Dermatology Devices Market

Dermatology Devices Market Share and Trend Analysis, By Technology (Laser Systems, Cryotherapy Devices, Microdermabrasion Equipment, Imaging Devices, Light Therapy Devices), By Application (Skin Cancer Diagnosis, Hair Removal, Tattoo Removal, Psoriasis Management, Acne Therapy, Anti-Aging Interventions), By End User (Hospitals, Dermatology Clinics, Home Care Settings) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

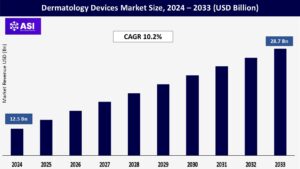

CAGR: 10.2%

Last Updated : February 25, 2026

The global Dermatology Devices Market was valued at USD 12.5 billion in 2024 and is projected to reach USD 28.7 billion by 2033, expanding at a compound annual growth rate CAGR of 10.2% during the forecast period (2025 – 2033).

Dermatology devices represent a complex set of medical equipment and technology tailored to the diagnosis, surveillance, and treatment of skin disorders and beauty treatments. This dynamic market plays an essential role for both clinical dermatology and aesthetic medicine.

Products include laser- and light-based devices for hair removal, tattoo removal, vascular lesion ablation, and skin rejuvenation; diagnostic imaging equipment, such as dermatoscopes and reflectance confocal microscopes, for the identification of skin cancer; biopsy tools; microdermabrasion devices; and light therapy machines for conditions such as psoriasis and acne. Their uses are extensive, addressing increasing global issues such as skin cancer cases driven by UV radiation and aging populations, treating chronic dermatological diseases (eczema, rosacea), and meeting the growing consumer demand for non-surgical cosmetic treatments for anti-aging, scar revision, and body contouring.

Growth is actually driven by rising awareness of skin health, the increasing incidence of skin disease worldwide, improvements in technology to provide safer and more effective treatment with less downtime, and an escalating focus on early diagnosis and minimally invasive treatments. The use of artificial intelligence for image analysis and the creation of portable, user-friendly devices further define the market, increasing accessibility and accuracy both in professional clinical environments and nascent home-care markets. This fusion of medical need and beauty preference consolidates the market’s integral position within contemporary health care.

The rising global skin cancer and chronic inflammatory disease burden continues as a core growth driver. Intensifying environmental stressors – such as chronic ultraviolet light exposure, air pollutants, and occupational exposures – synergistically fuel skin cancer risk in diverse populations. In parallel, autoimmune and genetic dermatoses continue to have high prevalence, driving ongoing clinical need for diagnostic and therapeutic options. This epidemiologic climate forces healthcare systems to emphasize early detection practices, rushing the implementation of high-resolution imaging technologies and non-invasive biopsy machines.

Public health programs expanding skin cancer consciousness even more deeply integrates screening programs, integrating sophisticated devices into routine care pathways. At the same time, therapeutic advances increasingly promote minimally invasive techniques such as targeted phototherapy and laser systems with greater patient compliance and fewer systemic side effects than traditional pharmacotherapies. This paradigm shift towards precision dermatology enables clinicians to treat complicated conditions more effectively while lowering hospital resource utilization. Demographic aging, environmental decline, and clinical preference for device-based treatments create a reinforcing cycle of increasing market growth in diagnostic, therapeutic, and preventive markets.

The pace of innovation in energy-based systems is progressively transforming aesthetic medicine’s efficacy and accessibility. Next-generation laser platforms now provide unprecedented selectivity in targeting pigmentation, vascular lesions, and subdermal tissue with minimal collateral damage – a step that makes treating darker skin tones and delicate areas safer. This technical advancement, combined with dramatically reduced recovery periods, converts cosmetic treatments from elective indulgences into accessible maintenance routines for the masses. Artificial intelligence now enhances treatment planning via predictive skin response modeling and real-time device calibration, taking results above practitioner variables.

Simultaneously, consumerization of professional technologies upends established delivery models; small, user-friendly devices approved for home use give patients in-office cosmetic upkeep between sessions. Cultural acceptance of aesthetic enhancement, amplified by visual social media, erases adoption hurdles while broadening indications past aging into preventive skin optimization. Manufacturers cleverly integrate functions into multi-platform workstation systems that can provide personalized combination treatments (for example, laser ablation with radiofrequency tightening), thus boosting clinic throughput and patient return on investment. This synergy of greater safety, democratized availability, and diversified uses drives strong cross-generational demand.

The hefty price tag associated with advanced dermatology technology is a major inhibitor of market growth. State-of-the-art laser systems, imaging technologies, and energy-based platforms require significant capital investment that is in many ways inaccessible to smaller clinics and healthcare establishments in price-sensitive markets. That economic barrier is added to by complex regulatory environments for medical devices. Companies must endure lengthy approval in varied jurisdictions, with high levels of clinical verification necessary and changing compliance standards slowing the launch of products. These bottlenecks in regulation not only raise the cost of development but also dampen cycles of innovation as firms divert funds towards documentation and testing. Besides, variable insurance reimbursement policies further limit adoption.

Most elective and aesthetic procedures enjoy little or no coverage, leaving patients to pay full costs and dampen demand. Fragmented healthcare infrastructures and inadequate training in emerging economies enhance operation risks, causing available equipment to be underutilized. Concern for safety due to improper use of the device—especially among products intended for home use—also discourages consumer confidence. Combined with the existence of counterfeit devices in unregulated markets, these issues present a difficult landscape for sustainable development, especially outside highly developed medical centers where buying power and regulation are still scarce.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Laser Systems Cryotherapy Devices Microdermabrasion Equipment Imaging Devices Light Therapy Devices

|

| By Application |

Skin Cancer Diagnosis Hair Removal Tattoo Removal Psoriasis Management Acne Therapy Anti-Aging Interventions

|

| By End User |

Hospitals Dermatology Clinics Home Care Settings

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Craniomaxillofacial devices market is segmented based on technology as follows: plate and screw fixation systems, bone graft substitutes, TMJ replacement systems, distraction systems, and cranial flap and thoracic fixation systems. Plate and screw fixation devices enjoy the highest volume by percentage since they are used extensively for trauma, reconstructive, and orthognathic surgery. Implants are normally composed of titanium or bioresorbable material, provide rigid stable fixation, and are best suited in terms of modularity and compatibility with radiography. Bone graft substitutes are used in instances of intrinsic bone deficiency, and they find most common use in trauma, tumor resection, or congenital defect reconstruction.

They are demineralized matrices, allografts, and synthetic ceramic biomaterials whose function is the stimulation of osteogenesis. TMJ replacement systems treat jaw disorders ankylosis and arthritis through anatomical and functional reconstruction through the use of CAD-fabricated, custom-designed implants. Distraction osteogenesis systems treat congenital facial deformities through controlled lengthening of bone, frequently applied in the pediatric patient. Finally, cranial flap fixation systems are neurosurgical for the fixation of bone following craniotomy, and thoracic fixation systems are reconstructive in nature within the thoracic cavity. Typically, these technologies are cosmetic as well as functional surgical requirements, with technological advancement concentrated on better materials, precision in design, patient comfort, and minimizing revision surgery.

Craniomaxillofacial devices are applied in trauma reconstruction, neurosurgery and ENT, orthognathic and dental surgery, and plastic and cosmetic surgery. The demand for trauma reconstruction is greatest because facial trauma due to road accidents, falls, and violence is extremely prevalent. The patients must be treated promptly and successfully by accessible fixation appliances and implants to achieve facial anatomy and function. CMF devices play a very crucial part in neurosurgery and ENT for the management of cranial base neoplasms, skull defects, and compound infection. Their precision and stability are of utmost priority for successful operation in sensitive brain and facial nerve fields.

CMF devices are utilized in dental and orthognathic procedures for the adjustment of jaw malalignments, malocclusions, and various other maxillofacial deformities. Increased demand for cosmetically enhanced smiles and functional rearrangements of the jaw is driving this segment. Cosmetic and plastic surgery simultaneously has experienced increased acceptance of CMF devices for chin, jaw, and cheek augmentations. With advances in technology, natural contours are feasible without extended scarring and healing and thus are perfectly suited to cosmetic augmentation. With an escalating degree of surgical competence and a need for patients, these applications increasingly overlap and expand, requiring devices that provide structural integrity and cosmetic precision. Together, these markets represent the need for widespread clinical use of CMF products in contemporary medicine.

Ambulatory surgical centers (ASCs), specialty clinics, and hospitals are three general end users of the craniomaxillofacial devices market. Hospitals have the greatest market share through shared infrastructure, multidisciplinary surgical teams and backup for managing emergency as well as complicated reconstructive cases. With their imaging capabilities and operating room services, hospitals are the site of attack for trauma treatment and management of congenitally deformed craniofacial disorders. ASCs, however, are emerging center-stage players with their cost-effective operations, reduced patient turnover, and applicability towards elective or limited procedures. With healthcare moving to outpatient centers, there is increasing usage of CMF devices in such centers for routine orthognathic, dental, and cosmetic surgeries.

Cosmetic facial surgery and targeted corrections are performed quite widely in specialty clinics, emphasizing treatment tailoring with the use of advanced surgery planning equipment and 3D imaging. The clinics encounter a patient population seeking individually tailored, typically elective procedures emphasizing appearance to an equal extent as functionality. Growing medical tourism and familiarity with facial-enhancing procedures are driving this segment’s growth. As healthcare delivery patterns change, all three end consumers—hospitals for urgency, ASCs for convenience, and clinics for personalization—are synergistic in establishing future demand for craniomaxillofacial devices.

North America is a leading destination in the dermatology devices market, thanks to its robust healthcare infrastructure and educated patient population. In the United States, routine skin cancer screening and increasing demand for aesthetic procedures maintain high demand. The FDA’s favorable attitude towards new approvals of devices encourages innovation. Dermatology centers are well established, and academic institutions ensure that product development continues. Insurance coverage of diagnostics enhances patients’ access. A combination of medical requirements and cosmetic objectives fuels steady expansion, as individuals become more inclined toward less intrusive procedures to address both skin wellness and cosmetic looks.

Europe maintains a stable but slowly expanding dermatology devices market, with its governmental healthcare environment in place. France and Germany offer extensive public access to medical technologies under universal healthcare systems. The EU’s rigid device safety regulations serve to engender confidence among users. Older age groups demand anti-aging solutions, while early skin cancer screening is encouraged by public health initiatives. Cosmetic device reimbursement rates differ, but coordinated regulation facilitates marketing new products. Northern Europe is especially utilizing teledermatology, expanding services into underserved areas and improving overall care quality.

The Asia Pacific market is rapidly changing, with rising economies significantly investing in healthcare. Japan continues to lead the way in sophisticated skin-care technology, while China and India are quickly building their network of skin clinics to satisfy growing demand. South Korea and Thailand lure medical tourists with low-cost aesthetic treatments. Preoccupation with pollution and looks has made skincare top of mind, further driving the market. Inconsistencies in regulations and inadequate reimbursement, however, continue to plague business operations. Regional players are making inroads by manufacturing affordable devices, particularly for domestic use, appealing to a wide, cost-conscious consumer base.

The LAMEA region provides a blend of opportunities and constraints. In Latin America, Brazil and Mexico are significant centers for cosmetic treatments, aided by increasing urban populations and private healthcare expenditure. Specialized clinics are growing, though adoption in the public sector is still restricted by cost. Meanwhile, luxury dermatology centers catering to locals and medical tourists alike find residence in the Middle East, most notably the UAE and Saudi Arabia. Africa is behind at a slower pace, with rural regions missing out on resources, but South Africa is notable for its advancing dermatology. Mobile clinics and regional manufacturing in certain areas seek to bridge gaps in care and lower import dependence.

The global Craniomaxillofacial Devices Market was valued at USD 12.5 billion in 2024.

The market is projected to grow at a CAGR of 10.2 % from 2025 to 2033.

Anti-Aging Treatments segment hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Lumenis Ltd., Alma Lasers, Cynosure, Bausch Health Companies Inc., Canon Medical Systems Corporation, Cutera Inc., Syneron Candela, HEINE Optotechnik, Aerolase Corp., and Bruker Corporation.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Dermatology Devices Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Dermatology Devices Market, By Application

5.3 Dermatology Devices Market, By End User

6.1 North America Dermatology Devices Market, By Country Type

6.1.1 Dermatology Devices Market, By Technology

6.1.2 Dermatology Devices Market, By Application

6.1.3 Dermatology Devices Market, By End User

6.2 U.S.

6.2.1 Dermatology Devices Market, By Technology

6.2.2 Dermatology Devices Market, By Application

6.2.3 Dermatology Devices Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping