging to comply with the strict requirements of the Energy Policy Act.

It is costly to build a new hydrogen refueling infrastructure (but not costlier than establishing a methanol or ethanol infrastructure). Natural gas can produce hydrogen, which can be more affordable than gasoline.

Unless low-cost off-peak electricity is used or solar panels are used, the cost of producing hydrogen from water and electricity through hydrolysis is higher than the cost of producing gasoline using conventional methods.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Electrolyte Type |

Polymer Electronic Membrane Fuel Cell Direct Methanol Fuel Cell Alkaline Fuel Cell |

| By Vehicle Type |

Passenger Cars Commercial Vehicles |

| By Fuel Type |

Hydrogen Methanol |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Polymer Electronic Membrane Fuel Cell (PEMFC) segment has established itself as the dominant technology in the automotive fuel cell system market, commanding approximately 91% of the market share in 2024.

This overwhelming market leadership is attributed to PEMFC’s superior energy conversion efficiencies, reliability, and clean by-product production capabilities. Major automotive manufacturers have shown a strong preference for PEMFC technology due to its proven track record in both passenger and commercial vehicle applications.

The technology’s ability to operate efficiently at lower temperatures, quick start-up capabilities, and compact design make it particularly suitable for automotive applications.

Recent developments in PEMFC technology have focused on reducing platinum usage in catalysts while improving power density, making the technology more cost-effective for mass production. The Direct Methanol Fuel Cell (DMFC) segment represents a promising alternative in the automotive fuel cell system market, with manufacturers exploring its potential for specific vehicle applications.

The technology’s key advantage lies in its ability to directly convert methanol fuel at the fuel cell anode, eliminating the need for complex fuel reforming processes. Recent technological advancements have focused on improving anode performance and developing highly efficient methanol oxidation catalysts to address previous performance limitations.

The segment has attracted significant attention from research institutions and manufacturers who are working on optimizing the technology for automotive applications. The Alkaline Fuel Cell (AFC) and Phosphoric Acid Fuel Cell (PAFC) segments, while smaller in market share, continue to play important roles in specific automotive applications.

AFCs are recognized for their high energy conversion efficiencies and environmentally friendly characteristics, though they face challenges related to ion conductivity and membrane stability. PAFCs offer advantages in terms of water management and impurity tolerance, making them suitable for certain specialized vehicle applications.

Both technologies are undergoing continuous development, with researchers working on addressing their respective limitations such as carbon dioxide sensitivity in AFCs and cost reduction in PAFCs.

Commercial vehicles dominate the automotive fuel cell system market, holding approximately 87% market share in 2024. This significant market position is driven by the increasing adoption of fuel cell technology in buses, trucks, and other heavy-duty vehicles due to their advantages in long-range operations and quick refueling capabilities.

Major developments in this segment include the deployment of fuel cell buses through programs like JIVE in Europe and similar initiatives in China and North America. The segment’s growth is further supported by stringent emission regulations worldwide pushing fleet operators toward zero-emission alternatives.

Companies like Hyundai, Toyota, and Daimler are actively expanding their fuel cell commercial vehicle portfolios, with particular focus on heavy-duty trucks and transit buses. The passenger car segment in the automotive fuel cell system market is experiencing robust growth, projected to expand at approximately 41% during 2024-2029.

This growth trajectory is supported by increasing investments in hydrogen infrastructure and growing consumer awareness about zero-emission vehicles. Automotive manufacturers are introducing new fuel cell passenger car models with improved range and efficiency, while also focusing on reducing production costs to make these vehicles more accessible to consumers. The segment is particularly gaining traction in regions with well-developed hydrogen refueling infrastructure, such as Japan, South Korea, and parts of Europe.

The passenger cars segment continues to dominate the automotive driveshaft market, commanding approximately 58% market share in 2024, driven by increasing global vehicle production and stringent regulations related to vehicular and passenger safety across major economies.

This segment’s leadership position is reinforced by the growing adoption of electric and hybrid vehicles in the passenger car category, which require specialized automotive drivetrain components to handle their unique powertrain configurations.

The segment is also experiencing the fastest growth trajectory, projected to expand at around 7% through 2025-2033, propelled by technological innovations in driveshaft design for electric vehicles and the rising demand for all-wheel-drive passenger vehicles.

The commercial vehicles segment represents a significant portion of the automotive driveshaft market, driven by the expanding e-commerce sector and increasing demand for logistics and transportation services globally.

This segment is characterized by the need for heavy-duty and highly durable driveshaft systems that can withstand intense usage patterns and heavy loads. The growth in this segment is being fueled by the increasing adoption of electric commercial vehicles, with companies like Tesla, BYD, Volvo, and Mercedes-Benz developing electric truck models that require specialized automotive axle shaft solutions. The segment is also benefiting from technological advancements in driveshaft materials and designs, specifically engineered to enhance the performance and reliability of commercial vehicles.

The hydrogen segment continues to dominate the automotive fuel cell system market, holding approximately 82% market share in 2024. This significant market position is driven by the increasing adoption of hydrogen fuel cell systems in commercial vehicles, particularly in buses and heavy-duty trucks.

Major automotive manufacturers are actively expanding their hydrogen fuel cell vehicle portfolios, with companies like Toyota and Hyundai leading the development of hydrogen-powered commercial vehicles. The segment’s growth is further supported by the ongoing development of hydrogen refueling infrastructure across major markets, particularly in Europe, North America, and Asia-Pacific regions.

The methanol segment is emerging as the fastest-growing segment in the automotive fuel cell system market, projected to grow at approximately 41% during the forecast period 2024-2029. This rapid growth is attributed to the increasing recognition of methanol as a viable alternative fuel source, particularly in regions where hydrogen infrastructure is still developing.

The segment is benefiting from technological advancements in direct methanol fuel cell (DMFC) systems, which are becoming more efficient and cost-effective. Several automotive manufacturers and technology companies are investing in research and development to enhance methanol fuel cell technology, focusing on improving power density and reducing system costs.

Asia-Pacific is the most significant shareholder in the global automotive fuel cell system market and is expected to grow at a CAGR of 33.15% during the forecast period. South Korea is a significant automotive market in the region.

Like other Asian nations, the country invests heavily in hydrogen technology, driving demand for automotive fuel cell systems. For example, Se’A Mechanics Co. Ltd. (Se’A Mechanics) announced in March 2021 that it would invest KRW 25 billion in constructing a new plant in Gumi, Gyeongsangbuk, and the investment will expire in 2027.

Europe has established itself as a key market for automotive fuel cell systems, supported by ambitious clean energy goals and strong governmental support. The region benefits from collaborative initiatives like the JIVE program, which promotes hydrogen fuel cell vehicle adoption.

Countries including Germany, the United Kingdom, France, Russia, and Spain are actively developing hydrogen infrastructure and implementing supportive policies. The commercial vehicle segment, particularly buses and heavy-duty trucks, has seen significant adoption of fuel cell technology across European nations.

North America is expected to grow at a CAGR of 52.56%, generating USD 14,645 million during the forecast period. The United States has one of the largest fleets of internal combustion engine vehicles, making it a top emitter. Due to strict emission regulations, technology manufacturers, and tax credits, the country’s fuel cell market is growing.

Leading automakers and OEMs in the U.S. are also expected to boost fuel-cell commercial vehicle adoption. For Instance, Hyundai plans to build a USD 6.4 billion factory by 2030 that can produce 500,000 fuel cell systems for commercial and passenger vehicles. Due to the widespread use of fuel-cell buses in public transportation, the automotive fuel-cell system market is expected to grow.

The automotive fuel cell system market is expected to grow CAGR of 40.73 % from 2025 to 2033.

The current automotive fuel cell system market size is USD 5.14 Billions in 2024.

The Asia Pacific currently holds the largest market share of automotive fuel cell system.

Top prominent players in Automotive Fuel Cell System Market are, BorgWarner Inc., Nuvera Fuel Cells LLC, Ballard Power Systems Inc., Cummins Inc., Nedstack Fuel Cell Technology BV, Oorja Corporation, Plug Power Inc., SFC Energy AG, Watt Fuel Cell Corporation, Doosan Fuel Cell Co. Ltd, etc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Automotive Fuel Cell Market, By Electrolyte Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Automotive Fuel Cell Market, By Vehicle Type

5.3 Automotive Fuel Cell Market, By Fuel Type

6.1 North America Automotive Fuel Cell Market , By Country

6.1.1 Automotive Fuel Cell Market, By Electrolyte Type

6.1.2 Automotive Fuel Cell Market, By Vehicle Type

6.1.3 Automotive Fuel Cell Market, By Fuel Type

6.2 U.S.

6.2.1 Automotive Fuel Cell Market, By Electrolyte Type

6.2.2 Automotive Fuel Cell Market, By Vehicle Type

6.2.3 Automotive Fuel Cell Market, By Fuel Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping