Defibrillator Market

Defibrillator Market By Product Type (Implantable Cardioverter Defibrillators, External Defibrillators) By End User (Hospitals & Clinics, Pre-hospital Care Settings, Public Access Settings, Homecare, Others) By Technology (Semi-Automatic Defibrillators, Fully Automatic Defibrillators) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

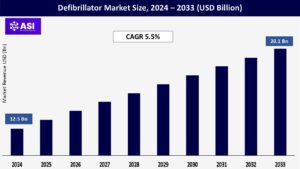

CAGR: 5.5%

Last Updated : November 8, 2025

The global Defibrillator Market size was valued at approximately USD 12.5 billion in 2024 and is projected to reach USD 20.1 billion by 2033, growing at a CAGR of 5.5% during the forecast period (2025–2033).

Defibrillators are life-saving devices that aim to return normal function to the heart of someone that is having sudden cardiac arrest (SCA). The defibrillator device attempts to restore a functional heartbeat either automatically, or as determined by a medical responder, by sending a controlled electric shock to the heart. Defibrillator products can include implantable cardioverter defibrillators (ICDs), automated external defibrillators (AEDs), and wearable defibrillator devices. Growth in the global defibrillator market is anticipated due to factors including: the increasing incidence of cardiac arrhythmias; development of new technologies in the defibrillator category; increase in public access defibrillation programs; and increase in knowledge about emergency cardiovascular care. In addition to these key drivers of growth, supportive government policies and increasing access to defibrillators in the community and home are fuelling global demand.

The increasing global rate of sudden cardiac arrest (SCA) primarily defined as a sudden cessation of the heart’s function, is raising demand for defibrillators around the world. The American Heart Association (AHA) states there are more than 356,000 out-of-hospital cardiac arrests (OHCAs) every year in the United States alone, with less than a 10% survival rate without immediate intervention.

Having access to an automated external defibrillator (AED) can increase a victim’s chance of survival by as much as 70% if administered within the first few minutes of the cardiac arrest. Government and health organizations across the world are working to implement public access defibrillation (PAD) programs in an effort to reduce sudden death due to cardiac arrest.

For example, in April 2024, the UK Department of Health and Social Care mandated every state-funded school install AEDs and implemented an awareness campaign to jan staff of the schools children of their use.

Similarly, Japan has strategically placed AEDs in train stations and shopping malls in order to improve the response time in cardiac events. As countries create further similar models or implement defibrillator accessibility to their emergency preparedness policies, the global AED segment is primed to explode as there are increasing installations in public spaces including airports, office buildings, and sports arenas.

Advances in defibrillator technology continue to make an impact on patient safety and treatment options, as well as providing opportunities for new market growth in the defibrillator sector. Patient safety is certainly motivated by advances in technology as well as regulatory approval for next generation defibrillators, which are outfitted with greater capabilities than ever before – including real-time ECG monitoring, connectivity to other wireless devices, vocal prompts, automated rhythm detection, and automatic shock features, thus making them much easier for clinical professionals and laypersons to use.

One of the areas where we have seen innovations come to fruition is in wearable cardioverter defibrillators (WCDs), which provide continuous heart rhythm monitoring along with a discharge shock in a life-threatening event. WCDs represent additional protection for patients with a high risk of sudden cardiac death (SCD) with an exclusion period until an implantable system is accepted (e.g., recently diagnosed myocardial infarction or infection).

In February 2024, ZOLL Medical Corporation launched the new version of its LifeVest (WCD) with improvements for wearability and intelligent, machine-learning arrhythmia detection. In late 2023, Medtronic unveiled its Aurora EX single-lead subcutaneous modern ICD that offers longer battery life and wireless programming features approved by the FDA.

These and similar innovations will increase overall patient safety and quality of life as well as improve existing rates of defibrillation where resuscitation is possible, while also increasing the adoption of defibrillators in hospitals and homes. In addition, foreshadowed growth in the defibrillator market will be driven by increasing demands for remote monitoring options that integrate with tele-health platforms.

One of the major restraints in the defibrillator market is the high cost associated with advanced defibrillator devices, particularly implantable cardioverter defibrillators (ICDs) and wearable cardioverter defibrillators (WCDs). These devices often require not only substantial upfront investment but also ongoing expenses related to maintenance, battery replacements, surgical implantation, and follow-up care.

For instance, the average cost of an ICD implantation in the U.S. can exceed USD 30,000, making it unaffordable for many patients without comprehensive health insurance. In low- and middle-income countries, limited healthcare budgets, inadequate reimbursement policies, and lack of trained professionals further restrict the adoption of defibrillators.

Public access defibrillation programs, which are critical for improving survival rates in sudden cardiac arrest, are also underdeveloped in many regions due to financial constraints. This cost barrier hinders widespread deployment of AEDs in schools, rural areas, and public spaces—severely impacting emergency response capabilities and slowing overall market penetration in emerging economies.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Implantable Cardioverter Defibrillators External Defibrillators |

| By End User |

Hospitals & Clinics Pre-hospital Care Settings Public Access Settings Homecare Others |

| By Technology |

Semi-Automatic Defibrillators Fully Automatic Defibrillators |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The defibrillator Market share is segmented by product type, end user, and technology. Each segment contributes uniquely to enhancing emergency response, cardiac care, and long-term arrhythmia management across different healthcare settings.

The Implantable Cardioverter Defibrillators (ICDs) segment is projected to remain the largest defibrillator market share of 43.1% in 2024, largely due to the increasing prevalence of life-threatening arrhythmias and sudden cardiac arrest (SCA). In the Implantable segment, Transvenous ICDs (TV-ICD) are the most widely used instrument because of their effectiveness in long-term rhythm correction and familiarity in practice.

The Subcutaneous ICDs (S-ICDs) are beginning to gain momentum due to their minimally invasive designs and fewer vascular complications for younger or higher risk patients. Driven by the presence of Automated External Defibrillators (AED) being installed in public places, the External Defibrillators segment is expected to grow rapidly.

AEDs are becoming a community resource for public access defibrillation (PAD), with many groups making them accessible in various settings such as communities, workplaces, schools, and transportation hubs. Wearable Cardioverter Defibrillators (WCDs) are also presenting significant possibilities for patients who are temporarily disqualified from implantable ICDs, since they offer real time monitoring and immediate shock delivery, without needing surgical implantation.

Hospitals & Clinics hold market dominance in the defibrillator market with over 58% of the total share in global market revenue in 2024 because hospitals are the primary sites for patients experiencing cardiac emergencies, are the site of ICD implantations, and most advanced electrophysiology patients.

Hospitals are the best-equipped sites for the use of implantable and external defibrillators as they have trained personnel available and sophisticated monitoring systems. In the Pre-hospital Care Settings (EMS) segment, portable AEDs and manual defibrillators are increasingly used to help improve rates of a survival from out-of-hospital cardiac arrest (OHCA). Rapid response teams and ambulances are good drivers of this segment.

The Public Access Settings segment is growing quite steadily, which can be attributed to government initiatives, well-researched public awareness campaigns, and introduced regulations encouraging the installation of public access AEDs in malls, stadiums, airports and academic institutions. The Homecare segment is growing as well because patients with chronic heart conditions who are being monitored at home with a wearable defibrillator (e.g. WCD) or consumer level AED’s – especially population at risk including the elderly or post-operative.

Semi-Automatic Defibrillators have a large share of the market because they are used in a professional environment with trainers who can use it as intended. In a semi-automatic mode, rhythm analysed before applying a shock. Fully Automatic Defibrillators are growing in popularity especially in locations with public access and home defibrillators, due to ease of use, voice-guided instructions in real-time, and a device that applies shock delivery automatically. They are vital to increasing bystander effectiveness in emergencies.

North America is forecasted to have the largest defibrillator market share of 41.2% in 2024 due to the large number of cases of sudden cardiac arrest (SCA) in individuals, favorable reimbursement policies, and the great number of highly developed healthcare systems within the region.

The United States will drive market growth from strong national initiatives aimed at making public access defibrillation a standard of care, with extensive deployment of automated external defibrillators (AEDs) in schools, airports, and corporate buildings, and also the increasing number of implantable cardioverter defibrillators (ICDs) being used in general patient care. Technological innovations from major players such as Medtronic, Boston Scientific, and ZOLL will also strengthen the adoption of defibrillation in the region.

Europe occupies a large portion of the market, especially countries with higher cardiovascular mortality rates such as Germany, France, UK, Netherlands, and Sweden. The European Society of Cardiology states that over four million deaths per year in Europe are caused by a cardiovascular disease. The adoption rates of ICDs and AEDs have been supported systematically through emergency medical services and awareness campaigns.

In addition, the EU has strong policies aimed at increasing the number of AEDs in public spaces, and health programs at the national level managing heart disease, which are contributing to steady market growth. The aging population along with the demand for wearable and home-based defibrillators are additionally driving growth.

The Asia Pacific region is projected to exhibit the highest growth rate with a forecast CAGR of 7.9%, largely supported by the rapid improvement of healthcare infrastructure, growing awareness of cardiac health, and increased investment into emergency medical services.

Countries such as China, India, Japan, and South Korea will continue to drive regional growth as these countries have high population density, booming urbanization rates, and high rates of cardiovascular disease. India alone reports over 700,000 sudden cardiac deaths annually, demonstrating the pressing need for easier access to defibrillators. The government of India has initiated programs that place AEDs in transport hubs, along with demand for cost-effective AEDs propelling growth.

Latin America and Middle East & Africa are seeing moderate growth, with improving access to emergency care assistance and increased government and non-government funding towards healthcare infrastructure. In Latin America, countries such as Brazil, Mexico and Argentina are also becoming increasingly interested in distributing AEDs in community health and urbanized areas.

Countries in the Middle East & Africa, like Saudi Arabia, UAE, and South Africa, are expanding the capacity of hospitals, and funding cardiac emergency equipment where possible in ambulances and clinics. However, there are a range of challenges limiting defibrillator market potential in some regions – limited budgets for healthcare, socio-economical disparities, and low public awareness are a few nuances still to be addressed.

The defibrillator market was valued at USD 12.5 billion in 2024.

The defibrillator market is projected to grow at a CAGR of 5.5% from 2025 to 2033.

The Implantable Cardioverter Defibrillator hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Medtronic plc, Boston Scientific Corporation and ZOLL Medical Corporation

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Defibrillator Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Defibrillator Market, By End User

5.3 Defibrillator Market, By Technology

6.1 North America The Defibrillator Market, By Country

6.1.1 Defibrillator Market, By Product Type

6.1.2 Defibrillator Market, By End User

6.1.3 Defibrillator Market, By Technology

6.2 U.S.

6.2.1 Defibrillator Market, By Product Type

6.2.2 Defibrillator Market, By End User

6.2.3 Defibrillator Market, By Technology

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping