Biotechnology & Pharmaceutical Services Market

Biotechnology & Pharmaceutical Services Market Share & Trends Analysis Report, By Service Type (Consulting Services, Regulatory Affairs Services, Product Maintenance Services, Product Upgrade Services, ERP Services, Auditing & Assessment, Training Services) By Application (Oncology, Infectious Diseases, Cardiovascular Diseases, Neurology, Immunology, Other Applications) By End User (Pharmaceutical Companies, Biotechnology Companies, Medical Device Manufacturers, Contract Research Organizations, Academic & Research Institutes) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 6.2%

Last Updated : March 7, 2026

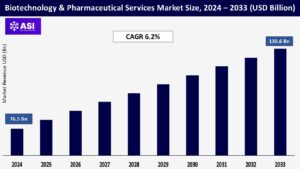

The global Biotechnology & Pharmaceutical Services Market was valued at approximately USD 76.5 billion in 2024 and is projected to reach USD 130.6 billion by 2033, growing at a CAGR of 6.2% during the forecast period (2025–2033).

Biotechnology and pharmaceutical services include a range of selected services that are outsourced to assist drug discovery, development, regulatory approval, manufacturing, and commercialization. The services include but are not limited to regulatory affairs, consulting, product lifecycle management, pharmacovigilance, clinical trial support, and training. These services can be found throughout most pharmaceutical and biotechnology firms, as they are common parts of processes that create efficiencies for operations, help mitigate timelines, and navigate increasingly complicated global regulatory reviews.

Increases in R&D spending by companies; enhanced complexities of clinical trials; and the need for governmental regulatory expertise are driving the market opportunities. Fast adoption of digital tools and artificial intelligence are reforming the service landscape in trial management and analytics. Emerging markets, such as India and China, are driving rapid expansion in the Asia Pacific because of cost, talent, and government incentives.

The increase in costs and complexities associated with drug development has led to a growing dependence on outsourced biotechnology and pharmaceutical services. Drug and biotech companies are under pressure to cut time to market but must also meet regulatory requirements and increasing R&D budget pressures.

According to the Pharmaceutical Research and Manufacturers of America (PhRMA), the global biopharmaceutical industry had over USD 244 billion in R&D investment in 2023, with an annual increase projected for the next decade. However, there are limitations to internal capacities, particularly when scaling and speed are needed for investigative multi-phase trials in therapeutic areas such as oncology, rare diseases, and gene therapies.

For this reason, many are outsourcing key functions such as regulatory affairs, clinical trial management, pharmacovigilance, or commercialization support services to a specialized service provider. For instance, in January 2024, Pfizer entered a multi-year relationship with Parexel to improve its speed and operational capabilities for oncology and immunology clinical trial execution and regulatory operations. Similarly, Moderna also continued its relationship with IQVIA to scale its global vaccine development programs.

Through these partnerships, pharmaceutical innovators can access global resources and expertise to help leverage their limitation… operational risk, and overall cost. It is the trend in training and executing R&D activities outside of companies that is paramount in stimulating growth in the biotechnology and pharmaceutical services market worldwide.

The growth in global pharmaceutical markets brings complexity in meeting diverse and changing regulatory environment. Regulatory authorities (e.g., U.S. FDA, the European Medicines Agency (EMA), and China’s NMPA) have increased their scrutiny of clinical trial protocols, safety reporting, and product labeling, which has prompted companies to seek external regulatory assistance.

According to the Regulatory Affairs Professionals Society (RAPS), over 60% of mid-sized biopharma recognized an expanded challenge for preparing global submissions in 2023, pointing to different data standard frameworks, documentation formats, and post market surveillance requirements across countries. This burden has significantly driven the demand for regulatory affairs services such as dossier preparation, compliance auditing, and lifecycle management. For example, in February 2024, Thermo Fisher Scientific announced the expansion of its regional regulatory consultancy businesses in Asia to support regional and multinational companies engage in the ASEAN harmonization framework.

Similarly, in 2024, Syneos Health released AI-base regulatory intelligence products to track guidelines, and help sponsors assess the risk of non-compliance in order to minimize delayed application filing. Furthermore, emerging therapeutic areas including cell & gene therapy or RNA-based drugs are creating customized regulatory strategies and are adding to the need to hire experts.

A significant limitation in the biotechnology and pharmaceuticals services market is the growing worry about security breaches of data or theft of intellectual property (IP) associated with the outsourcing of critical operations. As pharmaceutical companies and biotech companies increasingly engage with a third-party service provider (especially across borders), they put sensitive clinical data as well as some protected or proprietary drug formulations and regulatory documents at risk, along with exposing themselves to potential cyber or legal loopholes.

For example, a 2023 report by IBM Security states that the average expense incurred from a healthcare data breach was USD 10.93 million making it the highest among all industry classes. Outsourcing operations and/or services in regions with a lower standard of data protection increases companies’ exposure to non-compliance with global frameworks such as HIPAA, GDPR, or 21 CFR Part 11, and can be particularly troublesome when clinical trial data, patient information, or manufacturing processes are taken into account.

As an example, a reputable clinical research organization (CRO) in EU in 2022 encountered a ransomware incident that resulted in their trial data for several clients being compromised, which significantly delayed client submissions and also resulted in damage to trust between the stakeholders. Additionally, while there is a high concern regarding the leakage of IP, most notably when outsourcing to low-cost countries or areas where there is a low culture of enforcement of regulation or legislation, or even a low strength of patent stewardship. This can discourage some companies from completely outsourcing all R&D or regulatory functions particularly in early-stage drug development.

The potential for an IP breach as well as regulatory liability poses a significant risk for the market’s growth especially for emerging biotech companies, and with multinational partnerships. Tackling these obstacles involves tighter cybersecurity protocols, solid legal agreements, and more oversight which can raise costs and diminish the appeal of outsourcing.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Service Type |

Consulting Services Regulatory Affairs Services Product Maintenance Services Product Upgrade Services ERP Services Auditing & Assessment Training Services |

| By Application |

Oncology Infectious Diseases Cardiovascular Diseases Neurology Immunology Other Applications |

| By End User |

Pharmaceutical Companies Biotechnology Companies Medical Device Manufacturers Contract Research Organizations Academic & Research Institutes |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Biotechnology & Pharmaceutical Services Market is segmented by service type, application, end-user. Each segment plays a pivotal role in supporting drug development, regulatory compliance, and commercialization across the global life sciences industry.

By 2024, the consulting services segment will have exceeded the largest revenue share of the market, as this segment continues to show increasing demand from small to mid-sized biotechnology clients for strategic advice on product development, market entry and commercialization. Also, with the increasing complexity of regulatory beginnings and the increasing complexity of clinical pipelines, consulting services offer tone cadence for the regulatory landscape and time market acceleration.

One regulatory affairs service that is expected to grow out the fastest through 2033 is primarily a result of the overall growth of pharmaceutical operations globally, regulatory principles becoming tighter in the U.S., Europe, Asia-Pac, that direct professionals services and consultants.

Today, organizations are looking for regulatory consultants in response to include international filings, dossiers for drafting, and compliance with evolving regulations like GDPR, FDA, ICH, and others. Other segments like product maintenance services, ERP services, auditing & training segments continue to grow as companies are looking for full-service offering solutions that come with quality assurance on post-market compliance.

Oncology is expected to be the most significant application segment—driven by the increasing rate of development for cancer drugs and the highly complicated regulatory pathways connected to oncology therapeutics. Specialized services like clinical trial design, regulatory submissions, and pharmacovigilance continue to see high demand due to the proliferation of new therapies such as immuno-oncology and CAR-T cell therapies.

Infectious Diseases takes the second largest segment, further buoyed up from recent global efforts to combat diseases such as COVID-19, HIV, and hepatitis. Biotechnology and pharma companies engaged in vaccinology and anti-infective drug discovery extensively use consulting and regulatory services with the hopes of speeding up their approval process and satisfying a recognized community need.

Both the Cardiovascular and neurology application segments steadily expand, based on aging populations that require chronic care and increased complexity through management of trial protocols and compliance with chronic disease research.

Pharmaceutical Companies are the biggest end users in 2024, and will represent a major share of service demand. Pharmaceutical Companies will continue to outsource essential services, like regulatory submissions, clinical operations, and quality audits, to reduce costs and allow for an increased focus on their core R&D.

Biotechnology Companies will be the fastest growing service user category, especially smaller and mid-size emerging biotech companies that tend not to have their own staffing resources dedicated to regulatory or corporate strategy. Emerging smaller biotechs specifically are initiating more partnerships with service providers to navigate drug development, deal with IP, and for global launches, and as always they are up against de-risking agendas in answering to Boards of Directors and investors.

Contract Research Organizations (CROs) and medical device manufacturers are often repeat and very valuable users that frequently subordinate key specialized functions like regulatory intelligence, regulatory or optimization training, and/or integrating ERP Systems with company specific processes.

In 2024, North America is projected to hold the largest share of the market at 41.2%. This large market size is a result of a strong biopharmaceutical industry and a mature pharmacy/healthcare infrastructure in the region. Also, the region has a large biopharmaceutical industry, government and pharmaceutical investment into research and development, and a well-defined and regulated infrastructure of research and development.

In North America, the United States is the largest contributor, primarily through biopharmaceutical companies Pfizer, Merck, Johnson & Johnson, Amgen, etc. The biopharmaceutical companies use large external resource service providers to outsource significant amounts of regulatory, research, and clinical work to save time and streamline processes. There is also a well-defined regulatory environment in North America due to the U.S. Food & Drug Administration (FDA) that includes a strong need for consulting and compliance services and regulatory affairs experts.

Additionally, the large pipeline of biologics, cell therapies, and mRNA drugs in the United States also drives growth and demand for service providers with expertise in biologics or the associated services. Canada adds to the NFC or North American life science corporation environment with its own development of an expanding biotechnology ecosystem and useful government incentives and investments.

Europe remains a prominent regional market with strong activity in countries such as Germany, Switzerland, the United Kingdom, France and the Netherlands. This region represents around 27.8% of global market share as of 2024. There is greater demand for biotechnology and pharmaceutical services and products as processes become more difficult to regulate, especially with the evolving EMA’s frameworks and national level health technology assessments (HTA’s).

For example, there was more outsourcing of various regulatory and compliance services in Germany, and the U.K. regulatory framework has been affected by Brexit, giving rise to a biosimilar industry in both the countries prompting regulatory changes. The region is able to benefit competitively from the number of available CROs and specialized consultancies offering biopharma, pharmacovigilance, GMP compliance, and clinical operations.

The Asia-Pacific market is the fastest-growing segment, with a forecasted CAGR of 7.6% during the forecast period (2025-2033). In 2024 the Asia-Pacific market was around 21.5 % of global revenues and there is significant growth forecast, given high urbanization rates, affordable, skilled labor, and increased activity in clinical trials. India, China, Korea and Japan are major contributors. India has been at the forefront of the expansion of regulatory services, along with pharmacovigilance and medical writing.

This has been supported among other initiatives by the “Pharma Vision 2020” initiative of the Indian government, and tax incentives for research and development. Meanwhile China is emerging as an increasingly significant global player with large amounts of investment in manufacturing of biotechnology and reforming regulatory regimes under National Medical Products Administration (NMPA). The region functionally provides easier access for early-phase trials and development of biosimilars.

Moderate growth has been experienced in the Latin America and Middle East & Africa regions, buoyed by improving healthcare infrastructure and an uptick in foreign investment in life sciences. Brazil, Mexico and Argentina, for example, New Latin American countries are increasingly participating in clinical trials and outsourcing assurance and regulatory consulting services.

In MEA, the UAE, Saudi Arabia and South Africa are extending further into pharmaceutical manufacturing and distribution; however, the regions are still challenged with issues such as limited regulatory harmonization, inequitable healthcare access and economic disparities. Notwithstanding, the ever-increasing burden of chronic diseases and the need to align the regulatory environments with global standards will further enhance the demand for outsourced services.

The Biotechnology & Pharmaceutical Services market was valued at USD 76.5 billion in 2024.

The market is projected to grow at a CAGR of 6.2% from 2025 to 2033.

The pharmaceutical services segment hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include IQVIA and Parexel International, Charles River Laboratories.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Biotechnology & Pharmaceutical Services Market , By Service Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Biotechnology & Pharmaceutical Services Market, By Application

5.3 Biotechnology & Pharmaceutical Services Market, By End User

6.1 North America Biotechnology & Pharmaceutical Services Market, By Country

6.1.1 Biotechnology & Pharmaceutical Services Market , By Service Type

6.1.2 Biotechnology & Pharmaceutical Services Market, By Application

6.1.3 Biotechnology & Pharmaceutical Services Market, By End User

6.2 U.S.

6.2.1 Biotechnology & Pharmaceutical Services Market , By Service Type

6.2.2 Biotechnology & Pharmaceutical Services Market, By Application

6.2.3 Biotechnology & Pharmaceutical Services Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping