Continuous Glucose Monitoring Systems Market

Continuous Glucose Monitoring Systems Market Share and Trend Analysis, By Technology (Real-time CGM, Flash Glucose Monitoring, Implantable Sensors, Non-invasive Systems, Pump-Integrated Systems), By Application (Diabetes Management (Type 1 & 2), Hospital Monitoring, Gestational Diabetes, Non-diabetic Wellness, Research), By End User (Healthcare Institutions, Research Entities) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

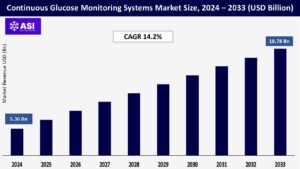

CAGR: 14.2%

Last Updated : August 6, 2025

The global Continuous Glucose Monitoring Systems Market was valued at USD 5.36 billion in 2024 and is projected to reach USD 18.78 billion by 2033, expanding at a compound annual growth rate CAGR of 14.2% during the forecast period (2025 – 2033).

Continuous glucose monitoring systems are breakthrough technological innovation revolutionizing diabetes care through real-time monitoring of glucose levels. These advanced devices use minimally invasive sensors located under the skin to quantify glucose levels in interstitial fluid, sending data wirelessly to receivers or apps on smartphones. In contrast to finger-stick blood glucose testing with multiple daily pokes, continuous glucose monitoring offers uninterrupted monitoring with readings received every five minutes or a minute during the day and night. The technology allows patients and caregivers to detect glucose patterns, forecast hypoglycemia and hyperglycemia events, and fine-tune treatment regimens with unprecedented accuracy.

Contemporary continuous glucose monitors include alarm facilities for life-threatening glucose levels, connectivity to smartphones for data transfer to caregivers, and interfaces with insulin pump systems for algorithmic diabetes control. The market involves diverse technological platforms such as real-time continuous glucose monitoring devices, flash glucose monitoring systems, and implantable sensors for longer wear durations. Modern technologies have stretched into non-traditional diabetes care into wellness applications for use by non-diabetic individuals who are interested in metabolic insights.

The growing global diabetes pandemic is the main driver propelling continuous glucose monitoring systems market growth, with diabetes prevalence increasing to epidemic levels in developed and developing countries. Based on the International Diabetes Federation, about 537 million adults have diabetes worldwide, with a prediction that this number will shoot up to 643 million by 2030 and as many as 783 million by 2045. This exponential growth is due to several interrelated factors such as lifestyles of being physically less active, changes in diet towards more processed foods, urbanization trends, and genetic factors leading to insulin resistance. The aging world population mainly speeds up diabetes incidence, with people over sixty-five years showing a much greater susceptibility to type two diabetes and its complications.

Obesity is another key component, with WHO estimating more than one billion overweight people globally in 2022, including 650 million adults, 340 million young people, and 39 million children. Healthcare providers globally identify continuous glucose monitoring as critical technology for the management of this expanding patient base, resulting in high levels of adoption in hospitals, clinics, and home healthcare environments. Government campaigns encouraging diabetes awareness, early detection initiatives, and preventive strategies also drive demand for advanced monitoring technologies.

Evolving technology for continuous glucose monitoring fuels industry expansion by increasing precision, user friendliness, and easy interoperability with digital health platforms. Advanced sensors exhibit greatly enhanced precision rates, longer wear periods, and lower calibration needs than the previous generation. The synergy between machine learning and artificial intelligence algorithms supports predictive analytics for glycemic fluctuations, individualized treatment advice, and computerized decision support systems. Smartphone connectivity supports the sharing of data in real-time with healthcare providers, family members, and diabetes management apps to enable remote patient monitoring and telemedicine consultations.

Some new developments in recent years involve non-invasive monitoring technology in development, implantable sensors that last for as long as one year, and compatibility with wearables such as smartwatches and fitness bands. Companies are also more commonly working on closed-loop insulin systems that integrate continuous glucose monitoring and automated insulin pumps to develop artificial pancreas technologies that revolutionize diabetes treatment. The availability of over-the-counter continuous glucose monitoring systems cleared for non-diabetic wellness uses broadens market access outside of conventional medical uses. Integration of digital health platforms facilitates integrated diabetes management through medication tracking, meal tracking, exercise tracking, and outcome analytics in integrated ecosystems.

Even where clinical advantages have been shown, high costs of continuous glucose monitoring systems present severe barriers to adoption, especially among underserved populations and in developing economies. Upfront device expenditures are generally higher than those of conventional glucose monitoring devices, while sensor replacement expenditures incur significant long-term charges for patients. Insurance coverage is uneven across various healthcare systems, with numerous payers having restrictive eligibility standards that restrict coverage for individual patient populations or types of diabetes. Medicare and Medicaid programs illustrate disparate coverage policies, with some covering continuous glucose monitoring at all for specific groups, posing access disparities across socioeconomic status and geography. Prior authorization tends to slow down patient access to continuous glucose monitoring systems, involving detailed documentation and multiple steps of approval that deter patients and healthcare professionals.

Regional payment differences generate global market fragmentation across developed nations, which provide wider coverage, and emerging markets, which face affordability issues. Technical sophistication demands specialized education for healthcare workers and patients, increasing the cost of implementation and potential entry barriers in resource-poor environments. Sensor limitations under certain conditions such as hypoglycemia, exercise, or drug interference may require additional conventional glucose testing, lowering cost-effectiveness proposals. Frequent replacements in sensor use create constant medical waste issues contributing towards aggregate expense loads that can discourage patient compliance with continuous monitoring regimens.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Real-time CGM Flash Glucose Monitoring Implantable Sensors Non-invasive Systems (in dev) Pump-Integrated Systems

|

| By Application |

Diabetes Management (Type 1 & 2) Hospital Monitoring Gestational Diabetes Non-diabetic Wellness Research

|

| By End User |

Healthcare Institutions Research Entities

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Continuous glucose monitoring technology has varied platforms that are used to address the different needs of patients and clinical demands in different diabetes management situations. Real-time continuous glucose monitoring systems lead market segments with better performance such as constant data transmission, patient-expandable alarms for threatening glucose levels, and connectivity options with insulin delivery devices. These devices normally offer minute-to-five-minute glucose readings to allow for prompt response to glycemic swings and to avoid severe hypoglycemia or hyperglycemia. Flash glucose monitoring is an alternative method involving active scanning to obtain glucose information, with lower costs and continuing extended sensor wear times up to fourteen days.

Implantable continuous glucose monitoring systems offer longest-term monitoring options with sensor life extending to one year, though in need of minor surgical intervention for implantation and removal. Wearable sensor technology is going further toward reduced-profile sizes, increased adhesion characteristics, and increased user comfort for extended wear durations. Non-invasive monitoring technologies on the horizon have the potential to obviate sensor insertion requirements altogether using optical, microwave, or electromagnetic sensing techniques. Smartphone-integrated systems utilize mobile device functionality for data processing, trend detection, and connectivity with healthcare professionals or family members. Integration with insulin pump technology facilitates automated insulin delivery systems to form closed-loop diabetes management platforms that are the future of continuous glucose monitoring technology progress.

Continuous glucose monitoring applications range across wide ranges of healthcare situations beyond the conventional diabetes management to include new wellness and preventive care uses. Diabetes management represents the primary application segment, serving both type one and type two diabetes patients requiring intensive glucose monitoring for optimal glycemic control. Type one diabetes patients demonstrate highest adoption rates due to insulin dependency and elevated risks of severe hypoglycemic episodes requiring continuous surveillance. Type two diabetes applications increasingly expand as healthcare providers recognize benefits for patients using various treatment regimens including oral medications, lifestyle modifications, and insulin therapy. Hospital inpatient monitoring apps became more popular during healthcare emergencies, allowing for decreased exposure of healthcare professionals while still providing uninterrupted glucose monitoring for critically ill patients.

Gestational diabetes tracking offers specialized use cases for pregnant women who need intensive glucose control to preserve maternal and fetal health endpoints. Non-diabetic wellness apps are new market opportunities targeting healthy individuals who want metabolic data to optimize nutrition, exercise, and lifestyle decisions. Athletic performance monitoring allows sport professionals and fitness participants to learn about glucose responses during exercise and competition for performance optimization. Research uses facilitates clinical trials, biomarker studies, and population health studies needing in-depth glucose pattern analysis in various demographic populations. Preventive care uses addresses prediabetic subjects and those at high-risk diabetes status for early intervention and lifestyle change programs.

Healthcare facilities such as hospitals, specialized diabetes clinics, and endocrinology practices are key end-user segments fueling the adoption of continuous glucose monitoring across clinical care environments. Hospitals more and more use continuous glucose monitoring for inpatient diabetes care, intensive care unit use, and surgical patient monitoring to enhance outcomes while lowering nursing workload related to recurring glucose testing. Endocrinology clinics and diabetes centers are specialized institutions for starting continuous glucose monitoring, educating patients, and sustained management support involving expert-level technical proficiency. Home healthcare is the most rapidly expanding end-user market with patients adopting self-management strategies aided by ease-of-use continuous glucose monitoring technology. Individual patients are major end-user groups yearning for more independence in diabetes care based on real-time glucose information and trend analysis functionalities.

Caregivers such as family members and professional caregivers are advantaged by remote monitoring features providing proactive intervention and assistance for glucose control. Long-term care facilities and assisted living facilities embrace continuous glucose monitoring to improve diabetes care quality and limit staff burden of traditional monitoring methods. Research organizations and pharmaceutical organizations leverage continuous glucose monitoring for clinical trials, drug development research, and biomarker research needing accurate glucose measurement capability. Healthcare payers and insurance firms increasingly identify continuous glucose monitoring worth in mitigating long-term diabetes complications and related healthcare expenditure. Workplace health programs investigate continuous glucose monitoring uses for employee health maximization and diabetes prevention programs.

North America continues to hold market dominance with prevailing share of more than forty percent of global continuous glucose monitoring income, propelled by well-developed healthcare infrastructure and established reimbursement systems.The United States drives regional growth through extensive diabetes prevalence across more than thirty-seven million Americans and strong uptake of new medical technologies. Large ongoing continuous glucose monitoring producers such as Dexcom, Abbott, and Medtronic have dominant presence with robust product lines and expansive distribution channels. Medicare expansion of coverage for continuous glucose monitoring among type two diabetes patients profoundly increases market accessibility and adoption rates. Canadian markets depict high growth prospects through government efforts such as universal coverage for diabetes medicines and specific device funding schemes.

Continuous glucose monitoring markets in Europe depict consistent growth aided by universal healthcare programs and government-backed diabetes management programs in leading economies. Germany, France, and the United Kingdom are lead markets with developed health infrastructure and early stage diabetes technology adoption. National Health Service programs within the United Kingdom encourage access to continuous glucose monitoring for type one diabetes patients and extend coverage consideration to broader patient populations. Regulatory alignment across European Union markets supports streamlined product clearance and market availability of innovative continuous glucose monitoring technologies. Increasing diabetes prevalence and population aging dynamics drive consistent demand for sophisticated glucose monitoring solutions across the region.

Asia Pacific exhibits highest regional growth rates spurred by fast-growing diabetes populations, enhanced healthcare infrastructure, and rising levels of disposable income. China dominates regional markets with world’s largest diabetes population and policies encouraging early diagnosis and sophisticated diabetes management technologies. India symbolizes high-growth emerging market with diabetes population expected to reach more than one hundred million by 2035, presenting high demand for low-cost continuous glucose monitoring options. Japan and South Korea have mature markets with high growth potential fueled by aging populations and innovation in adopting advanced healthcare technology. Healthcare investment by governments in the region and diabetes prevention programs aid in continuous glucose monitoring market growth.

The Latin America and Middle East Africa regions showcase emerging market potential even though they currently have smaller market shares than developed regions. Brazil, Mexico, and Argentina dominate Latin American markets with increasing diabetes consciousness and expanding healthcare availability providing platforms for the adoption of continuous glucose monitoring. Middle Eastern countries such as Saudi Arabia and United Arab Emirates invest significantly in the modernization of healthcare and diabetes care infrastructure. African markets are plagued by limited healthcare infrastructure and budget issues, although mounting international cooperation facilitates incremental technology adoption. Government programs of diabetes education and healthcare system development are part of long-term market development opportunities in these markets.

The global Continuous Glucose Monitoring Market was valued at USD 5.36 billion in 2024.

The market is projected to grow at a CAGR of 14.2 % from 2025 to 2033.

Real time CGM hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Abbott, Dexcom, Medtronic, Senseonics, SIBIONICS

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Continuous Glucose Monitoring Systems Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Continuous Glucose Monitoring Systems Market, By Application

5.3 Continuous Glucose Monitoring Systems Market, By End User

6.1 North America Continuous Glucose Monitoring Systems Market, By Country

6.1.1 Continuous Glucose Monitoring Systems Market, By Technology

6.1.2 Continuous Glucose Monitoring Systems Market, By Application

6.1.3 Continuous Glucose Monitoring Systems Market, By End User

6.2 U.S.

6.2.1 Continuous Glucose Monitoring Systems Market, By Technology

6.2.2 Continuous Glucose Monitoring Systems Market, By Application

6.2.3 Continuous Glucose Monitoring Systems Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping