Biosensors Market

Biosensors Market Share & Trends Analysis Report, By Product Type (Wearable Biosensors, Non-Wearable Biosensors (or Embedded Devices/Point-of-Care Devices)), By Technology Type (Electrochemical Biosensors, Optical Biosensors, Piezoelectric Biosensors, Thermal Biosensors, Nanomechanical Biosensors, Others)Consumables, Instruments, Services, Therapeutics (Small Molecule Drugs, Biologics, Cell & Gene Therapy), Diagnostics), By Application (Medical Diagnostics, Environmental Monitoring, Food and Beverages, Agriculture, Research & Development, Biodefense/Security), By End-User (Healthcare & Diagnostics, Food and Beverage Industry, Pharmaceutical & Biotechnology Companies, Academic and Research Institutes, Environmental Agencies, Security and Biodefense Agencies, Cosmetics Industry, Agriculture Sector)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

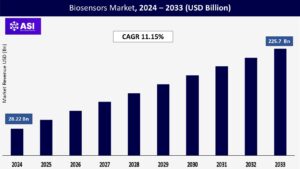

CAGR: 11.5%

Last Updated : November 25, 2025

The global for biosensors market size was valued at approximately USD 28.22 billion in 2024 and is projected to reach USD 225.7 billion by 2033, demonstrating a compound annual growth rate (CAGR) of 11.15% during the forecast period of 2025–2033.

The biosensors market is expected to witness remarkable growth from 2025 to 2033, fueled by a combination of technological innovation and growing healthcare needs. As more people around the world face chronic conditions like diabetes and heart disease, there’s an increasing demand for quick, accurate, and convenient diagnostic tools. Biosensors compact devices that can monitor health in real-time—are becoming essential, especially in point-of-care settings and for continuous health tracking at home. This shift reflects not just advances in medical technology, but also a broader move toward more personalized and proactive healthcare.

The growing global health crisis surrounding chronic diseases is a major force behind the rising demand for biosensors. One of the most pressing challenges is the diabetes epidemic millions of adults around the world now live with diabetes and require daily glucose monitoring to manage their condition. Continuous glucose monitors (CGMs), a standout success in biosensor technology, have become essential tools for these patients, offering real-time insights and improving quality of life.

Cardiovascular diseases (CVDs) are another major concern, responsible for a significant number of deaths each year worldwide. In this context, biosensors are proving to be lifesaving tools. By enabling the rapid, point-of-care detection of critical cardiac markers like troponin, they allow for much faster diagnoses, which can be crucial in emergency settings and significantly improve patient outcomes. Beyond diabetes and heart disease, the global burden of cancer, neurological disorders, and other chronic illnesses continues to rise.

These conditions often require ongoing, precise monitoring—an area where biosensors excel. Their ability to deliver continuous, non-invasive, and accurate data is making them an indispensable part of modern healthcare, driving their adoption across both clinical and home-based settings.

Biosensor technology is advancing rapidly, with a strong focus on improving accuracy, usability, and connectivity. One of the most exciting developments is the enhanced sensitivity and specificity of modern biosensors. Thanks to innovations in materials science, nanotechnology, and microfluidics, today’s biosensors can detect even the tiniest traces of biomarkers making early diagnosis more precise and reliable than ever before.

At the same time, there’s a clear trend toward miniaturization and portability. Devices are becoming smaller, more user-friendly, and easier to use outside of traditional clinical settings. From handheld glucose meters to wearable patches, biosensors are now accessible for home use, remote monitoring, and even in-the-field applications, empowering individuals to take control of their health. What truly sets the current generation of biosensors apart is their integration with advanced digital technologies. Artificial intelligence (AI) and machine learning (ML) are being used to interpret biosensor data with greater accuracy and even predict potential health issues—supporting earlier interventions and more personalized treatment plans.

Meanwhile, the Internet of Things (IoT) allows biosensors to transmit real-time health data directly to healthcare providers, enabling continuous monitoring and immediate alerts in case of critical changes. With the added benefit of wireless communication, patients and doctors can stay connected across distances, making healthcare more proactive, efficient, and responsive.

Despite their growing potential, the development and commercialization of biosensors come with significant financial challenges. Creating next-generation biosensor platforms—especially those that incorporate cutting-edge technologies like nanotechnology, artificial intelligence, or complex biological recognition elements—demands intensive investment in research and development.

This isn’t just about funding; it also involves acquiring specialized materials, advanced laboratory equipment, and hiring highly skilled experts, all of which drive up initial costs. Manufacturing these sophisticated devices is another expensive endeavor. Many biosensors require intricate microfabrication processes, often carried out in controlled cleanroom environments, particularly for silicon-based models. Even with ongoing efforts to reduce costs through innovative approaches—such as using plastic-based graphene materials—scaling up these cost-effective solutions to commercial production levels remains a significant hurdle.

Moreover, before any biosensor reaches the market, it must pass through a rigorous validation process to confirm its accuracy, safety, and reliability. This involves extensive testing, regulatory reviews, and clinical evaluations—all of which add to the overall expense. While these steps are essential to ensure quality and patient safety, they contribute to the high cost of bringing a biosensor from concept to reality.

Navigating the regulatory landscape is one of the biggest challenges facing biosensor developers, especially those targeting the medical diagnostics space. Devices intended for clinical use must meet strict standards set by regulatory bodies such as the U.S. Food and Drug Administration (FDA), the European Medicines Agency (EMA), and other national health authorities.

These approval processes are often lengthy, complex, and expensive—requiring detailed documentation and extensive clinical trials to prove that the biosensor is safe, effective, and reliable. One of the key issues is that regulations often lag behind technological innovation. As new breakthroughs emerge such as AI-powered biosensors or devices made with novel nanomaterials regulatory frameworks can struggle to keep up.

This mismatch can lead to delays in approvals and slow down the introduction of promising new technologies to the market. In addition, regulators require a large volume of high-quality data to evaluate a biosensor’s performance. This includes proof of accuracy, consistency, safety, and clinical relevance, which can be particularly difficult and costly to gather when dealing with new biomarkers or cutting-edge applications. For companies looking to launch their biosensors internationally, the challenge grows even more complex. Each country or region may have its own regulatory standards and processes, forcing manufacturers to meet a patchwork of compliance requirements.

This need for multi-jurisdictional approval significantly increases development costs and extends the time it takes to bring new products to market, potentially slowing innovation and limiting global accessibility.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Wearable Biosensors Non-Wearable Biosensors (or Embedded Devices/Point-of-Care Devices)

|

| By Technology Type |

Electrochemical Biosensors Optical Biosensors Piezoelectric Biosensors Thermal Biosensors Nanomechanical Biosensors, Others) Consumables Instruments Services Therapeutics (Small Molecule Drugs, Biologics, Cell & Gene Therapy) Diagnostics

|

| By Application |

Medical Diagnostics Environmental Monitoring Food and Beverages Agriculture Research & Development Biodefense/Security

|

| By End-User |

Healthcare & Diagnostics Food and Beverage Industry Pharmaceutical & Biotechnology Companies Academic and Research Institutes Environmental Agencies Security and Biodefense Agencies Cosmetics Industry Agriculture Sector |

| Key Players |

Abbott Laboratories F. Hoffmann-La Roche Ltd Medtronic Bio-Rad Laboratories, Inc. DuPont Dexcom, Inc. LifeScan IP Holdings, LLC Masimo Nova Biomedical Universal Biosensors ACON Laboratories Siemens Healthineers Biosensors International Group, Ltd. Cytiva LifeSignals Conductive Technologies Nix Biosensors Inc. Strados Labs Inc. i-Sens, Inc. SD Biosensor, Inc. Koninklijke Philips N.V. Thermo Fisher Scientific Zimmer & Peacock AS Dynamic Biosensors Pinnacle Technology Applied Biosensors Monod Bio Aromyx Agilent Technologies Sartorius Group GRIP Molecular Technologies InnerPlant |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Biosensors Market is categorized by product type, by technology, by application and by end-user. Each segment is rapidly evolving, with different areas of the industry growing at their own pace and shifting in how much of the market they represent. The biosensors market can be segmented across various dimensions to provide a comprehensive understanding of its structure and dynamics.

Biosensors come in a variety of forms, with wearable and non-wearable types serving different needs in healthcare and daily life. Wearable biosensors are integrated into everyday items like smartwatches, fitness trackers, smart glasses, and even clothing. These devices allow for continuous or on-demand health monitoring tracking everything from heart rate, sleep patterns, and physical activity to more advanced metrics like ECG, hydration, and even tear glucose levels through smart lenses. Innovations also extend to smart shoes for gait analysis and neckwear that can monitor posture or vocal patterns.

Adhesive sensor patches are another breakthrough, offering seamless, continuous tracking of biomarkers like glucose. On the other hand, non-wearable biosensors are more commonly found in clinical, lab, or home environments. These include devices like glucose monitors, blood analyzers, and breathalyzers, along with home diagnostic kits for conditions such as pregnancy, cholesterol levels, or infectious diseases. While not worn, they play a critical role in quick and convenient point-of-care testing. Together, these technologies are reshaping how we approach health—making it more proactive, personalized, and accessible.

Biosensors come in various types, each leveraging different scientific principles to detect biological signals with precision. Among them, electrochemical biosensors lead the market thanks to their accuracy, versatility, and affordability. These sensors measure electrical signals generated by biochemical reactions and include subtypes like amperometric, potentiometric, voltammetric, and conductometric sensors.

Optical biosensors are another powerful category, using light to detect biological changes in real time. Known for their sensitivity and ability to work without chemical labels, this group includes technologies like Surface Plasmon Resonance (SPR), colorimetric, and fluorescence biosensors. Piezoelectric biosensors detect shifts in mass or viscosity by observing oscillation patterns, with acoustic and microcantilever variants being the most common. Thermal biosensors operate by measuring heat changes during chemical reactions—offering reliable performance without frequent recalibration.

Meanwhile, nanomechanical biosensors are at the cutting edge, using nanoscale components to achieve ultra-sensitive and rapid detection. In addition, a range of emerging biosensor technologies is continuously expanding the landscape, offering new possibilities for medical diagnostics, environmental monitoring, and more.

Biosensors are transforming a wide range of industries, with medical diagnostics standing out as the largest area of application. As chronic diseases continue to rise globally, there’s an increasing need for fast, accurate, and user-friendly diagnostic tools. Biosensors are at the heart of this shift, playing a crucial role in point-of-care (POC) testing—used for everything from glucose monitoring and cardiac marker detection to pregnancy tests and cancer screening. They’re also widely used in home diagnostics, allowing individuals to manage conditions like diabetes or check cholesterol levels without visiting a clinic. Beyond diagnostics, biosensors are valuable tools in drug discovery and infectious disease screening, helping researchers and healthcare providers detect illnesses quickly and effectively. They’re also essential for continuous health monitoring, tracking vital signs and activity levels.

Outside the medical field, biosensors serve critical roles in environmental monitoring—detecting harmful pollutants, toxins, and pathogens in air, water, and soil. In the food and beverage industry, they ensure product safety by identifying contaminants, allergens, and microbes. In agriculture, they’re used to monitor soil conditions, track plant diseases, and even assess livestock health. Additionally, biosensors are key tools in research labs for various biochemical studies, and in biodefense and security applications, where they help detect biological threats and microbial agents. Altogether, these diverse applications highlight the expanding impact of biosensor technology across healthcare, science, and industry.

Biosensors are being adopted across a wide range of sectors, with healthcare and diagnostics leading the way. In hospitals, clinics, diagnostic labs, and point-of-care (POC) settings, these devices support faster, more accurate diagnosis and monitoring of various health conditions. They’re also increasingly used in home healthcare, allowing patients to track vital signs or manage chronic illnesses like diabetes with greater ease and independence.

Medical device companies are at the forefront of developing and integrating biosensor technologies into next-generation tools. Beyond healthcare, biosensors are making a significant impact in the food and beverage industry, where they help ensure product safety by detecting contaminants and allergens. In pharmaceutical and biotechnology companies, biosensors play a vital role in drug discovery, development, and quality control processes.

Academic and research institutes rely on them for a wide range of biological and biochemical studies, while environmental agencies use biosensors to monitor pollution and detect toxins in air, water, and soil. Security and biodefense agencies also employ biosensors to identify potential biological threats.

Even industries like cosmetics and agriculture are embracing this technology for product testing, monitoring soil and crop health, and tracking animal well-being. The growing adoption across these varied sectors highlights the versatility and transformative potential of biosensors in both clinical and non-clinical settings.

North America stands as the dominant force in the global biosensors market, maintaining the largest share and projected to continue leading well beyond 2030. In 2024, the region accounted for nearly 44.8% of the global market, a position driven by several key factors. One of the biggest contributors is the high and growing prevalence of chronic diseases such as diabetes and cardiovascular conditions health issues that now affect millions of Americans and are expected to impact up to 170 million people by 2030.

This rising disease burden fuels strong demand for rapid diagnostics and continuous health monitoring solutions. Supporting this growth is North America’s advanced healthcare infrastructure, characterized by high spending, cutting-edge facilities, and widespread access to medical technologies. The region is also a hub for innovation, home to major biosensor manufacturers and a strong R&D ecosystem that consistently delivers breakthroughs in wearable biosensors and point-of-care diagnostics.

While regulatory requirements especially in the U.S. can be stringent, bodies like the FDA provide clear guidance and pathways for device approval, encouraging innovation and market entry. The growing number of CLIA waivers for certain point-of-care devices is also making it easier for these tools to reach more users. Another major trend driving growth is the rising popularity of home diagnostics and wearable health technologies. Consumers are increasingly turning to smartwatches, fitness trackers, and sensor patches for real-time health monitoring from the comfort of their homes.

Beyond healthcare, biosensors are also finding applications in areas like environmental monitoring and biodefense, further expanding their impact. Within the region, the U.S. is by far the largest market, but Canada also plays a meaningful role in shaping North America’s biosensor landscape.

Europe holds a strong position in the global biosensors market, accounting for a significant share that continues to grow steadily. Much like North America, the region benefits from rising healthcare needs, increasing awareness, and rapid technological progress.

One of the key drivers in Europe is the growing emphasis on early disease detection—especially through national screening programs for conditions like cancer and prenatal disorders—which has led to greater demand for accurate, easy-to-use biosensors. The continent’s aging population is another important factor. As more people live longer, the incidence of age-related chronic diseases such as diabetes and cardiovascular disorders is increasing, creating a greater need for continuous health monitoring and diagnostic devices.

In response, many European countries are investing heavily in biosensor research, particularly in cutting-edge areas like nanotechnology and lab-on-a-chip systems, which support the trend toward rapid, point-of-care testing. Government support has also been crucial. Across Europe, various public health initiatives and funding programs are aimed at improving diagnostic capabilities and promoting innovation in medical technology.

At the same time, there is a growing shift toward personalized and preventive medicine an area where biosensors play a key role by offering real-time insights tailored to individual patient needs. Germany, the U.K., France, Italy, and Spain are among the largest contributors to the European market, with the U.K. expected to experience especially strong growth between 2025 and 2030. This regional momentum reflects Europe’s commitment to modernizing healthcare while making diagnostics more accessible and efficient.

The Asia Pacific region is emerging as the fastest-growing market for biosensors, with projections showing it will register the highest compound annual growth rate (CAGR) between 2025 and 2030. This remarkable momentum is driven by a combination of demographic, economic, and healthcare-related factors. With its massive and still-growing population particularly in countries like China and India the region has an enormous pool of patients affected by chronic and lifestyle-related diseases.

Conditions such as diabetes and cardiovascular disorders are becoming increasingly common, fueled by rapid urbanization, shifting dietary habits, and sedentary lifestyles. According to the International Diabetes Federation, over 90 million adults in Southeast Asia were living with diabetes in 2021 a number expected to rise to 113 million by 2030. To meet these growing healthcare needs, governments across Asia Pacific are investing in improving healthcare infrastructure and expanding access to diagnostic tools, especially in rural and underserved areas.

There’s also a rising demand for point-of-care (POC) diagnostics that are fast, accurate, and affordable making biosensors an ideal solution. At the same time, rising disposable incomes are enabling greater adoption of advanced medical technologies, including continuous monitoring devices and wearable biosensors. Supportive government policies and increased public and private investment in healthcare research and development are also playing a key role in accelerating growth. Many countries are encouraging local manufacturing and innovation partnerships, making it easier to bring new technologies to market.

The region is also quick to embrace digital health tools, with widespread adoption of wearable biosensors that integrate with smartphones and cloud platforms for real-time monitoring and data analysis. Key markets in the region include China, Japan, India, South Korea, and Australia. Among these, India is expected to post the highest growth rate through 2030, driven by ongoing advancements in healthcare technology, a thriving research ecosystem, and a strong push toward affordable and accessible diagnostics.

The Middle East and Africa (MEA) region is steadily emerging as a promising market for biosensors, with growth expected to gain pace in the coming years. Several factors are contributing to this upward trend, starting with increased healthcare spending across the region. Governments are investing in upgrading healthcare infrastructure and expanding access to medical services, especially in countries like Saudi Arabia, the UAE, and South Africa.

At the same time, growing public awareness around health and wellness—combined with a rising burden of chronic conditions such as hypertension and hyperlipidemia—is driving demand for effective monitoring tools. Home-based health monitoring is also becoming increasingly popular in MEA, mirroring global trends toward more convenient and patient-centered care.

Wearable biosensors and at-home diagnostic devices are being embraced by a population looking for easier ways to manage ongoing health conditions. Government initiatives aimed at strengthening healthcare delivery and promoting technological adoption are further supporting this shift. However, the region still faces some challenges. Limited reimbursement frameworks and complex regulatory environments can create hurdles for both manufacturers and healthcare providers, potentially slowing market adoption. Despite these obstacles, key markets like South Africa, Saudi Arabia, and the UAE are showing strong potential.

Notably, South Africa is projected to register the highest growth rate in the use of photoplethysmography (PPG) biosensors between 2024 and 2030, reflecting a growing interest in digital and wearable health solutions across the region.

The market was valued at USD 28.22 billion in 2024.

The market is projected to grow at a CAGR of 11.15% from 2025 to 2033.

Medical segment holds the largest market share.

Asia-Pacific region is expected to witness the highest growth rate.

Major players include Abbott Laboratories, Roche Diagnostics, Medtronic, and Bio-Rad Laboratories.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Biosensors Market, y Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Biosensors Market, By Technology Type

5.3 Biosensors Market, By Application

5.4 Biosensors Market, By End-User

6.1 North America Biosensors Market, By Product Type

6.1.1 Biosensors Market, By Technology Type

6.1.2 Biosensors Market, By Application

6.1.3 Biosensors Market, By End User

.2 U.S.

6.2.1 Biosensors Market, By Product Type

6.2.2 Biosensors Market, By Technology Type

6.2.3 Biosensors Market, By Application

6.2.4 Biosensors Market, By End-User

.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America