Bio-Lubricants Market

Bio-Lubricants Market & Trends Analysis Report, By Base Oil Type (Vegetable Oil, Animal Fat, Other: Polyalkylene Glycols and Synthetic Esters), By Application (Industrial, Automotive, Marine, Others), By End Use (OEMs, Aftermarket, Others)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

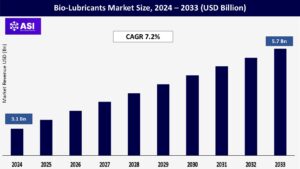

CAGR: 7.2%

Last Updated : March 27, 2026

The global Bio-Lubricants Market size was valued at approximately USD 3.1 billion in 2024 and is projected to reach USD 5.7 billion by 2033, growing at a CAGR of 7.2% during the forecast period (2025–2033).

Bio-lubricants, also known as biodegradable lubricants, are derived from renewable sources like vegetable oils and animal fats. They offer advantages such as reduced environmental impact, superior lubricity, lower toxicity, and enhanced biodegradability compared to conventional petroleum-based lubricants.

Market growth is primarily driven by increasing environmental regulations, rising awareness of sustainable products, and advancements in bio-based chemistry. However, limited oxidative stability and high production costs may hamper market expansion.

The market for bio-lubricants is being driven by the global movement toward decarbonization and sustainable industrial practices. To reduce pollution from petroleum-based lubricants, regulatory agencies like the European Chemicals Agency (ECHA), the U.S. Environmental Protection Agency (EPA), and the EU’s Registration, Evaluation, Authorization and Restriction of Chemicals (REACH) are implementing stringent rules.

These regulations are particularly strict in environmentally delicate industries where lubricant spills can directly harm the environment, such as forestry, agriculture, and marine transportation.

Consequently, businesses are turning more and more to low-toxicity, biodegradable lubricants that meet environmental safety regulations and bio-based content standards. Furthermore, global certifications like EU Ecolabel, VGP compliance, and OECD 301 biodegradability are encouraging manufacturers to develop and adopt

As manufacturers place a higher priority on eco-friendly operations, sustainable maintenance methods, and low-carbon solutions, bio-lubricants are becoming more and more popular in both automotive and industrial applications.

Bio-lubricants are utilized in engine oils, transmission fluids, and greases in the automobile industry, especially in electric and hybrid cars where environmental friendliness and performance efficiency are important selling features.

In the industrial sector, they are being used in gear oils, hydraulic systems, and metalworking fluids, particularly in machinery used in open spaces or for food-grade purposes.

In addition to pushing enterprises to transition to bio-lubricants, government procurement requirements and green certification programs for industrial equipment are also significantly increasing market demand.

The comparatively high cost of production of bio-lubricants in comparison to traditional mineral-based lubricants is one of the main obstacles preventing their widespread use.

To improve their thermal stability, oxidation resistance, and shelf life, bio-lubricants made from vegetable oils frequently need to undergo intensive chemical modification procedures like esterification, hydrogenation, or transesterification.

Higher manufacturing costs result from these extra processing steps’ high capital requirements, specialized catalysts, and energy-intensive procedures.

Pricing systems are further complicated by the price volatility of feedstocks like rapeseed, soybean, and palm oil, which is influenced by weather, agricultural production, and the world’s food demand. Because of this, end-user companies can be hesitant to abandon established, less expensive petroleum-based alternatives, particularly in areas where costs are high.

Bio-lubricants frequently have technical performance constraints despite their environmental advantages, especially in high-temperature, high-pressure, or high-speed applications. Conventional synthetic lubricants generally perform better than bio-based alternatives in such challenging situations in terms of longer drain intervals, resistance to temperature deterioration, and oxidation stability.

The use of bio-lubricants is restricted by this performance gap in industries where mechanical stress resistance and long service life are essential, such as heavy-duty automotive, high-performance industrial machinery, and aviation.

Despite continuous research into better additive formulations and synthetic esters, the existing constraints continue to impede market penetration in these demanding end-use contexts.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Base Oil Type |

Vegetable Oil Animal Fat Other: Polyalkylene Glycols and Synthetic Esters |

| By Application |

Industrial Automotive Marine Others |

| By End-Use |

OEMs Aftermarket Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Bio-Lubricants Market is segmented by Base Oil Type (Vegetable Oil, Animal Fat, Other: Polyalkylene Glycols and Synthetic Esters), By Application (Industrial, Automotive, Marine, Others), By End Use (OEMs, Aftermarket, Others).

Each factor plays a crucial role in enhancing patient safety, increasing the adoption of self-administered anticoagulant therapies, and supporting the development of more convenient, prefilled drug delivery systems that streamline treatment in the management of thromboembolic and cardiovascular conditions.

Vegetable Oil (62.4%) by Base Oil Type

dominates because it is affordable, readily available, and biodegradable. Canola, soybean, and sunflower oils are frequently utilized and are widely employed in chainsaw and hydraulic systems.

Animal Fat (19.3%)

provides excellent lubrication but has drawbacks because of supply issues and odor. Use is restricted to specialized applications, particularly in low-temperature gear systems or military settings.

Other: Polyalkylene Glycols and Synthetic Esters (18.3%)

Improve thermal performance and oxidative stability. increasingly utilized in industries with high demand, such as aerospace and marine lubricants.

Industrial (39.8%)

Includes hydraulics, compressors, and gear oils. Industrial machinery is the largest consumer due to heavy-duty, continuous operations requiring environmentally safe lubricants.

Automotive (28.6%)

Engine oils, transmission fluids, and greases for cars, commercial vehicles, and off-highway applications. Electric vehicle growth is also driving demand for thermally stable green lubricants.

Marine (17.5%)

Key application for biodegradable oils due to regulations on marine pollution (e.g., VGP in the U.S.). Used in stern tubes, deck machinery, and wire rope lubrication.

Others (14.1%)

Covers chainsaws, railroads, agriculture, and forestry. Forestry and farming equipment heavily favor bio-lubricants for their reduced impact on soil and water.

OEMs (Original Equipment Manufacturers) – 48.1%

Increasing number of machinery manufacturers are integrating factory-filled bio-lubricants to meet compliance and gain competitive sustainability credentials.

Aftermarket – 45.7%

Large demand from equipment replacement and maintenance. Rising consumer awareness and corporate sustainability goals are accelerating aftermarket sales.

Others – 6.2%

Includes government bodies, military procurement, and pilot programs focused on environmental R&D.

Due to its fast industrialization, burgeoning construction and automotive sectors, and mounting demand for environmentally friendly production methods, Asia-Pacific is the region with the fastest rate of growth.

With the growing need for bio-lubricants in industrial machinery, urban infrastructure, and automobile assembly, nations like China, India, Japan, and South Korea are major providers. Bio-lubricants are being more and more integrated into OEM systems, particularly in industries where environmental compliance and low toxicity are crucial.

Favorable conditions for market expansion are being created by government initiatives in China’s green economy transformation and India’s “Make in India” and “Green India” programs.

North America has a sizable portion, driven by a varied industrial base and rising environmental compliance in all industries. Due to EPA regulations, the USDA BioPreferred Program, and Department of Defense (DoD) green procurement initiatives, the demand for bio-lubricants is rising, especially in the United States, from the construction, transportation, maritime, and agricultural sectors.

The area is maintaining steady market growth thanks to the existence of significant industry players, developments in synthetic ester formulations, and growing awareness among OEMs and end users.

Due to a modern legislative framework, strict sustainability regulations, and extensive corporate ESG commitments, Europe continues to be the largest and most developed market for bio-lubricants.

The environment is now more favorable for ecologically friendly lubricants, especially in industrial, forestry, and marine applications, thanks to regulations like REACH, the EU Ecolabel, and the Vessel General Permit (VGP).

With high demand from industries like wind energy, rail, automobile manufacturing, and ecologically sensitive industrial processes, nations like Germany, France, Sweden, and Finland are early adopters. Growth in the region is further supported by government-backed R&D funding and incentives for the adoption of green technologies.

Although the Latin American market is still in its infancy, bio-lubricants are becoming more and more popular in nations like Brazil and Mexico, especially in the mining, transportation, and agricultural sectors.

Brazil is promoting the usage of biodegradable products due to its extensive soybean and sugarcane farming industries as well as growing environmental consciousness. Growth is anticipated to be accelerated in the upcoming years by foreign investment in sustainable practices and public-private partnerships.

Although the market for bio-lubricants is currently smaller in the Middle East and Africa, interest is steadily growing as a result of massive construction projects, the growth of logistics infrastructure, and a growing emphasis on sustainable urban development, especially in the Gulf region.

Environmentally friendly lubricants are finding new applications in construction equipment and marine transportation thanks to initiatives like Saudi Arabia’s NEOM smart city, the United Arab Emirates’ green infrastructure projects, and Africa’s renewable energy initiatives.

The market size of Bio-Lubricants market is USD 3.1 billion.

The projected CAGR of Bio-Lubricants market is Approximately 7.2%

Vegetable oil-based lubricants, due to cost-effectiveness and renewability.

Asia-Pacific, led by industrialization and sustainability reforms.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Bio-Lubricants Market, By Base Oil Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Bio-Lubricants Market, By Application

5.3 Bio-Lubricants Market, By End-Use

6.1 North America Bio-Lubricants Market , By Country

6.1.1 Bio-Lubricants Market, By Base Oil Type

6.1.2 Bio-Lubricants Market, By Application

6.1.3 Bio-Lubricants Market, By End-Use

6.2 U.S.

6.2.1 Bio-Lubricants Market, By Base Oil Type

6.2.2 Bio-Lubricants Market, By Application

6.2.3 Bio-Lubricants Market, By End-Use

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping