Clinical Diagnostics Market

Clinical Diagnostics Market Share and Trend Analysis, By Technology (Clinical Chemistry, Immunoassays, Molecular Diagnostics (MDx), Hematology, Microbiology, Coagulation/Hemostasis, Urinalysis, Other Technologies), By Application (Infectious Diseases, Oncology, Cardiology, Endocrinology, Genetic Testing, Autoimmune Diseases, Nephrology, Gastroenterology, Other Application), By End User (Hospitals, Diagnostic Laboratories, Physician Offices & Clinics, Other End Users) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

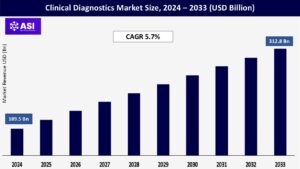

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 5.7%

Last Updated : August 6, 2025

The global Clinical Diagnostics Market was valued at USD 189.5 billion in 2024 and is projected to reach USD 312.8 billion by 2033, expanding at a compound annual growth rate (CAGR) 5.7% during the forecast period (2025 – 2033).

The Clinical Diagnostics Market is made up of an enormous selection of tests, instruments, reagents, and software that are utilized to detect, diagnose, monitor, screen for, and predict diseases and health-related conditions. It is the foundation of evidence-based medicine, delivering critical information to inform clinical decision-making, treatment choice, and patient care. Core technologies involve Immunoassays (ELISA, Rapid Tests), Clinical Chemistry, Molecular Diagnostics (PCR, Sequencing, Microarrays), Hematology, Microbiology, Coagulation, and Urinalysis, increasingly augmented by new areas such as mass spectrometry and digital pathology.

Applications are extremely diverse, ranging from infectious diseases (bacterial, viral, fungal, parasitic) to oncology (cancer screening, diagnosis, prognosis, selection of therapy), cardiology, endocrinology (diabetes, thyroid), genetic disorders, autoimmune disorders, nephrology, and therapeutic drug monitoring. The market addresses diverse end-users such as hospitals, diagnostic laboratories (independent, reference), physician offices/clinics, and increasingly, point-of-care (POC) locations and home testing, backed by integrated data management systems. This ecosystem is pivotal in enabling personalized treatment plans, facilitating population health management, and supporting the transition towards value-based healthcare models by optimizing resource allocation and improving outcomes. Driven by technological advancements, rising disease burden, and the shift towards personalized and preventive medicine, clinical diagnostics is fundamental to improving patient outcomes and healthcare efficiency globally.

The growing incidence of chronic diseases such as cancer, cardiovascular disease (CVD), diabetes, and chronic respiratory disease is a key driver of the clinical diagnostics market. A rapidly aging world population is also a strong contributor to this burden, since age is a substantial risk factor for many of these conditions. The World Health Organization projects noncommunicable diseases (NCDs) will account for 86% of the 90 million annual deaths by 2050, underscoring the immense diagnostic demand. Early and accurate diagnosis is paramount for effective management, improving survival rates, and reducing long-term healthcare costs. For instance, cancer diagnostics are crucial for staging, prognosis, and selecting targeted therapies, while CVD diagnostics (lipid panels, cardiac biomarkers) are essential for risk assessment and intervention.

Simultaneously, the persistent threat of infectious diseases, including seasonal outbreaks (influenza, RSV), antimicrobial resistance (AMR), and emerging pathogens (e.g., novel viruses like SARS-CoV-2 demonstrated), necessitates continuous diagnostic vigilance. Globalization and urbanization further accelerate pathogen spread, amplifying testing needs. Outbreaks drive urgent demand for rapid, accurate tests for identification, containment, and treatment. This dual pressure from chronic and infectious diseases creates sustained demand for a wide spectrum of diagnostic tests, instruments, and services, underpinning market growth.

Continuous innovation is revolutionizing clinical diagnostics, acting as a powerful market catalyst. Major developments are the accelerated development of molecular diagnostics (e.g., next-generation sequencing (NGS) for whole genomic profiling in oncology and orphan diseases, digital PCR for ultrasensitive detection), the expansion of point-of-care testing (POCT) devices providing speedy results at the bedside (e.g., glucose monitoring, infectious disease testing, cardiac biomarkers), increasingly augmented by connectivity for integration of data, and the application of Artificial Intelligence (AI) and machine learning (ML) for image interpretation (pathology, radiology), data interpretation, predictive risk modeling, and predictive analytics.

Automation and high-throughput platforms in core laboratories substantially improve efficiency, decrease turnaround times, and limit human error. In addition, the advancement of minimally invasive liquid biopsies (the detection of circulating tumor DNA (ctDNA), cells, or exosomes in blood) provides alternatives to conventional tissue biopsies for cancer diagnosis and monitoring, lowering patient risk and allowing serial monitoring. These technologies enhance diagnostic accuracy, sensitivity, and specificity, enabling earlier detection, personalized treatment strategies, and improved patient monitoring. They also expand accessibility by bringing sophisticated testing closer to the patient (POCT) and making complex analyses more efficient and scalable (automation, AI), thereby driving adoption and market expansion.

The market for clinical diagnostics is beset by massive headwinds in the form of complicated and dynamic regulatory environments, most notably for new and high-complexity tests such as LDTs (Laboratory Developed Tests) and next-generation sequencing (NGS) panels. Securing regulatory clearances (e.g., FDA clearance/ap-proval in the US, CE-IVD marking in Europe) is a time-consuming, expensive, and resource-draining procedure, slowing the introduction to market and innovation. Regulatory demands for clinical validity and utility are being tightened. Equally challenging is the reimbursement environment.

Healthcare payers (government agencies, private insurers) are under constant pressure to control costs, leading to rigorous evidence requirements for coverage decisions and frequent downward pressure on test pricing. Demonstrating clear clinical utility and cost-effectiveness for new diagnostic tests, especially expensive genomic or specialized assays, is difficult and time-consuming. Reimbursement policies often lag behind technological innovation, creating uncertainty for manufacturers and laboratories and potentially limiting patient access to cutting-edge diagnostics. Navigating the intricate web of varying regional regulations and payer policies adds substantial complexity and cost for global market players, acting as a major restraint on market growth.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Clinical Chemistry Immunoassays Molecular Diagnostics (MDx) Hematology Microbiology Coagulation/Hemostasis Urinalysis Other Technologies |

| By Application |

Infectious Diseases Oncology Cardiology Endocrinology Genetic Testing Autoimmune Diseases Nephrology Gastroenterology Other Application |

| By End User |

Hospitals Diagnostic Laboratories Physician Offices & Clinics Other End Users |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The clinical diagnostics market is fundamentally segmented by the underlying technological platforms employed. Clinical Chemistry continues to be a mainstay, automating large-volume analysis of body fluids (urine, blood) for such markers as proteins, enzymes, electrolytes, and glucose, which are critical in the evaluation of metabolic and organ function. Immunoassays, such as ELISA and rapid lateral flow assays, rule serology and hormone testing by virtue of high specificity in detecting antigens or antibodies; they are crucial in infectious disease serology, cardiac markers (troponin), and therapeutic drug level monitoring. Molecular Diagnostics (MDx), including PCR, next-generation sequencing (NGS), microarrays, and isothermal amplification, is the fastest-growing segment. Genomics-driven, its uses range from infectious disease pathogen identification (including multiplex panels) through oncology (somatic/germline mutation detection, MRD monitoring), pharmacogenomics, to genetic disorder screening.

NGS, while more expensive, is increasingly vital to full genomic profiling in cancer. Hematology analyzers run complete blood counts (CBC) and differentials, essential for anemia, infection, and leukemia diagnosis. Microbiology technologies detect pathogens through culture, mass spectrometry (MALDI-TOF), and molecular techniques, essential for antibiotic stewardship in the face of emerging AMR. Coagulation/Hemostasis tests track clotting function (PT/INR, APTT) for anticoagulant treatment and bleeding diseases. Urinalysis is a general screening method for kidney disease, diabetes, and UTIs. Other Technologies include Histopathology/Cytopathology (tissue/cell microscopy, increasingly digital) for cancer diagnosis and Flow Cytometry for immunophenotyping in immunology/oncology. Technology selection follows a general hierarchy driven by the analyte, analytical sensitivity/specificity required, throughput needs, cost, and the clinical environment (centralized lab automation vs. decentralized POCT simplicity).

Market segmentation by application reflects the vast disease areas where diagnostics provide critical insights. Infectious Diseases historically constitutes the largest segment, driven by routine testing for pathogens (bacteria like Strep, viruses like HIV/HPV/Hepatitis, fungi, parasites), outbreak response (COVID-19, influenza, RSV, emerging threats), and the global challenge of Antimicrobial Resistance (AMR) surveillance. Rapid diagnostics for STIs, respiratory infections, and bloodstream infections are constant needs. Oncology is the fastest-growing application segment, fueled by rising cancer incidence and the precision medicine revolution. It includes early detection (mammography adjuncts, PSA, fecal immunochemical tests), definitive diagnosis (biopsy pathology, IHC), prognosis (genomic classifiers), treatment selection (companion diagnostics to targeted therapies, immunotherapy biomarkers such as PD-L1), monitoring of recurrence (by imaging, tumor markers, ctDNA liquid biopsies), and minimal residual disease (MRD) detection.

Cardiology depends on biomarkers (troponin, BNP/NT-proBNP) for diagnosing/prognosing acute myocardial infarction and heart failure, and lipid panels for assessing cardiovascular risk. Endocrinology is dominated by diabetes management HbA1c, glucose monitoring and thyroid function tests TSH, Free T4/T3 Genetic Testing applications are rapidly expanding carrier screening, prenatal diagnostics NIPT, newborn screening, rare disease diagnosis, and pharmacogenomics Autoimmune Diseases diagnostics includes detection of autoantibodies, for example, ANA, RF, anti-CCP Nephrology tests include kidney function creatinine, eGFR, cystatin C damage albuminuria Gastroenterology includes malabsorption studies, liver function tests, and GI infections tests. Other Applications include toxicology (overdose, drugs of abuse), newborn screening panels, and allergy testing.

The clinical diagnostics market addresses unique end-user environments with different volumes of testing and complexities. The largest segment is hospitals, which contain core laboratories performing an enormous volume of routine and emergency tests (chemistry, hematology, routine coagulation, urinalysis, STAT infectious disease tests) 24/7 to serve inpatient services, emergency departments, and associated outpatient clinics. Their scale justifies significant investment in high-throughput automated analyzers and integrated laboratory information systems (LIS). Diagnostic Laboratories, including large independent reference labs (e.g., LabCorp, Quest) and specialized esoteric labs, form another major pillar. They excel in high-volume routine testing sent from physician offices and hospitals (outsourcing) and specialized, low-volume, high-complexity testing (advanced molecular, specialized immunoassays, flow cytometry, cytogenetics) requiring sophisticated equipment and expertise. Consolidation has been a key trend here.

Physician Offices & Clinics are a steadily growing segment, increasingly adopting Point-of-Care Testing (POCT) technologies. These enable rapid, near-patient testing for immediate clinical decisions – examples include glucose monitoring for diabetics, rapid strep/flu/COVID-19 tests, urine dipsticks, basic hematology (Hb), and INR monitoring for anticoagulated patients. POCT provides convenience and shorter turnaround but generally processes lower volumes and less complex tests than core labs. Other End Users are Academic/Research Institutes that are formulating and validating new assays, Home Care Settings using self-testing devices (e.g., glucose meters, coagulation monitors), and Nursing Homes/Long-Term Care Facilities using simple POCT. Decentralization momentum is most pronounced in the Physician Office/Clinic segment due to POCT technological advances.

Dominates the world market, powered by high spending on healthcare, developed infrastructure, quick uptake of new technologies, prominent role of major players, and high incidence of chronic diseases. The US is the single largest national market. Regulatory systems (FDA) and complicated reimbursement systems (Medicare, private payers) have major impacts on the market.

Accounts for a mature and large market, with powerful universal healthcare systems, sophisticated diagnosis facilities, and growing emphasis on customized medicine. Population ageing and technology uptake drive growth, but can be moderated by strict EU regulation (IVDR) and cost pressure in national health services. Germany, France, and the UK are key contributors.

Has the greatest growth potential among regions, driven by huge and aging populations, growing disposable incomes, improved access to healthcare, rising awareness of early diagnosis, high government healthcare infrastructure investments, and medical tourism expansion. China, Japan, and India are especially important growth drivers, although market maturity is highly disparate across the region.

A diverse region with varying levels of market development. Growth is driven by improving healthcare infrastructure (especially in Gulf Cooperation Council (GCC) countries), rising prevalence of infectious and chronic diseases, increasing government initiatives, and growing private sector investment. However, economic volatility, resource limitations, and uneven access to advanced diagnostics remain challenges in many areas.

The global clinical diagnostics market was valued at USD 189.5 billion in 2024.

The clinical diagnostics market is projected to grow at a CAGR of 5.7 % from 2025 to 2033.

The Hospitals hold the largest market share of clinical diagnostics.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Roche Diagnostics, Abbott Laboratories, Siemens Healthineers, Sysmex Corporation, bioMérieux SA, Becton Dickinson (BD), Thermo Fisher Scientific, Qiagen, QuidelOrtho, Hologic, Bio-Rad Laboratories, and Agilent Technologies. These companies compete through innovation, automation, and portfolio breadth.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Clinical Diagnostics Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Clinical Diagnostics Market, By Application

5.3 Clinical Diagnostics Market, By End User

6.1 Clinical Diagnostics Market, By Country Type

6.1.1 Clinical Diagnostics Market, By Technology

6.1.2 Clinical Diagnostics Market, By Application

6.1.3 Clinical Diagnostics Market, By End User

6.2 U.S.

6.2.1 Clinical Diagnostics Market, By Technology

6.2.2 Clinical Diagnostics Market, By Application

6.2.3 Clinical Diagnostics Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping