Cannula Market

Cannula Market Share & Trends Analysis Report By Product Type (Nasal Cannula, Venous Cannula, Arterial Cannula, Cardiac Cannula, Vascular Cannula, Dermal/Filler Cannula, Other) By End User (Hospitals & Clinics, Ambulatory Surgical Centers, Diagnostic Centers, Cosmetic Surgery Centers, Home Healthcare, Others) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

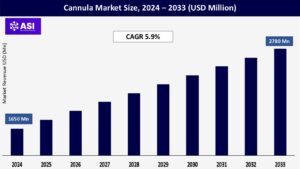

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 5.9%

Last Updated : August 27, 2025

The global Cannula Market was valued at approximately USD 1650 million in 2024 and is projected to reach USD 2780 million by 2033, growing at a CAGR of 5.9% during the forecast period (2025–2033).

Cannulas are flexible tubes put into the body for fluid delivery, oxygen therapy, and other medical processes, including cosmetic surgery, cardiovascular procedures, and surgical procedures. Cannulas can be used for venous access, arterial monitoring, as an oxygen source, and for administering aesthetic fillers. Nasal cannulas and other types of oxygen delivery systems are used in respiratory care, while vascular and cardiac cannulas are often used in procedures such as vascular bypass and Extracorporeal Membrane Oxygenation (ECMO). Several factors drive market expansion, such as increasing surgical volumes around the world, the rise in minimally invasive procedures, and an increase in the aging population that requires long-term medical care.

Other benefits that will speak to growth are the increasing demand for aesthetic procedures, such as the use of microcannulas, as well as several technological advances in the materials and design of cannulas for aesthetic and medical purposes. The rise in chronic diseases, such as cardiovascular disease and respiratory disorders, also reinforces demand for cannulas in both clinical and home healthcare settings.

The continued global rise in both elective and emergency surgery involving procedures from cardiovascular to orthopedic to cosmetic surgery are underestimated factors driving the growth of the cannula market. Cannulas are indispensable in medical practice for the administration of fluids, transfusion of blood products, oxygen delivery, and delivery of medications during hand on times in the scope of a procedure.

The World Health Organization (WHO) estimates there are 234 million major surgeries everyday around the world, and that numbers continue to rise due to a rising supply of healthcare services available to populations in developing countries. In tandem, chronic diseases such as diabetes, respiratory conditions, and cancers are on the rise. For example, the International Diabetes Federation (IDF) states that the total population of diabetes worldwide reached 537 million in 2023, and is projected to increase to 783 million by 2045 and for many of those individuals, they will either require long-term (months to years) intravenous access, insulin infusion (via cannula), or short-term (days to months) oxygen therapy via nasal cannula.

The increased burden of disease, will require widespread variety of cannulas in hospitals, outpatient settings and homecare. The post pandemic recovery of the healthcare system has also led to an increase in cancelled out-patient surgeries and elective surgeries getting rescheduled. In addition to the global cannula market factors being discussed, there will continue to be an increased used of vascular access devices and fluid management in acute and chronic care settings and reflected in the growing cannula.

The aesthetic medicine market has experienced tremendous growth and considerable interest, particularly surrounding the use of microcannulas for cosmetic filler injections, which provide a less painful, safer option for patients than traditional sharp needles. Blunt-tip microcannulas can reduce the likelihood of bruising, swelling and vascular injury during procedures such as lip augmentations, cheek volume injections, and jawline contouring, stemming from sharp needle punctures.

These cannulas have opened the door to larger usage by dermatologists and plastic surgeons. According to the International Society of Aesthetic Plastic Surgery (ISAPS), there were over 18.8 million non-surgical aesthetic procedures performed across the world in 2023, with dermal fillers being one of the top three requested. Regions with a high demand include North America, Europe and certain portions of Asia-Pacific with a high demand among middle-aged and younger segments of society almost exclusively engaging in minimally invasive beauty enhancements.

Leaders within the industry – including TSK Laboratory and SoftFil – have continued to innovate within microcannula technology by producing ultra-thin wall cannulas or cannula products with more flexible (shaft) options to increase precision and patient comfort. The increase in aesthetic procedures as a result of growing societal acceptance, and rising disposable incomes – especially seeing the influence of social media – will continue to spur demand in the microcannula segment, especially the market growth for cannulas in the cosmetic realm.

The risk of complications associated with cannulas (e.g. infections, vascular injuries, thrombosis, or air embolism) secondary to improper insertion, extended use, or subpar quality will essentially constrain the global cannula market. Adverse and sub-optimal clinical results not only reduce patient safety, but also lead to apprehension among healthcare workers about using certain types of cannulas, especially in critical care and long-term intravenous therapy.

Furthermore, product recalls as a result of manufacturing deficiencies (e.g., catheter detract or rupture, malfunctioning valves that cause premature injections of fluid, or leaks) present unique challenges to market growth. For instance, in September 2023, the U.S. Food and Drug Administration (FDA) issued a Class I recall (the most serious form of recall) for a lot of venous cannulas used in extracorporeal circulation due to the risk of blood leakage which could lead to serious injury or death.

These adverse events impair the perception of the product and manufacturer, lead to regulatory scrutiny, and dissuade procurement of the product by healthcare settings. Thus, fear of difficulties and stringent post-marketing surveillance policies might delay the adoption of cannulas altogether (especially in resource-poor environments where quality assurance and training may be an issue).

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Nasal Cannula Venous Cannula Arterial Cannula Cardiac Cannula Vascular Cannula Dermal/Filler Cannula Other |

| By End User |

Hospitals & Clinics Ambulatory Surgical Centers Diagnostic Centers Cosmetic Surgery Centers Home Healthcare Others |

| Key Players |

Terumo Corporation Braun Melsungen AG Smiths Medical (ICU Medical) Medtronic plc Teleflex Incorporated BD (Becton, Dickinson and Company) Boston Scientific Corporation CardioMed Supplies Inc. Nipro Corporation Conmed Corporation |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Cannula Market is segmented by product type and end-user. Each segment plays a critical role in supporting diverse medical, surgical, and aesthetic procedures globally.

In 2024, Nasal Cannula held the largest market share due to its widespread use across many types of respiratory therapy, particularly for patients with chronic obstructive pulmonary disease (COPD), COVID-19, and other respiratory conditions. Its non-invasive nature, low cost, and ease of use with oxygen concentrators also contribute to its primary status as a form of respiratory therapy for patients needing oxygen in hospital and homecare settings.

According to the WHO, 3 million deaths directly due to COPD occur each year, indicating the sustained demand for nasal cannulas. The Venous Cannula segment is rapidly achieving growth, attributed to increasing applications in cardiac surgeries and extracorporeal membrane oxygenation (ECMO). Venous cannulas are critical in any procedure involving cardiopulmonary bypass, particularly as heart surgeries will become more frequent in response to the increasing occurrences of cardiovascular disease in North America and globally.

Lastly, the Dermal/Filler Cannula segment is displayed rapid growth in the aesthetics sector. The dermal microcannulas have many advantages compared to using needles that have led to their rapid adoption in injecting dermal fillers. This is primarily because the much lower risk of trauma to body tissues, ease of use and accuracy of filler placement. With over 18 million non-surgical cosmetic procedures performed in 2023, this segment is forecasted to continue achieving growth in North America and Europe.

In 2024, the cannula market was dominated by Hospitals & Clinics, accounting for over 58% of the overall market share. The market share for Hospitals & Clinics continued to weigh heavily due to patients undergoing a high-volume of inpatient surgeries, trauma care and emergency procedures that had to utilize cannulation. The larger hospitals typically had a high volume of cannulae available in house to make certain they had arterial, vascular, etc for clinical use.

Though not as robust as Hospitals & Clinics, Ambulatory Surgical Centers (ASCs) continue to see an increase in their individual cannulae demand as outpatient procedures become increasingly popular. Many minimally invasive surgeries require specialized cannulas, such as laparoscopic surgery or aesthetic procedures. This allows ASCs to provide a mechanism for the cannulae demand as a rapidly growing segment of the end-user market. Cosmetic Surgery Centers provide a very small, yet growing end-user segment.

As there is an increase in social acceptance and disposable incomes in urban areas, microcannula demand for aesthetic enhancements (including Botox and dermal fillers) is rapidly expanding. Home Healthcare is poised to emerge as a sizable segment due to the trend toward managing chronic disease at home. Major applications for cannulae in homecare include oxygen therapy, insulin infusion and hydration therapy using nasal and intravenous cannulae primarily among older adult patients.

In 2024, North America accounted for the largest market share of 38.6% that was primarily determined by its well-established healthcare system, the wide adoption of minimally invasive surgical procedures in addition to a large number of surgical cases. The US is the largest contributor to the cannula segment, as hospitals, ambulatory surgical centers and cosmetic clinics are increasingly employing cannulas in their surgical practices.

There has been a spike in cosmetic procedures that utilize dermal filler cannulas, along with a constant demand for nasal cannulas and venous cannulas for respiratory and cardiac care. Additionally, with the support of prominent manufactures and rapid adoption of innovative technologies for cannulas, it highlights the strength in North America’s dominance in the cannula market.

Europe continues to be a strong contributor to the cannula segment on a worldwide basis, as strong market countries such as Germany, France, the UK, and Italy was a leader in both medical and aesthetic procedures. Growth in the older population and rising levels of chronic diseases, specifically cardiovascular disease and respiratory disease, are driving demand for vascular and nasal cannulas.

Eurostat reports that the volume of surgical interventions (such as bypass and orthopedic procedures) continues to increase across all of Europe. Moreover, the growing trends of experiencing aesthetic enhancements with the use of microcannulas (specifically in France and the UK) has created an expanding cosmetic segment in Europe.

The Asia Pacific region is anticipated to grow at the fastest rate of CAGR 7.4% for the period 2025-2033. This growth is driven by increasing healthcare investments, improved access to medical facilities, and increased awareness of cosmetic surgery.

Some of the most developing nation markets (China, India, South Korea, and Japan) have large patient populations and there is a growing demand for both therapeutic and aesthetic procedures. Cannulas are expected to become more popular in clinical adolescence due to increasing government programs that encourage the promotion of surgical infrastructure and chronic disease management (like in India, and China).

Latin America and the Middle East & Africa have moderate growth in the cannula markets. In Latin America, the demand for aesthetic procedures is growing in countries like Brazil and Mexico, which will help drive some growth for filler cannulas. At the same time, the increase in the number of surgical procedures and ICU admissions is contributing to an increasing demand for vascular and nasal cannulas.

In the Middle East & Africa, relatively good growth in the cannula markets is going to occur, as the healthcare modernization in Saudi Arabia, UAE, and South Africa is driving demand for cannulas in dramitic fashion, despite some challenges, including limited access to healthcare, lower per capita income, limited or no healthcare updates in other areas of the region, and regulatory variability.

The market was valued at USD 1650 million in 2024.

The market is projected to grow at a CAGR of 5.9% from 2025 to 2033.

The vascular Cannula hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Terumo Corporation, B. Braun Melsungen AG and Smiths Medical (ICU Medical)

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Cannula Market By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Cannula Market By End User

6.1 North America Cannula Market, By Country

6.1.1 Cannula Market, By Product Type

6.1.2 Cannula Market By End User

6.2 U.S.

6.2.1 Cannula Market, By Product Type

6.2.2 Cannula Market By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping