Chemiluminescence Immunoassay Market

Chemiluminescence Immunoassay Market Share and Trend Analysis, By Product (Instruments, Consumables, Software & Services), By Sample Type (Blood, Urine, Saliva, Others), By Application (Therapeutic Drug Monitoring, Oncology, Cardiology, Endocrinology, Infectious Disease, Autoimmune Disease, Others), By End User (Hospitals and Clinics, Medical and Diagnostic Laboratories, Pharmaceutical and Biotechnology Companies, Others) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

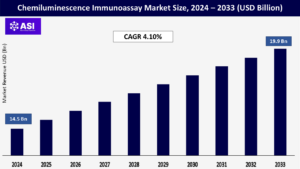

CAGR: 4.10%

Last Updated : July 17, 2025

The global Chemiluminescence Immunoassay market was valued at USD 14.5 Billion in 2024 and is projected to reach USD 19.9 billion by 2032, expanding at a compound annual growth rate (CAGR) of 4.10 % during the forecast period (2026 – 2033).

The diagnostic method known as Chemiluminescence Immunoassay (CLIA) combines light-emitting detection with antibody-based reactions to detect and measure particular compounds in biological samples. A mainstay of contemporary clinical laboratories, CLIA is well-known for its high accuracy, speed, and dependability. It is frequently used to identify and track infections, cancers, hormone imbalances, and autoimmune diseases. The approach is perfect for high-volume testing in medical facilities, research institutes, and diagnostic centres because it allows for both qualitative and quantitative analysis. Its ability to work with automated systems reduces human error, improves operational efficiency, and streamlines workflows. Furthermore, CLIA can handle a variety of sample types, such as blood, urine, and saliva, which increases its applicability in a range of healthcare contexts.

As a result, there is a steady increase in demand for CLIA instruments and consumables worldwide. Furthermore, the growing demand for accurate, economical, and prompt diagnostic solutions is reflected in the continuous improvements in CLIA technology. As a result, the market is expanding steadily due to its critical role in improving laboratory productivity, raising patient care standards, and addressing the global rise in infectious and chronic diseases. The necessity of CLIA in contemporary healthcare systems is further supported by ongoing innovation, which guarantees that it stays at the forefront of diagnostic techniques.

CLIA systems successfully meet the need for quick, precise results at scale that modern labs require. Errors and manual labour are greatly decreased by automated features like remote diagnostics, integrated reagent systems, and robotic sample handling. Thousands of tests can now be processed every day by high-volume labs and hospitals without the need for additional staff. CLIA is an affordable option for increasing throughput and turnaround times because modular analyser designs allow for smooth capacity expansion as testing requirements increase.

The need for accurate biomarker tracking has increased due to the rise in chronic illness cases, such as diabetes, heart disease, and cancer, which has sped up the adoption of CLIA. The significance of highly sensitive tests for screening and treatment monitoring is also highlighted by the regular occurrence of infectious disease outbreaks. CLIA’s crucial role in diagnostics is further supported by the demand for routine hormone, cardiac, and cancer testing brought on by aging populations. These health trends directly drive market expansion by incentivizing labs to upgrade from antiquated systems to cutting-edge CLIA platforms.

Customized treatment plans rely on thorough biomarker analysis, which is supported by the sensitivity and accuracy of CLIA. In domains such as oncology and the treatment of autoimmune diseases, the technology enables the simultaneous testing of genomic markers, hormone levels, and protein panels, allowing for accurate patient classification. In order to progress biomarker research and create treatment-specific diagnostics, pharmaceutical companies and research institutes are consequently investing more in CLIA. This compatibility with frameworks for precision medicine keeps increasing market uptake and establishes CLIA as a vital instrument for contemporary healthcare innovation.

With individual analyzers frequently costing hundreds of thousands of dollars, the upfront cost of sophisticated CLIA systems continues to be a significant obstacle. Upfront expenditures are further increased by infrastructure improvements, employee training, and installation. Budgets are strained by recurring expenses for calibration kits, proprietary reagents, and required service contracts, especially in environments with limited resources. The adoption of CLIA may be delayed in emerging economies by smaller labs or clinics that favor less expensive options like ELISA or rapid tests.

High-end system maintenance also necessitates specialized technicians, which increases operational complexity. Public healthcare systems and rural facilities bear a disproportionate amount of the financial burden, even though long-term efficiency gains partially offset the costs. As a result, manufacturers encounter difficulties breaking into price-sensitive markets where, because of financial limitations, obsolete equipment continues to exist.

Labs face financial uncertainty due to regionally inconsistent reimbursement policies for CLIA-based tests. For example, in certain nations, insurance coverage gaps for more recent assays discourage labs from upgrading systems out of concern for unrecovered expenses. Development timelines are prolonged by months or years due to regulatory obstacles, such as the FDA or EMA’s strict approval procedures for new tests. Smaller manufacturers frequently lack the resources necessary to handle intricate compliance requirements, which hinders innovation and gives larger competitors an advantage.

Administrative burdens are also increased by changing data privacy and quality control regulations. Approval delays also affect patient care in rapidly evolving fields like oncology by delaying the availability of vital tests. These difficulties deter investment in CLIA innovations, strengthening established players’ market dominance. Labs in areas with unclear reimbursement policies, meanwhile, experience revenue instability, which further slows adoption rates and keeps them dependent on outdated technology.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product |

Instruments Consumables Software & Services |

| By Sample Type |

Blood Urine Saliva Others |

| By Application |

Therapeutic Drug Monitoring Oncology Cardiology Endocrinology Infectious Disease Autoimmune Disease Others |

| By End User |

Hospitals and Clinics Medical and Diagnostic Laboratories Pharmaceutical and Biotechnology Companies Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Chemiluminescence Immunoassay market is divided into instruments, consumables, and software & services. Automated CLIA instruments are gaining traction due to their precision, scalability, and rapid turnaround times, which are essential in high-throughput environments like diagnostic laboratories. The consumables segment, comprising reagents, test kits, and disposable materials, represents a recurring revenue stream and accounts for the largest market share, driven by the continuous demand for routine diagnostic tests. Meanwhile, the software and services segment are expanding as labs increasingly adopt data-driven diagnostic systems and require real-time analytics and technical support for workflow optimization and compliance with regulatory standards.

Based on sample type, blood continues to dominate the market due to its widespread use in detecting a broad range of biomarkers linked to various diseases. However, urine and saliva samples are gaining popularity due to their non-invasive nature and ease of collection, particularly in home-based testing and pediatric or geriatric populations. Urine is especially utilized in drug screening and hormone monitoring, while saliva testing is emerging in hormone profiling and infectious disease diagnostics. The “others” category, including cerebrospinal fluid (CSF) and tissue extracts, supports niche diagnostic needs, particularly in neurological or oncological investigations.

In terms of application, the CLIA market finds its strongest foothold in therapeutic drug monitoring (TDM), where it ensures safe and personalized dosing by measuring precise drug concentrations. Oncology is another significant segment, driven by the rising global cancer burden and the growing need for early detection and monitoring via tumor markers. Cardiology benefits from CLIA’s ability to detect cardiac enzymes, critical in diagnosing acute coronary syndromes.

Endocrinology is another key application area, particularly with the rising prevalence of thyroid disorders, diabetes, and adrenal diseases, where hormone level quantification is essential. The infectious disease segment has witnessed a surge in demand, especially post-COVID-19, where sensitive and specific pathogen detection is vital for managing outbreaks. Autoimmune disease testing, using CLIA for identifying autoantibodies, is also growing steadily due to increased awareness and diagnosis rates. The “others” category encompasses fertility testing, allergy panels, and metabolic screening, reflecting CLIA’s versatility.

When segmented by end user, hospitals and clinics form a significant portion of the market due to their requirement for rapid, on-site diagnostic testing for both inpatients and outpatients. Medical and diagnostic laboratories, however, remain the largest users, owing to their capacity to handle high volumes of tests with the efficiency provided by automated CLIA platforms. Pharmaceutical and biotechnology companies utilize CLIA extensively in clinical trial workflows and biomarker research, supporting drug development and therapeutic validation. Lastly, the academic and research organizations segment, including contract research organizations (CROs), is steadily expanding, leveraging CLIA’s high sensitivity and specificity for specialized studies in translational medicine and biomarker discovery.

Due to its sophisticated healthcare systems, extensive use of automated technologies, and high rates of diagnostic testing per capita, North America accounted for about 41.7% of the global CLIA market in 2024. Large hospital networks and independent labs upgrading to cutting-edge CLIA platforms for quicker, standardized results drove the U.S. to account for more than 34% of regional demand. Market leadership was further cemented by government programs encouraging early disease detection and advantageous insurance coverage.

In 2024, Europe accounted for 28.6% of the global market, with Germany, France, and the United Kingdom leading the way. CLIA adoption was facilitated by centralized laboratory networks and strong public health funding in these countries. The need for accurate diagnostics was accelerated by aging populations and the rise in chronic illnesses like cardiovascular diseases. Despite the regulatory challenges associated with approving novel assays, investments in AI-driven lab solutions and cross-border partnerships are anticipated to maintain a 5.6% CAGR through 2033.

Through 2023, Asia Pacific is expected to grow at a compound annual growth rate (CAGR) of more than 8%, driven by rising rates of diabetes and cancer, urbanization, and growing healthcare budgets in China and India. By setting up rural labs that can handle CLIA, national initiatives like India’s Ayushman Bharat are decentralizing testing. Although there are still infrastructure gaps in remote areas, accessibility is further improved by increased private-sector investments in automated systems and collaborations with international diagnostic companies.

The growing private healthcare networks in Brazil, Mexico, and Argentina are driving growth in Latin America, which accounts for about xx% of the global CLIA market. Adoption is aided by partnerships between regional labs and international diagnostic companies as well as the growing demand for infectious disease and oncology testing. However, reliance on imported instruments, uneven reimbursement policies, and economic volatility impede quicker adoption. In order to increase access, nations like Chile and Colombia are giving priority to lab modernization programs; however, infrastructure deficiencies persist in rural areas. Due to investments in urban healthcare and growing awareness of advanced diagnostics, the region is expected to grow at a 6.1% CAGR.

With growth concentrated in Gulf Cooperation Council (GCC) nations like Saudi Arabia and the United Arab Emirates, the Middle East and Africa account for about xx% of the market. These countries are implementing CLIA for the management of infectious outbreaks and chronic diseases, and they are making significant investments in hospital infrastructure and precision medicine. Sub-Saharan Africa, on the other hand, has difficulties, such as insufficient funding, a dependence on programs funded by donors, and unequal diagnostic coverage outside of major cities. While collaborations with institutions like the WHO seek to close access gaps, initiatives like South Africa’s NHI scheme aim to decentralize testing. Due to geopolitical unpredictability and disjointed healthcare systems in low-income areas, the region is predicted to grow at a 4.2% CAGR.

The global Chemiluminescence Immunoassay market was valued at USD 14.5 billion in 2024.

The market is projected to grow at a CAGR of 4.10 % from 2025 to 2033.

Instruments hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Roche, Abbott and Siemens Healthineers

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Chemiluminescence Immunoassay Market, By Product

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Chemiluminescence Immunoassay Market, By Sample Type

5.3 Chemiluminescence Immunoassay Market, By Application

5.4 Chemiluminescence Immunoassay Market, By End User

6.1 U.K.

6.2 Germany

6.3 France

6.4 Spain

6.5 Italy

6.6 Russia

6.7 Nordic

6.8 Benelux

6.9 The Rest of Europe

7.1 China

7.2 South Korea

7.3 Japan

7.4 India

7.5 Australia

7.6 Taiwan

7.7 South East Asia

7.8 The Rest of Asia-Pacific

8.1 UAE

8.2 Turkey

8.3 Saudi Arabia

8.4 South Africa

8.5 Egypt

8.6 Nigeria

8.7 Rest of MEA

9.1 Brazil

9.2 Mexico

9.3 Argentina

9.4 Chile

9.5 Colombia

9.6 Rest of Latin America

10.1 Canada

10.2 USA

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping