Automotive Ignition Coil Market

Automotive Ignition Coil Market Size, Share & Industry Analysis, By Type (Coil-on-plug, Distributor based, Distributor less), By Sales Channel (OEM and Aftermarket), and By Vehicle Type (Passenger Cars and Commercial Vehicles), Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

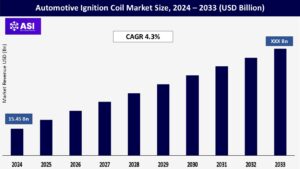

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 4.3%

Last Updated : February 5, 2026

The global ignition coil market size was estimated at USD 15.45 Billion in 2024 and is expected to expand at a CAGR of 4.3% from 2025 to 2033, driven by the surge in automotive production and sales across both developed and emerging economies.

As internal combustion engine (ICE) vehicles continue to dominate the automotive landscape, the need for efficient ignition systems remains paramount. Ignition coils, essential for converting low voltage from a vehicle’s battery into the high voltage necessary for engine operation, are integral to this process.

The growth trajectory is further supported by the rising adoption of advanced ignition technologies, such as coil-on-plug systems, which offer improved performance and fuel efficiency.

Technological advancements in automotive engineering have led to the development of high-performance engines with higher compression ratios and leaner fuel mixtures, requiring more efficient ignition systems.

According to industry reports, the global automotive industry continues to witness a shift toward electrification and the adoption of advanced engine technologies to meet stringent emissions regulations and fuel efficiency standards.

As a result, automakers are increasingly incorporating advanced ignition coil systems into their vehicles to enhance ignition timing precision, combustion stability, and overall engine performance.

The growing trend toward turbocharged engines and downsized powertrains further underscores the importance of reliable ignition coil systems. These engines require precise control over ignition timing and spark intensity to maximize power output while minimizing fuel consumption and emissions.

Also, the increasing popularity of performance-oriented vehicles, such as sports cars and high-performance sedans, contributes to the demand for high-quality ignition coil systems. These vehicles rely on advanced ignition technology to deliver optimal engine performance and responsiveness, driving the market for premium ignition coil products.

Overall, the increasing demand for vehicles with advanced ignition systems, driven by evolving regulatory requirements, engine technology advancements, and consumer preferences for improved performance and efficiency, serves as a major driving force for the automotive ignition coil market in 2024 and beyond.

Consumers worldwide prefer electric vehicles over ICE vehicles due to less maintenance, rapid acceleration, and low energy costs. The governments of respective countries are also offering customers a chunk of benefits & implementing regulations related to fuel-efficient vehicles.

The predicted growth of electric vehicles in the coming years will hinder the growth of these coils as these types of coils are not used in EV for operations. In addition, the ignition coil maintenance & repairing cost is slightly comparatively higher.

Also, their failure chances are higher as it is mounted on the hottest part & prone to vibration. Thus, these factors are expected to significantly impact the automotive spark coil market’s growth.

The growing consumer and industry shift toward fully electric vehicles, which do not require ignition coils, poses a significant challenge for the ignition coil market in the long term.

As governments worldwide push for zero-emission vehicle targets and offer incentives for electric vehicle (EV) adoption, the demand for internal combustion engine components could gradually decline. This transition necessitates that ignition coil manufacturers diversify their product offerings or pivot toward technologies supporting electric powertrains.

For instance, in March 2021, Diamond Electric Mfg. Co. Ltd expanded its U.S. operations to support traditional ignition coil production, while also strategizing for the upcoming EV shift. Adapting to the EV revolution by investing in new technologies and expanding market focus will be critical for the future resilience of ignition coil companies.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Coil-on-Plug Distributor-based Distributor less |

| By Vehicle Type |

Passenger Cars Commercial Vehicles Nickel-cadmium |

| By Distribution Type |

OEM Aftermarket |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Coil-on-plug systems accounted for 51.33% of 2024 revenue, and their 6.32% CAGR positions them as the clear growth engine for the automotive ignition coil market. The design removes high-voltage leads, reduces electromagnetic loss, and supports advanced knock-control strategies demanded by turbocharged engines. Block coils and rail assemblies stay competitive in cost-sensitive models, especially in entry-level segments across emerging economies. Also, with fewer connections and eliminating the distributor rotor to cap air gap, it can be used in sync with injector control to have the ECU perform a misfire diagnosis.

The distributor ignition coils segment led the market and accounted for the largest revenue share of 34.7% in 2024. They are widely used in older vehicle models and various internal combustion engine (ICE) applications. These coils are essential in traditional ignition systems, where they work in conjunction with the distributor to direct the spark to the appropriate cylinder. Despite the rise of newer ignition technologies like coil-on-plug (COP) systems, distributor ignition coils are still prevalent in many vehicles, especially in markets with a large number of older vehicles. The affordability and ease of replacement of distributor ignition coils also contribute to their high demand in regions where cost-effectiveness is a priority.

A discrete coil supplies voltage to each spark plug in a distributor-less ignition system. The computer in your car can then calculate the exact time to ignite each cylinder. This approach gives you more control and eliminates any moving mechanical parts. However, this segment will not grow as it is more difficult and expensive to examine and repair than a traditional system and still requires high voltage wires from the coils to the spark plugs.

The passenger car segment currently holds the biggest share of the global market, which is expected to continue. The advantage can be attributed to several factors, including the growing urban population and the requirement for commuting. The demand is expanding as people become more concerned about rising pollution levels and their low running costs. The increased demand for used cars and the average age of passenger cars globally are expected to drive the demand for aftermarket ignition coils, as people tend to spend more on repairing and replacing parts to keep their vehicles in good condition.

The commercial vehicle sector is expanding in terms of product offerings and sales.On the other hand, commercial EVs are now a part of the transportation business in China and the United States. During the projected period, they are anticipated to replace conventional trucks. Several medium and heavy commercial vehicles manufacturers are working on electrification and have begun producing automotive batteries with increased power capacity.

The global automotive ignition coil market is segmented into OEM and aftermarket. The aftermarket segment accounted for the largest market share and is estimated to grow at a CAGR of 4.8% during the forecast period.

A large number of gasoline-powered vehicles in use worldwide is anticipated to drive the demand for aftermarket ignition coils. In recent years, the demand for gasoline-powered vehicles has significantly increased.

For instance, since 2016, all the new cars sold in China (excluding electric vehicles) have been powered by gasoline. Similarly, 52.1% of all the new cars sold in the first half of 2020 in the European Union were powered by gasoline.

The share of gasoline-powered passenger cars has been increasing consistently over the last five years. The ignition coils in these recently-sold gasoline-powered passenger cars are likely to be subjected to replacement in the coming years, which will drive the aftermarket segment’s growth during the forecast period.

OEM contracts delivered 75.12% of 2024 sales, but aftermarket revenue is rising at 7.18% CAGR, faster than any other channel in the automotive ignition coil market. Independent garages rely on ready availability and multi-pack options, attributes embraced by Standard Motor Products and NGK.

The aging vehicle profile in North America and Western Europe underpins parts replacement. Meanwhile, emerging markets such as India see aftermarket coils used in second-hand imports that lack dealer support. As BEVs shrink OEM coil demand, aftermarket activity will become the stabilizing pillar for the automotive ignition coil industry.

Asia Pacific dominated the market and accounted for the largest revenue share of 46.4% in 2024. This is due to rapid industrialization, urbanization, and a booming automotive sector, especially in countries like India, Japan, and South Korea. Rising disposable incomes, expanding middle-class populations, and strong domestic vehicle manufacturing contribute to the growing demand.

Government initiatives to promote cleaner emissions and fuel-efficient technologies are also pushing manufacturers to adopt advanced ignition systems. The region’s focus on hybrid and compact car segments also boosts the adoption of newer ignition technologies.

In Europe, stringent emission regulations and strong environmental awareness are key factors boosting the demand for advanced ignition systems. The region’s automakers focus on engine downsizing and turbocharging, which require high-efficiency ignition coils to ensure performance and compliance.

The presence of a large fleet of high-end vehicles and a mature aftermarket also supports consistent demand for ignition coil replacements. In addition, incentives for eco-friendly vehicles indirectly drive ignition technology upgrades.

In North America, rising consumer demand for pickup trucks, SUVs, and high-performance vehicles supports growth in the ignition coil market. The presence of a large vehicle parc and a strong culture of vehicle maintenance and repair sustains demand in the aftermarket.

Furthermore, increasing environmental regulations in the U.S. and Canada encourage automakers to upgrade ignition systems for better fuel economy and reduced emissions. The adoption of advanced diagnostic tools also boosts timely ignition component replacement.

The U.S. market for ignition coils is experiencing increased ignition coil demand due to aging vehicle fleets, widespread ownership, and a high preference for large-engine vehicles requiring more robust ignition systems.

Growth in the electric and hybrid vehicle segment also contributes, as some hybrid systems still require specialized ignition coils for internal combustion components. Additionally, the strong presence of DIY vehicle maintenance culture fuels the replacement parts market, further supporting growth.

In the Middle East & Africa, demand for ignition coils is rising due to increasing vehicle imports, especially in urban centers with growing middle-class populations. Economic diversification and infrastructure development are also spurring vehicle sales.

The harsh climatic conditions in many parts of the region necessitate robust and heat-resistant ignition systems, which further supports market growth. Moreover, the growth of the aftermarket and parallel import channels makes replacement ignition coils more accessible to consumers.

The market is expected to grow CAGR of 4.3 % from 2025 to 2033.

The current market size is USD 15.45 Billions in 2024.

Asia Pacific currently holds the largest market shares.

Companies such as MARSHALL ELECTRIC, CORP (U.S.), BorgWarner Inc (U.S.), Continental AG (Germany), DENSO CORPORATION (Japan), and Hitachi Astemo Americas, Inc. (U.S.) are the major companies in the ignition coil market.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Automotive Ignition Coil Market, By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Automotive Ignition Coil Market, By Vehicle Type

5.3 Automotive Ignition Coil Market, By Distribution Type

6.1 North America Automotive Ignition Coil Market , By Country

6.1.1 Automotive Ignition Coil Market, By Type

6.1.2 Automotive Ignition Coil Market, By Vehicle Type

6.1.3 Automotive Ignition Coil Market, By Distribution Type

6.2 U.S.

6.2.1 Automotive Ignition Coil Market, By Type

6.2.2 Automotive Ignition Coil Market, By Vehicle Type

6.2.3 Automotive Ignition Coil Market, By Distribution Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping