Cannabis Testing Market

Cannabis Testing Market Share and Trend Analysis, By Technology (Chromatography-Based Testing, Spectroscopy-Based Testing, Other Technologies), By Application (Potency Testing, Pesticide Screening, Residual Solvent Testing, Heavy Metal Testing, Terpene Profiling, Microbial Analysis), By End User (Cannabis Cultivators, Cannabis Product Manufacturers, Testing Laboratories, Research and Academic Institutions) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 14.7%

Last Updated : August 4, 2025

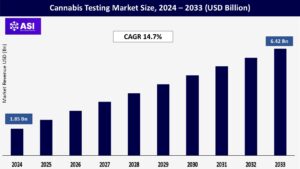

The global Cannabis Testing Market was valued at USD 1.85 billion in 2024 and is projected to reach USD 6.42 billion by 2033, expanding at a compound annual growth rate CAGR of 14.7% during the forecast period (2025 – 2033).

Cannabis testing is the method of scientifically examining cannabis products to establish the existence of contaminants, cannabinoid levels (e.g., THC and CBD levels), terpene content, and residual solvents, among others. It has a vital role in maintaining public safety, particularly as medical and recreational cannabis becomes legal in an increasing number of jurisdictions around the world. Agencies like the U.S. FDA and Health Canada, and state regulations, impose high standards of quality control on the industry. The principal areas of application are potency analysis, heavy metal and pesticide testing, terpene identification, and microbiological analysis. The demand for standardized, third-party certification of the quality of cannabis in order to provide consumer confidence, compliance with regulation, and commercial competitiveness drives the market.

The fast-growing legalization of cannabis for medical as well as recreational use in North America, select regions of Europe, as well as new Asian and Latin American markets has brought about a regulatory environment that requires uncompromising testing protocols. For example, more than 30 U.S. states legalized medical marijuana, and almost 20 states have legalized recreational marijuana. In each state, cannabis manufacturers must comply with the local or national testing standards, hence the need for certified marijuana testing labs and equipment.

This regulatory movement has spurred large investments in third-party laboratories, data management and reporting compliance software, and sophisticated analytical equipment like gas chromatography (GC), high-performance liquid chromatography (HPLC), and mass spectrometry (MS). Governments are also implementing greater transparency and consumer protection measures. For instance, Health Canada requires microbial, pesticide, and solvent residual analysis for every batch released. The cannabis legalization wave has also led other labs outside the cannabis industry to expand their lines of services and get into the cannabis testing business. Global increases in legal cultivation and distribution channels serve as a strong impetus for the cannabis testing market to grow.

With the growing number of recreational and medical cannabis consumers has grown the need for accurate potency labeling and contaminant-free product. It is a necessity now to deliver consistent cannabinoid content and purge the products of toxic material such as mold, pesticide, or residual solvent to deliver consumer confidence and brand integrity. Contamination and mislabeling-driven product recalls not only damage brand reputation but are also at the expense of public health.

Thus, producers employ certified laboratories and high-throughput analyzers for real-time and batch testing to reduce risks and meet changing regulatory requirements. The increasing application of cannabis in pediatric epilepsy, pain care, and oncology in medical use especially underlines the importance of uniform dosage and absence of toxic contaminants. In addition, with cannabis-infused edibles and wellness products becoming diversified, analysis becomes even more important in order to maintain uniformity across modalities of delivery. As the market matures, the customers are becoming increasingly educated and are demanding complex terpene and cannabinoid profiles, further increasing the role of advanced testing services in the cannabis value chain.

Despite profitable growth of the cannabis industry, it takes enormous capital and regulatory issues to set up and maintain cannabis testing labs. High-performance analytical equipment such as HPLC, LC-MS, and GC-MS is expensive, and six-figure amounts are usually required for them. In addition, skilled people who can operate these instruments and obtain measures correctly are required, which involves overhead for laboratories. Also, laboratories will need to spend on regular calibration, maintenance, and periodic upgrade to keep abreast with changing testing standards, contributing to higher costs.

Along with equipment cost, obtaining regulatory certification such as ISO/IEC 17025 accreditation or state-level licensure involves time-consuming recordkeeping, regular audits, and continuous proficiency testing, all of which raise the operational entry barrier. Small-scale cannabis farmers or analytico-chemistry facilities in new markets may not be profitable to conduct full-service in-house analysis and rely on third-party labs instead, further concentrating the market around existing participants. Further, differences in regional test requirements lead to operational inefficiencies and a lack of streamlined service delivery across boundaries. This disbursed compliance environment can slow product launches and make cross-regional trade more complex.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Chromatography-Based Testing Spectroscopy-Based Testing Other Technologies

|

| By Application |

Potency Testing Pesticide Screening Residual Solvent Testing Heavy Metal Testing Terpene Profiling Microbial Analysis

|

| By End User |

Cannabis Cultivators Cannabis Product Manufacturers Testing Laboratories Research and Academic Institutions

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Cannabis analysis is generally classified into two primary drug types: Cannabinoid Testing and Contaminant Testing. Cannabinoid testing is crucial for quantifying active constituents like tetrahydrocannabinol (THC), cannabidiol (CBD), cannabigerol (CBG), and cannabichromene (CBC). This analysis enables accurate product labeling and supports correct dosage for medicinal and recreational purposes. It also keeps regulatory compliance about legal THC limits. Cannabinoid testing captures the highest market share in this category because it has a direct bearing on consumer expectations, physician approval, and shop price. In contrast, contaminant testing is acquiring tremendous significance owing to health issues that are associated with chemical and microbial contamination.

This involves testing for pesticides, heavy metals such as arsenic, mercury, lead, and cadmium, and residual solvents employed in the process of extraction, microbial contaminants like mold, E. coli, Salmonella, and mycotoxins. Increased concern over product recalls, toxic shock, and public safety has driven governments to implement stringent contaminant limits. As such, cannabis manufacturers are increasingly investing in multi-residue analysis equipment to suit and quick testing devices. The contaminant testing market is growing rapidly, and it plays a significant role in establishing long-term customer confidence and regulatory acceptance.

Cannabis analysis is used in various important areas such as Potency Testing, Pesticide Screening, Residual Solvent Analysis, Terpene Profiling, and Microbial Examination. Potency testing accounts for the largest share and constitutes measuring active cannabinoids such as THC and CBD. True potency details are required on packaging and ensures that consumers get the expected effect and dosage. In medical products, it is also important not to under- or over-dose, particularly among vulnerable groups such as pediatric or geriatric patients. Pesticide and residual solvent analysis are given greater emphasis by regulators with increasing frequency, considering that most growers apply off-label agrochemicals or inadequately controlled extraction methods.

Non-removal of these toxins can pose serious health threats, especially when cannabis is vaped or smoked. Ultra-low detection technologies like LC-MS/MS are highly sought for this intention. Terpene profiling is a new niche that provides information on flavor, aroma, and therapeutic synergy. Terpene information is applied for differentiation by premium cannabis brands. Microbial testing, particularly for the presence of pathogens such as mold, Aspergillus, or Listeria, is required for safety, especially among immunocompromised consumers. In total, each of these applications targets specific health and regulatory needs and plays a role in a rich and varied testing ecosystem.

End-users of the cannabis testing market are categorized under Testing Laboratories, Cannabis Cultivators, Cannabis Product Manufacturers, and Academic & Research Institutions. The majority of them are testing laboratories. They perform third-party, unbiased analysis to satisfy regulations of safety and compliance. Governments of North America and Europe require that batches of cannabis be tested by accredited laboratories prior to hitting the dispensaries. These laboratories have state-of-the-art equipment, such as LC-MS, GC-MS, and HPLC, and frequently hold certifications such as ISO/IEC 17025, instilling confidence in their outputs. Cannabis growers and product manufacturers, previously reliant solely on third-party labs, are now becoming prominent end users.

As benchtop testing equipment becomes more accessible and user-friendly, many businesses are incorporating in-house testing to speed up turnaround time and enhance production control. Internal laboratories assist with tracking potency, screening for contaminants, and avoiding costly product recalls. Academic and research centers are also becoming increasingly stakeholders. Since cannabis is now legalized in various parts of the globe, universities and biotech laboratories are investigating the pharmacology, therapeutic utility, and genetics of the plant. Their participation will also rise, especially in developing new cannabis-based products and testing safety and efficacy using preclinical studies

The North American region controls the cannabis testing industry, with the United States taking the lead because of extensive legalization across various states. Well-developed cannabis culture, a network of established third-party labs, and stringent regulatory environments drive leadership here. Strong public visibility, additional R&D investment, and strict compliance environments further drive market growth here. Canada, with complete federal legalization, also offers well-developed laboratory environments and mandatory testing needs, positioning the region as very appealing for testing equipment vendors and service labs.

Europe is the second-largest market, with the UK, Germany, and the Netherlands leading the pack. The increasing legalization of medical cannabis in Europe and the need for pharmaceutical-grade products have driven the necessity for sophisticated testing services. The EU has strict regulatory standards for pesticide residues, microbial load, and heavy metal levels that manufacturers must conduct extensive lab testing on. Growing imports of cannabinoid medicines also drive regional testing demand.

The Asia-Pacific region is experiencing accelerated growth, fueled by evolving regulatory environments and increasing cannabis research. Thailand and South Korea have started to liberalize medical cannabis laws, and Japan and Australia are promoting regulated therapeutic use. Public funding into cannabinoid research and more collaborative efforts between countries are also driving testing service uptake. As quality and safety awareness grows, so does the demand for consistent, standardized cannabis testing facilities, particularly for export-oriented production hubs in the region.

LATAM and MEA are slowly developing markets. Colombia and Brazil have legalized medical cannabis, and they are drawing in foreign investment, and proper testing structures are required. Israel, with its innovative R&D environment for cannabis, is a regional innovation and lab standard leader. But regulatory ambiguity, underdeveloped infrastructure, and disparate enforcement are holding back wider adoption of testing in some areas of Africa. In spite of all the complications, continued reforms and international demand for cannabis exports are stimulating investments in testing infrastructure and lab accreditation.

The global Cannabis Testing Market was valued at USD 1.85 billion in 2024.

The cannabis testing market is projected to grow at a CAGR of 14.7 % from 2025 to 2033.

The Potency Testing hold the largest market share of cannabis testing.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Agilent Technologies, Thermo Fisher Scientific, Shimadzu Corporation, PerkinElmer, and Waters Corporation.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Cannabis Testing, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Cannabis Testing, By Application

5.3 Cannabis Testing, By End User

6.1 North America Cannabis Testing Market, By Country

6.1.1 Cannabis Testing, By Technology

6.1.2 Cannabis Testing, By Application

6.1.3 Cannabis Testing, By End User

6.2 U.S.

6.2.1 Cannabis Testing, By Technology

6.2.2 Cannabis Testing, By Application

6.2.3 Cannabis Testing, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping