Dementia Drugs Market

Dementia Drugs Market Share & Trends Analysis Report, By Indication Type (Alzheimer’s Disease Dementia, Vascular Dementia, Lewy Body Dementia (LBD), Parkinson’s Disease Dementia (PDD), Frontotemporal Dementia (FTD), Other Indications), By Drug Class (Cholinesterase Inhibitors, NMDA Receptor Antagonists (Glutamate Inhibitors), Combination Drugs, MAO Inhibitors (MAO-B Inhibitors), Disease-Modifying Therapies (DMTs), Others), By Route of Administration (Oral, Injectable, Transdermal Patch), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies)

– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 6.9%

Last Updated : December 16, 2025

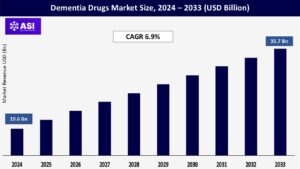

The worldwide market for Dementia Drugs Market was valued at approximately USD 19.6 billion in 2024 and is projected to reach USD 35.7 billion by 2033, demonstrating a compound annual growth rate (CAGR) of 6.9% during the forecast period of 2025–2033.

The dementia drugs market is set to witness significant growth from 2025 to 2033, driven by the increasing global prevalence of dementia and a rapidly aging population. As the number of affected individuals continues to rise, there is a growing urgency for more effective treatment options. The market is moving beyond symptom management, with a strong push toward disease-modifying therapies and personalized medicine that cater to individual patient needs. At the same time, the integration of digital health solutions—such as remote monitoring tools and AI-driven diagnostics—is enhancing patient care and treatment efficiency. This progress is being further accelerated by increased collaboration among pharmaceutical companies, academic researchers, and governments, all working together to bring innovative, accessible, and impactful solutions to those living with dementia.

The steady rise in global life expectancy, fueled by advancements in healthcare, improved nutrition, and better living conditions, is significantly altering population demographics. As more people reach the age of 65 and above, dementia cases particularly Alzheimer’s disease are increasing at an alarming rate. Since aging is the primary risk factor for most forms of dementia, this demographic shift directly correlates with a growing patient population worldwide. The numbers paint a stark picture: dementia cases are expected to double every 20 years, reaching approximately 82 million by 2030 and soaring to 152 million by 2050.

This rapid escalation is placing an immense strain on individuals, families, and healthcare systems alike. To address this mounting challenge, there is a growing demand for effective diagnostic tools, symptomatic treatments, and most importantly, disease-modifying therapies that can slow disease progression. As dementia becomes an increasingly urgent global health concern, medical research, policy initiatives, and healthcare infrastructure must evolve to support the expanding patient population and mitigate the long-term impact on societies worldwide.

For years, dementia treatment has largely focused on managing symptoms, offering patients relief but not addressing the underlying progression of the disease. However, groundbreaking research into the biological mechanisms of dementia such as the role of amyloid plaques and tau tangles in Alzheimer’s has paved the way for new therapeutic approaches. The approval of disease-modifying therapies (DMTs) like lecanemab (Leqembi) and donanemab (Kisunla) marks a major shift, as these drugs aim to slow or even halt disease progression rather than simply ease symptoms.

This progress extends beyond these recent approvals. A diverse pipeline of potential dementia treatments is currently in development, with growing interest in Disease-Targeted Therapies (DTTs), personalized medicine, and new areas of research, such as neuroinflammation and synaptic dysfunction. With multiple promising drug candidates in clinical trials, the future of dementia treatment is evolving rapidly. The impact of these advancements is profound. The introduction of therapies that can change the disease course is reshaping the market, attracting major investment and opening new revenue opportunities.

While these treatments can be expensive, their ability to slow cognitive decline provides a strong value proposition for patients, caregivers, and healthcare systems alike. Additionally, cutting-edge technologies including genomics, neuroimaging, and biomarker analysis are accelerating drug discovery and development, making it possible to refine treatments and improve patient outcomes. With continued research and innovation, the dementia drug market is set for transformative growth, bringing new hope to those affected by these challenging conditions.

The arrival of disease-modifying therapies (DMTs) for dementia, particularly Alzheimer’s treatments like lecanemab and donanemab, represents a major breakthrough in neurology. Unlike traditional medications that only manage symptoms, these therapies aim to slow or halt disease progression, offering hope to millions affected by cognitive decline. However, this innovation comes at a high financial cost, with annual treatment expenses reaching tens of thousands of dollars per patient. Such hefty price tags create a significant financial burden on healthcare systems, insurance providers, and individual patients. Many health authorities and insurers carefully evaluate whether these drugs provide enough benefit to justify their steep costs.

As a result, reimbursement challenges often arise, leading to restricted access, limited coverage, and slow adoption especially in countries with budget-constrained healthcare systems. A striking example of this issue was seen with NICE’s initial rejection of donanemab in the UK, where cost-effectiveness concerns prevented swift approval. This highlights a broader challenge: even highly effective treatments may struggle to reach patients if funding and reimbursement policies are too restrictive. The future of DMT accessibility will depend on efforts to balance innovation with affordability, ensuring that groundbreaking therapies can make a meaningful impact on global dementia care.

Most dementia treatments available today, such as cholinesterase inhibitors and NMDA receptor antagonists, primarily focus on managing symptoms rather than addressing the underlying neurodegeneration. While these medications can help improve cognitive function and alleviate behavioral symptoms, their effects are temporary, and they do not stop or reverse disease progression.

Even the newer disease-modifying therapies (DMTs) for Alzheimer’s—such as lecanemab and donanemab have shown statistically significant slowing of cognitive decline, but they are not a cure and cannot fully halt the disease.

This limitation in treatment options affects both patient and healthcare provider perceptions. Many individuals experience treatment fatigue, as the available drugs offer only modest benefits, often requiring long-term adherence without delivering dramatic improvements. Additionally, the high costs and potential side effects of newer therapies can lead to hesitation in adopting these treatments, particularly when the clinical benefits remain incremental rather than transformative. As a result, some patients and caregivers may struggle with the decision to continue treatment, weighing the financial burden, possible side effects, and uncertain long-term benefits.

Healthcare providers also face challenges in justifying these medications, especially in systems where cost-effectiveness evaluations influence access and reimbursement decisions. Despite these concerns, continued research and innovation in dementia treatment, including biomarker-based therapies, personalized medicine, and new drug targets, offers hope for more effective solutions in the future. As scientific understanding deepens, the focus remains on developing treatments that go beyond symptom management to truly alter the course of the disease.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Indication Type |

Alzheimer’s Disease Dementia Vascular Dementia Lewy Body Dementia (LBD) Parkinson’s Disease Dementia (PDD) Frontotemporal Dementia (FTD) Other Indications |

| By Drug Class |

Cholinesterase Inhibitors NMDA Receptor Antagonists (Glutamate Inhibitors) Combination Drugs MAO Inhibitors (MAO-B Inhibitors) Disease-Modifying Therapies (DMTs) Others |

| By Route of administration |

Oral Injectable Transdermal Patch |

| By Distribution Channel |

Hospital Pharmacies Retail Pharmacies Online Pharmacies |

| Key Players |

AbbVie Inc. Alector Inc. Apotex Inc. AstraZeneca PLC Aurobindo Pharma Ltd. Biogen Inc. Bristol-Myers Squibb Company Cipla Ltd. Cognition Therapeutics Corium Inc. Daiichi Sankyo Company, Limited Dr. Reddy’s Laboratories Ltd. Eisai Co., Ltd. Eli Lilly and Company F. Hoffmann-La Roche AG (Roche) GlaxoSmithKline plc (GSK) Grifols, S.A. H. Lundbeck A/S Johnson & Johnson (Janssen Pharmaceutical) Lupin Limited Merck & Co., Inc. Merz Pharma GmbH & Co. KGaA Neurim Pharmaceuticals Ltd. Novartis AG Novo Nordisk A/S Otsuka Pharmaceutical Co., Ltd. Pfizer Inc. Sanofi S.A. Sun Pharmaceutical Industries Ltd. Takeda Pharmaceutical Company Limited TauRx Pharmaceuticals Ltd. Teva Pharmaceutical Industries Ltd. Torrent Pharmaceuticals Ltd. Zydus Cadila (Zydus Lifesciences Limited)

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Dementia Drugs Market is categorized by indication type, by drug class, by route of administration and by distribution channel. Each segment is rapidly evolving, with different areas of the industry growing at their own pace and shifting in how much of the market they represent. Each segment provide a comprehensive understanding of its dynamics and growth opportunities. The Dementia Drugs Market is broadly segmented to provide a comprehensive understanding of its various facets and dynamics.

This part of the market is divided based on the specific type of dementia being treated, each with its own unique characteristics and treatment needs. Alzheimer’s disease dementia dominates the market, as it’s the most common form accounting for 60–70% of all dementia cases. The approval of new disease-modifying therapies like lecanemab (Leqembi) and donanemab (Kisunla) for early-stage Alzheimer’s is creating fresh momentum in this space. Vascular dementia follows as the second-largest segment, caused by reduced blood flow to the brain often after strokes and is attracting increasing attention as researchers look to address its root causes.

Lewy body dementia (LBD), marked by abnormal protein deposits in the brain, is emerging as a fast-growing segment due to its complex blend of cognitive and motor symptoms. Parkinson’s disease dementia (PDD) affects individuals who already have Parkinson’s, while frontotemporal dementia (FTD) though less common targets the brain’s frontal and temporal lobes, often affecting behavior and language. The “other” category includes rarer or less clearly defined forms of dementia, which also contribute to the market’s growing diversity and demand for tailored treatment approaches.

This part of the market is categorized by the different types of drugs used to treat dementia, each targeting specific symptoms or underlying causes. Cholinesterase inhibitors are currently the most widely used, especially for mild to moderate Alzheimer’s, as well as in Lewy body and Parkinson’s-related dementias. These drugs like Donepezil, Rivastigmine, and Galantamine work by boosting levels of acetylcholine in the brain, a chemical important for memory and learning. Thanks to their proven effectiveness and long-standing use, this category holds the largest market share. NMDA receptor antagonists, such as Memantine, are commonly used for moderate to severe stages of Alzheimer’s. They help protect brain cells by regulating glutamate, a chemical that, in excess, can damage neurons.

Combination therapies, which blend cholinesterase inhibitors with NMDA antagonists (like Donepezil with Memantine), are becoming increasingly popular. These offer more comprehensive symptom control and are helping to expand this segment quickly. MAO-B inhibitors, often used in Parkinson’s disease dementia, work by preserving dopamine levels in the brain and can help manage both cognitive and motor symptoms. Perhaps the most exciting area is disease-modifying therapies (DMTs), which aim to actually change the course of the disease, not just manage symptoms.

These include new treatments like lecanemab and donanemab, which target amyloid plaques in the brain and are specifically designed for Alzheimer’s. This rapidly growing segment is expected to play a major role in shaping the future of dementia treatment. The “Others” category includes emerging drug types some repurposed from other conditions and others targeting newer areas like neuroinflammation and tau proteins that are still under research but show promise for expanding treatment options down the line.

When it comes to delivering medications to patients, different methods cater to varying needs and preferences. Oral administration remains the most popular choice, largely due to its convenience, ease of use, and the wide availability of tablets, capsules, and liquid formulations. Many patients prefer this approach since it requires minimal effort and is generally well-tolerated. On the other hand, injectable medications are experiencing rapid growth, particularly with the rise of biological disease-modifying therapies such as monoclonal antibodies. These treatments often require intravenous or subcutaneous injections, making them essential for certain conditions.

Advances in medical technology, including the development of user-friendly autoinjectors, are further driving the demand for injectables by enhancing accessibility and ease of administration. For patients who find it difficult to swallow pills, transdermal patches present an effective alternative. These patches deliver medication steadily through the skin, ensuring continuous drug absorption over time. Certain formulations, such as those used for rivastigmine, demonstrate the advantages of this method in providing consistent therapeutic effects while eliminating the challenges associated with oral medication intake. Each delivery method offers distinct benefits tailored to different medical conditions and patient needs, contributing to an evolving landscape of drug administration.

Medications for dementia are dispensed through various channels, each serving distinct patient needs and preferences. Hospital pharmacies currently dominate the market, as hospitals are often where dementia is first diagnosed and treatment plans are initiated. Patients admitted for care or those receiving specialized therapies frequently rely on hospital pharmacies for their prescriptions, ensuring access to the latest and most advanced treatments. Meanwhile, retail pharmacies, including local community drugstores, play a crucial role in long-term dementia management. Patients or caregivers can easily fill prescriptions here, providing convenience and continuity for ongoing treatment. These pharmacies offer accessibility, allowing individuals to receive their medication without requiring hospital visits.

The rise of online pharmacies is reshaping the way medications are obtained. With increasing digitalization, patients and caregivers can now order dementia drugs from the comfort of home. This segment is growing rapidly due to its convenience, potential cost savings, and access to a wider range of medications, making it an appealing option for many looking for an easier way to manage their healthcare needs. Each of these distribution channels caters to specific circumstances, ensuring patients receive their medication in the most suitable and accessible manner.

The Dementia Drugs Market is shaped by regional differences, each influencing market growth in distinct ways. North America leads the charge with advanced healthcare infrastructure, strong investment in research, and a growing elderly population fueling demand for effective treatments. Meanwhile, Europe follows closely, benefiting from widespread government support and an emphasis on innovative neurological research. In the Asia-Pacific region, market expansion is accelerating due to rising awareness, an increasing aging demographic, and improved healthcare access across countries like Japan, China, and India. Similarly, Latin America is experiencing gradual growth, driven by healthcare advancements and the broader adoption of dementia treatment protocols.

In contrast, the Middle East & Africa region faces unique challenges, such as limited access to specialized healthcare and varying levels of awareness about dementia. However, ongoing efforts to strengthen healthcare infrastructure and introduce newer treatment options signal potential for future growth.

North America, particularly the United States, is set to remain the dominant force in the global dementia drugs market, with projections suggesting it could hold around 38.3% of the market share by 2025. This leadership is driven by a combination of demographic, healthcare, and regulatory factors that foster innovation and accessibility. One of the key drivers is the high prevalence of dementia, especially Alzheimer’s disease, due to the rapidly aging population. With more individuals entering the age range most vulnerable to cognitive decline, the demand for effective treatments continues to grow.

Supporting this is the advanced healthcare infrastructure, which includes specialized memory clinics, cutting-edge diagnostic tools like PET scans and cerebrospinal fluid biomarker testing, and top-tier research institutions working on innovative therapies. Another crucial factor is high healthcare expenditure, allowing both private and public sectors to invest in expensive but potentially groundbreaking treatments, including the latest disease-modifying drugs. This is reinforced by strong R&D investment, fueled by major pharmaceutical and biotech companies such as Biogen, Eli Lilly, and Pfizer, which are driving forward new drug development and clinical trials.

The favorable regulatory environment in the U.S. is also a significant contributor, with agencies like the FDA offering accelerated approval pathways for serious conditions, enabling quicker access to novel treatments. Additionally, high awareness and patient advocacy groups are actively involved in promoting early diagnosis, raising public knowledge, and pushing for better access to therapies. Looking ahead, the market is expected to focus on disease-modifying treatments, with an increasing reliance on biomarkers to tailor treatments for individual patients. The potential for personalized medicine is becoming more apparent, paving the way for more targeted and effective dementia care. With all these factors in place, North America’s position in the dementia drugs market is strong, ensuring continued advancements in treatment options for those affected by this challenging condition.

Europe holds a significant share of the global dementia drugs market, supported by its large aging population and well-established healthcare systems. As many European nations experience rapid demographic shifts, the increasing prevalence of dementia is driving demand for effective treatments. The region benefits from universal healthcare coverage, which ensures broad access to approved therapies, though the process of making new treatments widely available can sometimes be slower than in other markets. Additionally, academic institutions and pharmaceutical companies across Europe are deeply involved in dementia research, contributing to advancements in diagnostics, treatment approaches, and clinical trials.

Government initiatives also play a key role, with various national dementia strategies and increased funding aimed at improving care and research efforts. However, challenges remain—reimbursement hurdles make it difficult for expensive new therapies to gain widespread approval, as health technology assessment (HTA) bodies carefully evaluate cost-effectiveness. A recent example is the provisional rejection of donanemab by NICE in the UK in October 2024, highlighting the complexities of regulatory and reimbursement processes. Despite these challenges, Europe is focusing heavily on early diagnosis, with efforts expanding across multiple countries to promote early intervention and improve patient outcomes. However, the market varies significantly between nations due to differing healthcare policies, reimbursement models, and disease prevalence, which adds complexity to drug distribution and access.

Overall, Europe’s dementia drugs market is shaped by a strong research foundation, supportive government policies, and an evolving approach to early diagnosis and treatment accessibility. These factors will continue to influence market trends in the years ahead.

The Asia-Pacific region is emerging as the fastest-growing market for dementia drugs, driven by several key factors that are reshaping the landscape of dementia care. With rapidly aging populations in countries like China, Japan, South Korea, and India, the number of dementia cases is rising dramatically, increasing the demand for effective treatments. Public understanding of dementia and mental health is also evolving, leading to higher diagnosis rates and a growing demand for medical interventions. At the same time, significant investments in healthcare infrastructure and rising disposable incomes are making advanced medical treatments more accessible, allowing more patients to seek specialized care.

Historically, access to cutting-edge dementia treatments has been limited in some parts of the region, creating a large unmet need that emerging therapies aim to address. Government involvement is playing a crucial role, with initiatives to improve dementia care, fund research, and build healthcare support systems. Additionally, domestic pharmaceutical companies particularly in China and India are making substantial contributions by producing affordable generic medications, helping drive accessibility and affordability.

Despite these advancements, challenges remain. The high cost of novel therapies often creates financial barriers for patients, pushing demand for more cost-effective alternatives. There is also a diagnostic gap, as advanced tools like brain imaging and biomarker tests are often concentrated in major cities, making access more difficult for rural populations. Beyond infrastructure concerns, cultural stigma around dementia can delay diagnosis and treatment, preventing some individuals from seeking the help they need.

As the Asia-Pacific region continues to evolve in dementia drug development and distribution, efforts to bridge affordability, expand diagnostic capabilities, and reduce stigma will be key to unlocking the market’s full potential. With these changes, access to innovative treatments is expected to improve, offering hope for better dementia care across the region.

The Middle East & Africa (MEA) region is a smaller but steadily growing market for dementia drugs, shaped by evolving healthcare landscapes and demographic shifts. One of the biggest driving forces behind this growth is the aging population, as more elderly individuals contribute to a rising number of dementia cases. In the Middle East, particularly in countries within the Gulf Cooperation Council (GCC), significant investments in healthcare infrastructure and advanced medical technologies are improving access to dementia treatments.

These nations are increasingly adopting innovative diagnostic tools and therapeutic approaches, helping shape the region’s medical capabilities. Meanwhile, efforts by governments and healthcare organizations to raise awareness about neurological disorders are encouraging earlier detection and intervention, ensuring that more patients receive the care they need. Despite these advancements, several challenges persist. There are significant disparities in healthcare access, with well-developed systems in parts of the Middle East, such as the UAE and Saudi Arabia, contrasting sharply with more limited resources available in many African countries. This creates gaps in treatment availability and diagnostic capabilities across different areas.

Additionally, affordability remains a major concern, as the high cost of dementia drugs coupled with limited healthcare budgets in African nations restrict widespread adoption and access to new therapies. Another obstacle is the lack of comprehensive epidemiological data, making it difficult to accurately assess dementia prevalence and track treatment outcomes in certain parts of the region. With ongoing efforts to improve data collection and healthcare accessibility, MEA’s dementia drug market has the potential to expand further, especially as governments focus on building stronger healthcare frameworks and addressing these systemic challenges.

The dementia drugs market was valued at USD 19.6 billion in 2024.

The dementia drugs market is projected to grow at a CAGR of 6.9% from 2025 to 2033.

Alzheimer’s Disease Dementia segment holds the largest market share of dementia drugs.

Asia-Pacific region is expected to witness the highest growth rate.

Major players include Eli Lilly, Biogen, Novartis, Eisai, Johnson & Johnson, and H. Lundbeck..

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Dementia Drugs Market, By Indication Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Dementia Drugs Market, By Drug Class

5.3 Dementia Drugs Market, By Route of Administration

5.4 Dementia Drugs Market, By Distribution Channel

6.1 North America Dementia Drugs Market, By Country

6.1.1 Dementia Drugs Market, By Indication Type

6.1.2 Dementia Drugs Market, By Drug Class

6.1.3 Dementia Drugs Market, By Route of Administration

6.1.4 Dementia Drugs Market, By Distribution Channel

6.2 U.S.

6.2.1 Dementia Drugs Market , By Indication Type

6.2.2 Dementia Drugs Market , By Drug Class

6.2.3 Dementia Drugs Market , By Route of Administration

6.2.4 Dementia Drugs Market, By Distribution Channel

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping