Cancer Cachexia Market

Cancer Cachexia Market Share & Trends Analysis Report, By Therapeutics Type (Progestogens (e.g., Megestrol Acetate), Corticosteroids, Combination Therapies, Others), By Mechanism of Action (Appetite Stimulators, Weight Loss Stabilizers), By Distribution Channel (Hospital Stores, Retail Pharmacies, Online Pharmacies)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

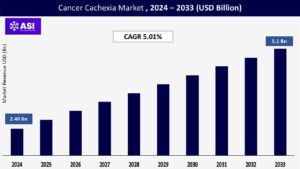

CAGR: 5.01%

Last Updated : March 13, 2026

The worldwide cancer cachexia market size was valued at approximately USD 2.48 billion in 2024 and is projected to reach USD 5.1 billion by 2033, demonstrating a compound annual growth rate (CAGR) of 5.01% during the forecast period of 2025–2033.

The Cancer Cachexia Market plays a vital and increasingly important role in the pharmaceutical and healthcare industries. Cancer cachexia is a serious and complex condition that affects many people living with cancer, especially those in the advanced stages of the disease. Unlike ordinary weight loss, cachexia involves involuntary weight loss, severe muscle wasting, loss of appetite, and a noticeable decline in strength and daily function. It’s not just a side effect it deeply affects a patient’s quality of life, making it harder to tolerate cancer treatments and often leading to worse outcomes. In fact, cachexia can directly contribute to death in cancer patients, even before the cancer itself. Because of its profound impact, there is a growing urgency to develop better ways to manage and treat cachexia, which is driving investment and expanding the cancer cachexia market size.

One of the most critical forces driving the cancer cachexia market is the rising global burden of cancer itself. As cancer diagnoses continue to increase worldwide, so does the number of patients vulnerable to cachexia, a severe and often overlooked complication. This debilitating condition affects between 50% and 80% of cancer patients, especially those battling advanced-stage cancers like pancreatic, gastric, lung, and head and neck tumors.

It’s not just numbers; these are real people facing intense physical decline, weight loss, and muscle wasting, which drastically reduce their quality of life and ability to respond to treatment. With organizations like the World Health Organization projecting a sharp rise in new cancer cases over the coming decades, the need for effective cachexia treatments is becoming more urgent than ever. This growing demand underscores the critical importance of advancing supportive care solutions alongside cancer therapies and contributes directly to the expansion of the cancer cachexia market size.

Scientific research has made significant strides in uncovering the complex biology behind cancer cachexia, revealing how inflammatory molecules like IL-6, TNF-α, and GDF-15, along with tumor-derived factors and metabolic disruptions, contribute to this debilitating condition. This deeper understanding is now fueling the development of more targeted and effective treatments.

A wave of promising therapies is emerging, such as Pfizer’s Ponsegromab, a GDF-15 inhibitor showing encouraging results in clinical trials, along with other innovative candidates like ghrelin receptor agonists (e.g., Anamorelin), myostatin inhibitors, activin receptor blockers, and multi-target agents. At the same time, there’s a growing realization that cachexia is too complex for a one-size-fits-all solution. This has led to a shift toward combination and multimodal therapies that integrate medication with nutritional support, physical activity, and psychological care, offering a more holistic and patient-centered approach to managing this life-altering condition. This shift toward targeted and multimodal therapies is supporting sustained cancer cachexia market growth.

One of the biggest challenges in tackling cancer cachexia is that it often goes unrecognized or is diagnosed too late, which can limit the short-term expansion of the market size. Many times, it’s mistaken for simple weight loss, general malnutrition, or just an inevitable part of cancer. This delay is largely due to the lack of clear, widely used diagnostic criteria and limited awareness among healthcare providers, especially those outside of specialized oncology settings.

As a result, cachexia often isn’t identified until it has already progressed to a severe stage, limiting the effectiveness of potential interventions. Compounding the problem is the absence of a universally accepted clinical definition and staging system. While efforts like the GLIM criteria have helped move things forward, inconsistencies still exist across research and clinical practice, making it hard to compare data or standardize care.

Additionally, the field still lacks definitive biomarkers for early detection and treatment monitoring. Although molecules like GDF-15 are showing promise, we don’t yet have a reliable set of tools to catch cachexia early or measure how well treatments are working. This makes proactive and personalized care much more difficult, ultimately affecting outcomes for patients who need timely support the most.

Cancer cachexia is not a simple condition; it’s a complex and multifaceted syndrome that stems from a mix of factors, including chronic inflammation, metabolic imbalances like insulin resistance, accelerated breakdown of fat and muscle, reduced appetite, and substances secreted by tumors themselves. This complexity makes it incredibly difficult to treat with a single drug. Traditionally, treatments have relied on repurposed medications like appetite stimulants (e.g., megestrol acetate) and corticosteroids, but these offer only modest benefits, come with significant side effects, and fail to address the core issue of muscle wasting.

Even when patients receive nutritional support, many experience what’s known as “anabolic resistance,” meaning their bodies can’t effectively use nutrients to rebuild muscle, so simply increasing calorie intake isn’t enough. On top of that, cachexia severely weakens patients, making it harder for them to tolerate standard cancer treatments like chemotherapy, radiation, or surgery. This often results in reduced doses, delays, or treatment interruptions, which can directly impact the success of their cancer care. Despite progress in drug development, truly effective therapies that can comprehensively reverse cachexia remain a critical unmet need.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Therapeutics Type |

Progestogens (e.g., Megestrol Acetate) Corticosteroids Combination Therapies Others |

| By Mechanism of Action |

Appetite Stimulators Weight Loss Stabilizers Other Mechanisms of Action |

| By Distribution Channel |

Hospital Stores Retail Pharmacies Online Pharmacies. |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The cancer cachexia market is categorized by therapeutic type, by mechanism of action, and by distribution channel. Each segment is rapidly evolving, with different areas of the industry growing at their own pace and shifting in how much of the market they represent. Each segment provides a comprehensive understanding of its dynamics and growth opportunities. The Cancer Cachexia Market is typically segmented to provide a comprehensive understanding of its various facets, enabling market players to identify opportunities and strategize effectively.

The cancer cachexia treatment landscape is evolving, with various drug classes targeting different aspects of this complex condition. Traditionally, progestogens such as megestrol acetate have dominated the market and accounted for a significant market share due to their appetite-stimulating effects. These drugs are relatively affordable but fall short in improving lean muscle mass, which is crucial for maintaining strength. Corticosteroids like dexamethasone and methylprednisolone are also commonly used for their anti-inflammatory and appetite-boosting effects, though their long-term use is limited by significant side effects.

Recognizing that cachexia is driven by multiple interconnected factors, there is growing interest in combination therapy, a more holistic approach that blends different drugs with supportive strategies like nutrition and exercise. This segment is gaining momentum as it allows for multiple pathways to be targeted simultaneously, for example, stimulating appetite while preserving muscle mass.

Meanwhile, emerging therapies are generating excitement for their novel mechanisms of action. These include ghrelin receptor agonists like Anamorelin (already approved in Japan), which can increase appetite and potentially enhance muscle mass; GDF-15 inhibitors like Pfizer’s Ponsegromab, designed to block an appetite-suppressing signal; myostatin and activin receptor inhibitors, which aim to prevent muscle breakdown; as well as SARMs, anti-inflammatory agents, and cannabinoid-based therapies. Together, these newer treatments reflect a shift toward more targeted, effective, and patient-tailored solutions for managing cancer cachexia.

Cancer cachexia therapies can also be understood based on how they work to relieve symptoms and improve patient outcomes. Appetite stimulants remain the cornerstone of treatment and dominated the market in 2023, a trend expected to continue. These drugs, such as megestrol acetate, corticosteroids, and anamorelin, primarily aim to boost food intake, helping patients regain some strength by improving their overall nutritional status. However, as our understanding of cachexia deepens, there’s a growing emphasis on not just increasing appetite but also preserving muscle mass and stabilizing weight.

This has led to rising interest in therapies like myostatin and GDF-15 inhibitors, along with other anabolic agents that actively work to prevent the muscle wasting at the heart of cachexia. This shift reflects a broader movement toward treating the root causes rather than just the visible symptoms. Additionally, there’s a category of treatments that operate through other mechanisms of action, targeting the inflammation, metabolic imbalances, or tumor-derived signals that contribute to the syndrome. Together, these diverse therapeutic strategies are shaping a more nuanced and comprehensive approach to managing cancer cachexia.

Cancer cachexia products reach patients through several key distribution channels, each playing a unique role in ensuring access and continuity of care. Hospital pharmacies and hospital stores remain the dominant distribution point, as hospitals are often where cancer is first diagnosed and treated. These settings provide immediate access to specialized cachexia medications and nutritional therapies as part of a coordinated care plan, making them a critical touchpoint for early intervention.

Retail pharmacies also play an essential role, particularly in supporting patients over the long term. They offer convenient, ongoing access to medications and supplements once patients transition to outpatient care, helping to maintain treatment consistency.

Meanwhile, online pharmacies are emerging as a fast-growing segment, thanks to the rise in digital healthcare, doorstep delivery services, and often more competitive pricing. This channel is increasingly valued for its convenience and potential to improve treatment adherence, especially when it comes to ongoing supportive care products that patients may need regularly from the comfort of their homes.

North America continues to lead the global cancer cachexia market and holds the largest market share due to high cancer prevalence and strong healthcare infrastructure. This leadership is driven by several key factors. First and foremost is the high prevalence of cancer in the U.S. and Canada, which naturally results in a larger population affected by cachexia. The region also benefits from a highly developed healthcare system, with strong infrastructure, substantial investments in medical research, and early adoption of new and emerging treatments. There’s also a higher level of awareness among healthcare providers and patients about the importance of supportive care in cancer, including cachexia management. Affordability and favorable reimbursement policies further improve access to treatment.

Additionally, many of the world’s leading pharmaceutical and biotech companies are headquartered in North America, actively investing in R&D and bringing innovative therapies through the pipeline. Several promising drugs for cancer cachexia are currently in advanced stages of clinical development here, expected to drive even more growth as they enter the market.

Europe is poised for impressive growth in the cancer cachexia market, with a strong compound annual growth rate (CAGR) projected over the coming years. This momentum is largely driven by the rising number of cancer cases across the region, particularly types like lung, colorectal, and head & neck cancers, which are more commonly associated with cachexia. As awareness continues to grow among both patients and healthcare professionals, there’s increasing recognition of the need to actively diagnose and manage cachexia as part of comprehensive cancer care.

Europe also benefits from a strong research ecosystem, with leading universities, specialized research centers, and significant government funding fueling advancements in treatment. Widely approved therapies such as megestrol acetate and medroxyprogesterone acetate are already in use across many countries, particularly for cancer- and AIDS-related cachexia.

Additionally, the region is seeing a steady increase in pharmaceutical activity, with numerous clinical trials underway and more companies entering the space. Within Europe, the United Kingdom stands out as a key contributor, thanks to its robust life sciences sector, strong academic collaborations, and a well-established pharmaceutical industry driving innovation and market growth.

The Asia Pacific region is emerging as the fastest-growing market for cancer cachexia therapies, with the highest projected CAGR during the forecast period. This surge is largely driven by the region’s vast and expanding cancer patient population, especially in countries like China and India, where the burden of advanced-stage cancers is on the rise. At the same time, healthcare infrastructure across the region is improving rapidly, with increased investments in hospitals, diagnostics, and access to specialized treatments, particularly in urban areas.

Rising disposable income levels are also playing a key role, enabling more patients to afford advanced and targeted therapies that were once out of reach. Governments are stepping up as well, with stronger support for public health initiatives and growing awareness campaigns focused on cancer-related conditions like cachexia. Additionally, local pharmaceutical companies are becoming more active, investing heavily in R&D, distribution networks, and new product launches. A notable example is the approval of Adlumiz (anamorelin) in Japan, a targeted therapy specifically developed for cancer cachexia. Together, these factors are creating a dynamic and promising environment for market growth across the Asia Pacific region.

Regions such as Latin America, the Middle East, and Africa currently hold a smaller share of the global cancer cachexia market, but they are not without potential. One of the main challenges in these areas is the lack of awareness, both among the general public and healthcare providers,s about the importance of supportive care in managing cancer cachexia. This often leads to late or missed diagnoses. Additionally, limited reimbursement policies make it difficult for many patients to afford costly cancer treatments and supportive therapies, creating a major barrier to access. In some areas, an underdeveloped healthcare infrastructure further compounds the problem, restricting the availability of specialized care and advanced medications.

However, the situation is gradually evolving. As cancer incidence continues to rise and governments increase healthcare spending, there is a growing window of opportunity. These regions are beginning to invest more in healthcare development and awareness initiatives, which could pave the way for long-term growth in cancer cachexia treatment and care.

The cancer cachexia market was valued at USD 2.48 billion in 2024.

The cancer cachexia market is projected to grow at a CAGR of 5.1% from 2025 to 2033.

The progestogens segment holds the largest market share of the Cancer Cachexia.

Asia-Pacific region is expected to witness the highest growth rate.

Major players include Pfizer, Novartis, Merck, Eli Lilly, Bristol-Myers Squibb, AbbVie, Actimed Therapeutics, Aeterna Zentaris, and others.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Cancer Cachexia Market, By Therapeutic Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Cancer Cachexia Market, By Mechanism of action

5.3 Cancer Cachexia Market, By Distribution Channel

6.1 North America Cancer Cachexia Market, By Country

6.1.1 Cancer Cachexia Market, By Therapeutic Type

6.1.2 Cancer Cachexia Market, By Mechanism of action

6.1.3 Cancer Cachexia Market, By Distribution Channel

6.2 U.S.

6.2.1 Cancer Cachexia Market, By Therapeutic Type

6.2.2 Cancer Cachexia Market, By Mechanism of action

6.2.3 Cancer Cachexia Market, By Distribution Channel

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

Teva Pharmaceutical Industries Ltd.

Astellas Pharma Inc.

Daiichi Sankyo Company Limited.

Sun Pharmaceutical Industries Ltd.

Perrigo Company plc.

Kyowa Kirin Co. Ltd.

Hikma Pharmaceuticals plc.

Endo International plc.

Aspen Pharmacare Holdings Limited.

Lupin Limited.

Mallinckrodt plc.

Akorn Inc.