Automotive Lighting Market

Automotive Lighting Market Share & Trends Analysis Report by Vehicle Type (Passenger Vehicles, Commercial Vehicles), by Technology (LED, Halogen, Xenon), by Position (Rear Lighting, Front Lighting, Side Lighting, Interior Lighting) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2024–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

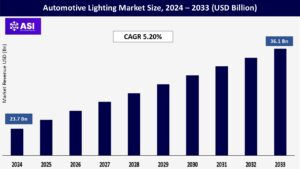

CAGR: 5.20%

Last Updated : June 3, 2026

The global Automotive Lighting Market size is projected to reach USD 23.7 billion in 2024 and is expected to grow to USD 36.1 billion by 2033, reflecting a compound annual growth rate (CAGR) of 5.20%.

Automotive lighting plays a crucial role in vehicle safety and aesthetics, with applications spanning passenger and commercial vehicles. The increasing demand for advanced lighting technologies, such as LED and Xenon, along with stringent safety regulations, are key drivers of market growth.

As the automotive industry shifts towards electric and autonomous vehicles, the need for innovative lighting solutions is more critical than ever.

Because they provide higher energy efficiency, long-term lifespans, and good glowing. The automotive industry is observe a important change to advanced lighting technologies, primarily manage by the need for improve safety and energy efficiency.

Collaboration between producers and technology suppliers are increasing the development and adoption of new lighting technologies. LED lighting, for instance, offers superior brightness, longer lifespan, and lower energy consumption compared to traditional halogen lights.

According to industry reports, LED lights can consume up to 75% less energy, making them a preferred choice for manufacturers aiming to meet fuel efficiency standards.

The automotive interior ambient lighting system market is projected to grow significantly, driven by increasing demand for improve in quality, vehicle comfort, premium vehicles, and technological advancements in LED and OLED lighting.

It is more beneficial and also economical services for the consumers. In nature, the increasing demand for advanced lighting technologies throwback a combination of technological developments , consumer partialiality, regulatory pressures, and growing discuss about energy regulations and Supportable.

For Example – Governments apply rules and giving motivation to encourage the assumption of energy-efficient lighting, such as LED lighting, driving market growth.

Regulatory bodies worldwide are applying demanding safety standards that required to improved clarity and visibility for vehicles. This regulatory pressure is pushing manufacturers to innovate and adopt advanced lighting solutions, thereby driving market growth.

Governments worldwide are applying strict laws requiring obstruction lighting for various structures, including buildings, towers, wind turbines, and communication masts, driving market growth. By setting standards for safety, quality, and ethical conduct, regulations can motivate businesses to inventions of new technologies and processes that encounter these requirements.

Strict rules and laws can give assurity of product safety and quality, improve consumer confidence and driving demand. A clear and compatible regulatory environment can increase investment, both domestic and foreign, by reducing variability and risk. For example- the European Union has introduced regulations requiring advanced lighting systems in new vehicle models.

High production costs associated with advanced lighting technologies, particularly LED and Xenon, pose a significant challenge for manufacturers. The initial investment required for R&D and production facilities can be substantial, limiting the ability of smaller players to compete.

Additionally, the complexity of combine advanced lighting systems into existing vehicle designs can inhibit adoption. Managing supply chains can be challenging, particularly when it comes to sourcing high-quality materials and components.

In horticulture lighting, different lot have specific lighting requirements, making it challenging to design lighting systems that can harbour a wide range of batch. Every country’s having different rules and policies for the business which are multiplex or taking more time.

There culture and languages are different so we can’t adapt or adjust with them. Languege barrier’s can affect on businesses and many challenges might be facing in further activities related to the businesses.

Insufficient infrastructure and equipments can affect the business expansions like transportations etc. For Example – Financial restrictions and regulatory problems can limit expansions of business.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Vehicle Type |

Passenger Vehicles Commercial Vehicles |

| By Technology |

LED Halogen Xenon |

| By Position |

Rear Lighting Front Lighting Side Lighting Interior Lighting |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Passenger cars held the most portion of the automotive lighting industry, accounting for over 54.7% of the total market in 2024. The enormous volume of passenger cars produced worldwide and the growing consumer preference for high-end lighting systems like LED, matrix LED, and laser headlights are the reasons for this dominance.

In order to improve user experience, safety, and aesthetics, automakers are increasingly incorporating ambient interior lighting, adaptive front illumination, and daytime running lights (DRLs) into mid-range and high-end passenger vehicles.

With the help of smart lighting integration, increasing vehicle electrification, and increased consumer awareness of road safety, particularly in metropolitan areas, the market is predicted to expand gradually.

Commercial Vehicles, including light and heavy-duty trucks and buses, held an estimated xx% market share in 2024. Based on vehicle type, the market is segmented into light commercial vehicle, heavy vehicle, and buses.

The light commercial vehicle segment accounts for a significant share in the global market, owing to its highest usage in logistics operation in a smaller range. It is expected to continue to account for most of the global market.

The heavy vehicle segment is also expected to develop exponentially over the forecast period. It is expected to exhibit the highest CAGR (11.8%) during the forecast period. The bus market is also expected to grow exponentially during the forecast period.

LED: The global LED lighting is covered 46.4 % of the automotive lighting market. Over the forecast period, the LED segment will dominate the market. The low energy consumption and excellent power output of LED as compared to halogen are likely to help the segment grow.

Leading manufacturers are focusing on developing advanced LED lights that will eventually replace halogen bulbs. For instance, in September 2024, Forvia Hella, a global automotive supplier, launched series production of an RGB LED rear combination lamp with full-color light animations in China for the first time.

Halogen: Global Halogen Lamp market is held the most of the portion of the automotive lighting industry, accounting for 35% of the total market in 2024. This helps to understand the fastest-growing segments, such as industrial robots, electric motors, material handling systems, or construction equipment, and others.

The halogen segment is anticipated to hold the second-largest position in the market over the forecast period. It has witnessed steady growth over the forecast period. Halogen lights are most commonly used in heavy vehicles due to their unique characteristics and low heat compared to LED. Also, halogen lights provide better visibility, improving drivers’ safety and comfort.

Xenon: Xenon is held the less portion of the automotive lighting global market industry, only 15% .In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand.

Rear Lighting: Rear lighting market is covered more than 33.5% of the global market in 2024. Automotive LED tail lights are main leading segment of rear lighting. Necessary for safety, with a high demand. Provide clearity and signaling to other road users. Indicate when the vehicle is stoping.

Light up the area behind the vehicle when reversing. The automotive rear lights market is influenced by several key driving factors.

First, technological advancements in lighting systems such as LED and OLED technologies have revolutionized the market. The Global Automotive Rear Lights Market is Segmented on the basis of Type of Product, Functionality, Sales Channel, and Geography.

Front Lighting: Front lighting is held the most of the portion of the global market is 60% in 2024. Head lamps is main leading segment and The largest segment, driven by safety regulations and technological advancements. The Indian automotive adaptive front lighting market is experiencing robust growth, projected to reach XXX million units by 2033.

Provide forward visibility, available in various types (halogen, LED, HID) improve visibility during the day, often using LED technology increase visibility in low-visibility conditions, such as fog or heavy raining. Premium vehicles will likely lead the market segment in terms of adoption of adaptive front lighting.

Side Lighting: Side lighting is covered less market of the automotive lighting market it is only 7% in 2024. Indore lighting segment is main leading segment for side lighting Emerging segment with increasing adoption in luxury vehicles.

Amber or red lights that indicate the vehicle’s presence and width Indicate the driver’s intention to turn or change lanes Side lighting primarily includes side marker lights (amber colored for the front and red for the rear) and turn signal lights. LED technology is increasingly being used for side lighting due to its energy efficiency and durability.

Interior Lighting: The market covered by the interior lighting as per 2024 is only 11% of the global market. Commercial lighting is main leading segment of interior lighting Growing due to consumer preferences for improves cabin aesthetics.

Interior Lighting Market size is expected to reach $122.59 billion by 2033, rising at a market growth of 5.3% CAGR during the forecast period.

Soft, precise lighting that improves the interior conditions and designs, Focused lights that provide illumination for passengers, Soft lights that illuminate the footwell area. Rising trends in luxury interiors and artistic lighting designs are key drivers for this segment.

North America accounted for a strong 32.1% of the worldwide automotive lighting market, fueled by rising vehicle production, the expanding use of advanced driver-assistance systems (ADAS), and consumer desire for improved safety and visibility features.

The U.S. accounts for the majority of this regional share, driven by considerable R&D investments in adaptive lighting systems and government legislation mandating daytime running lights (DRLs) and automatic headlamp controls.

LED and matrix LED technologies are being used into new models by automakers more frequently, especially in luxury and electrified cars. The region’s market expansion is being driven by the need for sophisticated and energy-efficient lighting solutions in both passenger and commercial vehicles.

Europe’s expertise in automotive innovation and legislative drive for energy-efficient lighting solutions helped it become the second-largest market. In 2024, the region was projected to have 28.7% of the global market. With a combined market share of about xx%, nations like Germany, France, and the UK are leading the way.

Due to its robust automotive production base and the extensive use of matrix LED and laser headlamp technology in high-end automobile segments, Germany in particular plays a crucial role. The increasing need for energy-efficient lighting is also a result of EU regulations on emissions and daytime running lights (DRLs).

APAC is expected to develop at the fastest rate, with a compound annual growth rate (CAGR) of 11.8% between 2024 and 2032. Rapid urbanization in nations like China, India, Japan, and South Korea, as well as increased automotive production and disposable income, are driving the growth.

Because of its large automobile population and government subsidies for electric vehicles that need high-performance lighting systems, China dominates the regional industry. Rising consumer demand for mid-range automobiles’ safety and aesthetics, along with increased domestic production under the Make in India campaign, are driving India’s strong growth.

MEA is expected to grow steadily, particularly in the construction of infrastructure and the sale of luxury automobiles. The desire for luxury and high-performance cars, which frequently have sophisticated lighting systems, is growing in nations like the United Arab Emirates and Saudi Arabia.

Additionally, OEMs are being encouraged to localize production of lighting components via automotive manufacturing programs in North African and South African nations. The region’s severe weather also makes high-intensity, long-lasting lighting solutions necessary, which increases market potential.

Latin America is progressively increasing its market share in the automotive lighting sector, with Brazil and Mexico leading the way with a significant combined market share. The adoption of LED and halogen-based lighting systems is aided by Brazil’s robust automobile industry, government incentives for domestic production, and improvements to safety standards.

Energy-efficient and economical lighting modules are becoming more and more in demand in Mexico, a major production location for North American OEMs. As car safety and pollution requirements continue to conform to international standards, the region is anticipated to increase at a moderate rate.

The market is expected to reach USD 36.1 billion by 2033.

The main technologies include LED, Halogen, and Xenon.

The Asia-Pacific region is expected to have the highest CAGR due to rapid urbanization.

Key drivers include the demand for advanced lighting technologies and regulatory standards for vehicle safety.

High production costs and integration complexities are significant challenges.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Automotive Lighting Market, By Vehicle Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Automotive Lighting Market, By Technology

5.3 Automotive Lighting Market, By Position

6.1 North America Automotive Lighting Market , By Country

6.1.1 Automotive Lighting Market, By Vehicle Type

6.1.2 Automotive Lighting Market, By Technology

6.1.3 Automotive Lighting Market, By Position

6.2 U.S.

6.2.1 Automotive Lighting Market, By Vehicle Type

6.2.2 Automotive Lighting Market, By Technology

6.2.3 Automotive Lighting Market, By Position

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping