Automotive Wiring Harness Market

Automotive Wiring Harness Market By Application (Chassis harness, Sensors), Material Type (Copper, Aluminium), Transmission Type (Terminals, Electrical Wiring) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

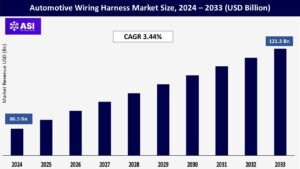

CAGR: 3.44%

Last Updated : February 5, 2026

The global automotive wiring harness market size was valued at USD 86.5 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 121.3 Billion by 2033, exhibiting a CAGR of 3.44% during 2025-2033.

Asia Pacific currently dominates the market, holding a significant market share of over 46.7% in 2024. At present, Asia Pacific holds the largest automotive wiring harness market share, driven by cost-effective manufacturing and increasing adoption of electric vehicles (EVs).

Specialty cables are in high demand due to their lighter weight, lower cost, and smaller bundle diameter. There will be plenty of demand for cameras, displays, and other infotainment applications, resulting in the development of new techniques to combine video and camera signals into a single specialty cable, decreasing the weight and expense of wiring harnesses even further.

For lightweight and high-speed harnesses, original equipment manufacturers chose aluminum and optical fiber. Thus, this factor is driving the growth of the global automotive wiring harness market.

The rising vehicle production and sales majorly drive the global market. As vehicle manufacturing scales up, so does the demand for wiring harnesses. Emerging markets are witnessing significant growth in vehicle production, which is driving the demand for these components.

Additionally, the growing demand for electric vehicles (EVs) is also contributing to the growth of the automotive wiring harness market, as these vehicles require more complex wiring systems.

Moreover, modern vehicles are equipped with advanced features, such as advanced driver-assistance systems (ADAS), infotainment systems, and electronic safety systems, all of which require complex wiring systems.

Therefore, the increasing integration of these electronic systems and features into vehicles is directly driving the demand for more sophisticated and durable wiring harnesses.

Copper prices have been volatile, affecting demand for optical fiber cables in the global market. Original equipment manufacturers emphasize the use of optical fibers that are more durable than copper/aluminum and can endure hard environments and weather.

The relatively higher expense of optical fiber cables, on the other hand, is likely to limit its adoption in the global market. Several restraining factors will inhibit the rise of the automotive wire harness market internationally.

The production deficits and the quality of raw materials used to manufacture these automotive wire components. Poor maintenance or inappropriate configuration can cause problems with machine-made wire systems.

Common errors involve bad soldering or crimping, weak connections, and incorrect wiring arrangements. Also, using the primitive copper alloy instead of OEM-grade copper for the crucial components like the terminals will restrict the growth of the market.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Application Type |

Chassis harness Sensor |

| By Material Type |

Aluminium Copper |

| By Transmission |

Terminals Electrical Wiring |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Chassis harness segment led the market with the largest revenue share of 34.64% in 2024. The regulatory mandates for vehicle safety, consumer demand for enhanced driving dynamics and safety features, and technological advancements in chassis control systems are driving the demand for the chassis wiring segment.

Wiring harnesses for chassis applications are evolving to support the increasing electrification and connectivity of chassis components, as well as the integration of advanced safety and driver assistance systems.

The sensors harness segment is expected to exhibit the fastest CAGR from 2024 to 2030. Including numerous sensors for systems such as illumination, battery system, speed systems, infotainment systems, and ADAS.

Moreover, the development and integration of advanced sensors are expected to play a crucial role in the evolution of automotive technology, especially as vehicles increasingly feature a variety of safety solutions.

For instance, in May 2022, Continental AG, an automotive manufacturer, announced the expansion of its extensive sensor portfolio by introducing two new sensors for electric vehicles, namely Battery Impact Detection (BID) and Current Sensor Module (CSM).

Copper leads the market with around 86.2% of the market share in 2024. Copper’s dominance is due to its superior electrical conductivity, thermal performance, and reliability. Moreover, its ability to efficiently transmit electrical signals with minimal resistance makes it indispensable in powering critical vehicle systems, including engine controls, infotainment, and safety features.

Besides this, the heightened reliance of the automotive industry on copper due to its durability and recyclability, aligning with sustainability goals and stringent regulatory standards, is fostering the market growth.

Aluminum’s forecast CAGR is in double digits, easily outpacing the broader Automotive Wiring Harness industry trajectory. Advances in anti-corrosion terminals and friction-weld splice techniques have removed earlier reliability concerns.

Because aluminum is price-stable relative to copper, finance teams increasingly model its use as a hedge. The shift indicates that material science choices now intersect directly with treasury risk management strategies inside large suppliers.

Electrical wiring leads the market with around 81.5% of the market share in 2024. It acts as the backbone for power and signal transmission across divergent automotive systems, such as lighting, infotainment, and advanced driver-assistance systems (ADAS).

The market growth is also being catalyzed by an increasing demand for electric vehicles (EVs) and hybrid vehicles that heavily rely on intricate electrical wiring to manage high-voltage power and connectivity requirements.

the terminal segment is expected to grow at the fastest CAGR in the global automotive wiring harness market during the forecast period. The growing use of innovative automotive technologies such as autonomous and integrated cars and the subsequent investments in research and development efforts to improve the efficiency, reliability, and performance of automotive wires are the factors that will contribute to the segment’s growth.

Asia Pacific dominated the automotive wiring harness market with a revenue share of 45.8% in 2024. The dynamic nature of the automotive industry in the Asia Pacific is opening ample opportunities for the manufacturers of automotive wiring harnesses to capitalize on the advances in technology and shifting consumer preferences. As such, market players are focusing on innovation and product differentiation to cater to the evolving market demands effectively.

The automotive wiring harness market in Europe is anticipated to reach USD 13.00 billion in 2024. The region is expected to see a rise in the demand for high-voltage harness wires as the region witnessed a consistent rise in electric vehicle sales.

The sales of EV vehicles are further propelling market growth, owing to subsidies provided by the EU and respective governments of European countries.

North America is expected to register at a considerable CAGR from 2025 to 2033. As the automotive industry continues to evolve, the growing demand for advanced wiring harnesses is playing a crucial role in driving the market growth.

The push toward autonomous vehicles and the electrification of mobility are presenting a significant opportunity for innovation and investment in automotive wiring harness solutions.

The automotive wiring harness market in the Middle East and Africa (MEA) region is anticipated to reach USD 2.86 billion by 2033. The aggressive adoption of automation and other advanced technologies in manufacturing, in line with the broader trend of Industry 4.0, is driving the market growth of the Middle East and Africa.

The integration of smart technologies in manufacturing automotive wiring harnesses can help create more agile and responsive supply chains.

The automotive wiring harness market is expected to grow CAGR of 3.44% from 2025 to 2033.

The current automotive wiring harness market size is USD 86.5 billion in 2024.

The Asia-Pacific currently holds the largest market share of automotive wiring harness.

Electrical wiring is the leading segment by transmission type, driven by the rapid shift towards electric vehicles (EVs) and hybrid electric vehicles (HEVs) that rely on electrical power for propulsion and energy management.

Some of the major players in the global Automotive Wiring Harness market include Furukawa Electric Co. Ltd., Lear Corporation, Leoni AG, Nexans Autoelectric GmbH, PKC Group, B.V., Sumitomo Electric Industries Ltd., THB Group (AmWINS Group, Inc), YAZAKI Corporation, YURA Corporation, etc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Automotive Wiring Harness Market, By Application Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Automotive Wiring Harness Market, By Material Type

5.3 Automotive Wiring Harness Market, By Transmission Type

6.1 North America Automotive Wiring Harness Market , By Country

6.1.1 Automotive Wiring Harness Market, By Application Type

6.1.2 Automotive Wiring Harness Market, By Material Type

6.1.3 Automotive Wiring Harness Market, By Transmission Type

6.2 U.S.

6.2.1 Automotive Wiring Harness Market, By Application Type

6.2.2 Automotive Wiring Harness Market, By Material Type

6.2.3 Automotive Wiring Harness Market, By Transmission Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping