Dialysis Machine Market

Dialysis Machine Market Share and Trend Analysis, By Technology (Hemodialysis Machines, Peritoneal Dialysis Equipment, Continuous Renal Replacement Therapy (CRRT), Wearable/Sorbent-Based Systems), By Application (Hospital-Based Dialysis, Outpatient Dialysis Centers, Home Dialysis), By End User (Hospitals, Dialysis Clinics, Home Care Patients) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

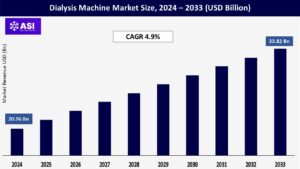

CAGR: 4.9%

Last Updated : August 11, 2025

The global Dialysis Machine Market was valued at USD 20.96 billion in 2024 and is projected to reach USD 33.82 billion by 2033, expanding at a compound annual growth rate CAGR of 4.9% during the forecast period (2025 – 2033).

Dialysis machines are life-support devices employed for conducting renal replacement therapy on patients suffering from acute or chronic kidney failure. These machines filter out toxins, excess water, and waste products of metabolism from the blood when the kidneys are no longer able to do so sufficiently. Hemodialysis machines utilize semi-permeable membranes and regulated fluid exchange, while peritoneal dialysis utilizes the patient’s own peritoneum as the filtration medium. Continuous renal replacement therapy (CRRT) is utilized in critical care to treat hemodynamically unstable patients. Applications span hospitals, dedicated dialysis centers, and home based care.

Over the past decade, rising incidence of end-stage renal disease (ESRD), driven by hypertension and diabetes, has fueled demand. Concurrently, advances such as portable and wearable dialysis systems, improved membrane biocompatibility, and integrated digital monitoring have enhanced patient convenience and treatment efficacy. Regulatory approvals in major markets and expanding coverage under national healthcare programs are further accelerating adoption. As medical infrastructure enhances and awareness among patients increases, particularly in developing economies, the market is well-placed to grow continuously.

Chronic kidney disease is a severe and worsening worldwide health burden. Its growing prevalence is directly due to interlinked factors: populations remaining longer, escalating incidence of diseases such as diabetes and high blood pressure, and the movement towards urban lifestyles commonly associated with less healthy diets and less physical activity. These factors add together to produce a rapid escalation of CKD cases globally. This is especially true in areas with few healthcare resources. Delayed disease identification and lack of proper access to early treatments often result in irreversible advancement to end-stage renal disease (ESRD), where life-supporting dialysis is necessary. Global health trends suggest CKD is expected to rise considerably as a principal cause of early death worldwide over the next few decades.

This increasing ESRD incidence directly translates to burgeoning demand for dialysis technology in all environments – big hospitals, dedicated outpatient facilities, and increasingly, patient homes. Health authorities in developed countries are reacting by establishing wider screening programs, further increasing the demand for diagnostic and treatment equipment. At the same time, policy reforms are enhancing access. Expansion of health insurance coverage and stronger government pay systems for dialysis treatments are substantially reducing the cost barrier for patients. This confluence of increasing patient volume, active screening, and enhanced support mechanisms is producing an intense, long-term upward pressure on the dialysis machine market, as healthcare systems seek to keep pace with this increasing challenge.

Uninterrupted and accelerated technology innovation in dialysis is a core driver of market expansion. The last few years have seen incredible advancements, most notably in creating ever-smaller, extremely portable hemodialysis units. These units provide patients with greater freedom and autonomy than ever before, allowing effective treatment within the comfort of home. This change profoundly improves quality of life by minimizing clinic visits and interruptions in regular routines, as well as lowering the high costs of multiple hospitalizations. Improvements reach deeply into the very core machine structures. New membrane materials, designed to have enhanced biocompatibility, significantly minimize negative patient responses such as inflammation and blood clotting.

This enhancement not only increases patient tolerance but also prolongs the functional lifetime of critical filters and permits potentially longer or more effective treatment sessions. In addition, the incorporation of advanced digital technologies is transforming care delivery. Machines are increasingly being equipped with Internet-connected sensors and utilizing cloud-based analytics platforms. This facilitates constant, real-time remote monitoring of key parameters – such as accurate blood pressure readings, ultrafiltration rates, and overall treatment efficacy. The clinicians receive valuable data, enabling timely, individualized therapy adjustments without physical presence. In the future, research extends boundaries even further. Wearable artificial kidneys and miniaturized sorbent-based dialysis systems are in active development.

The dialysis industry also experiences considerable growth headwinds with overwhelming fiscal burdens and unpredictable reimbursement schemes. The purchase of sophisticated dialysis equipment requires substantial initial capital outlays, frequently in the tens of thousands per machine, which puts tremendous pressure on healthcare centers, particularly in facilities with limited resources. In addition to the initial cost, the continuous cost of vital disposable parts – such as dialyzers, specialized tubing, and filters – forms a continuing fiscal barrier. Though peritoneal dialysis provides useful at-home treatment convenience, the regular monthly expense of required solutions is still significant. Insurance coverage demonstrates striking worldwide inequality. Patients in many developing countries face prohibitively high out-of-pocket costs, essentially depriving access to life-supporting treatment.

Governments with limited healthcare budgets often cater to acute and infectious disease care at the expense of long-term chronic care such as dialysis, leading to limited or unreliable reimbursement rates. This shortfall in funding triggers a chain of adverse consequences: viable machines may be idle because of cost-of-operation considerations, older machinery rides out longer than ideal replacement periods because of capital limitations, and implementation of new, possibly more efficient technologies is slowed to a crawl. Movement toward setting up value-based care systems and bundled payment arrangements, seeking to tie payment to patient outcomes and overall cost-effectiveness, are being proposed as possible solutions. But such sophisticated programs take a lot of time to develop, align with stakeholders, and implement before they can provide broad, consistent funding sources that can surmount the existing financial hurdles and effectively increase patient access worldwide.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Hemodialysis Machines Peritoneal Dialysis Equipment Continuous Renal Replacement Therapy (CRRT) Wearable/Sorbent-Based Systems

|

| By Application |

Hospital-Based Dialysis Outpatient Dialysis Centers Home Dialysis

|

| By End User |

Hospitals Dialysis Clinics Home Care Patients

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Hemodialysis is still the dominant technology, which generates the majority of market revenue. It is because of its strong-rooted clinical acceptance and standard treatment protocols. Conventional stationary hemodialysis equipment form the core of hospital and dialysis center operations, but portable and mobile units are more and more commonly used for home dialysis programs, particularly in North America and Europe, providing patients with flexibility. Peritoneal dialysis systems constitute an alternate strategy, employing fluid installed into the abdomen. The strategy provides a less equipment-requiring alternative, appropriate for self-manageability by the patient, making it crucial in regions with limited clinical infrastructure.

Continuous renal replacement therapy devices play a vital role in intensive care units. Made for critically ill patients, they offer continuous, gentle blood purification that unstable patients can better handle. In the future, the market may be transformed by products in the process of clinical trials. Sorbent-based technology and wearable artificial kidney designs hold potential revolutionary transformations. These technological advancements have the goal to significantly minimize equipment size and fluid demands while taking steps toward increased patient mobility and convenience. Each technological segment targets specific patient needs and healthcare settings, which directly determine equipment design, pricing strategies, and related service delivery models.

Dialysis machine deployment is seen across three main settings: hospitals, freestanding dialysis centers, and home care. Hospitals use machines mainly for inpatients requiring acute or emergency renal replacement. The machines usually include continuous renal replacement therapy functionality and advanced monitoring capabilities for critical care. Freestanding dialysis centers – including freestanding clinics and outpatient departments – represent the core service delivery structure. They perform routine hemodialysis sessions efficiently through many machines in each facility, with advantages of economies of scale, highly specialized clinical personnel, and standard treatment protocols.

Home dialysis is the fastest-growing application segment. This is driven by patient demand for convenience of treatment and self-administration, facilitated by technological innovation in remote monitoring. Home hemodialysis and peritoneal dialysis equipment is more portable and user-friendly, facilitated by extensive patient training programs. Most importantly, payment policies among key markets increasingly support the uptake of home therapy as a means to reduce healthcare costs overall while enhancing quality of life and patient independence. Industry players are reacting with partnerships with service companies to provide package deals for integrated home solutions, including machine sale, patient education, and persistent telehealth support.

The principal end users of the dialysis machines are hospitals, dialysis clinics, and home care patients. Hospitals use highly versatile machines that can accommodate standard hemodialysis and continuous renal replacement therapy for the treatment of acute and critical inpatients. Dialysis clinics, often owned by large specialized chains, specialize in delivering scheduled outpatient treatments. They generally use mid-range equipment designed for high patient throughput, operational efficiency, and reliability in a specialized environment. Home care patients represent an accelerating end-user market, fueled by the trend towards decentralized care delivery.

This segment requires highly portable, automated devices with easy-to-use interfaces and strong remote connectivity for clinical monitoring. Taking into account the substantial upfront cost hurdle to home users, some manufacturers provide rental or subscription-based options. They tend to package the machine with regular maintenance and regular supplies. Priorities vary dramatically between end-use markets: hospitals and clinics require highest device availability and complete service agreements, whereas home consumers value ease of use, safety features built-in, and prompt after-sales support. Accordingly, manufacturers adjust their technical support systems and training programs to address these unique requirements, providing safe and effective use in the various settings in which dialysis care is provided.

North America dominates dialysis adoption owing to extremely high ESRD rates and strong reimbursement systems such as the U.S. Medicare ESRD program. Strong infrastructure supports quick technology adoption, most notably home dialysis facilitated by value-based payment systems. Large-scale producers have comprehensive service networks for effective deployment. In spite of cost pressures and access imbalances in underserved populations, the region leads in portable systems and wearable technology. Regulatory stringency guarantees safety but might slow innovation. Market maturity supports high service levels and replacement cycles, with aging populations and chronic conditions driving steady demand for advanced equipment in hospital, clinic, and home environments.

Europe’s second-largest dialysis market after the U.S. depends on universal coverage from robust public health systems in Germany, France, and the U.K. Strict EMA regulations maintain high standards of safety and performance, and sustainability efforts fuel demand for water-saving machines. Adoption of home dialysis is regionally varied but expands under national strategies for chronic care. Eastern Europe is promising with increasing healthcare investments, and cross-border coordination unifies reimbursement to facilitate technology diffusion. Challenges are constraints on budgets and outdated infrastructure, but the area focuses on energy-efficient innovations and telehealth adoption, consistent with EU Green Deal goals to treat disparities.

Asia Pacific is the most rapidly expanding dialysis market, driven by increased CKD due to diabetes/hypertension and growing healthcare access. China and India lead patient volumes but have low device penetration, with immense unmet demand. Japan’s aging population drives home hemodialysis uptake, with government programs financing clinic growth and public hospital renovations. Collaborations between international producers and domestic companies make it more affordable, and telehealth fills rural-urban surveillance deficits. Reimbursement fragmentation, staffing shortages, and cost inhibition notwithstanding, transportable systems become increasingly popular with peritoneal dialysis continuing to play a crucial role in remote locations, facilitated by policy transitions toward universal coverage.

LAMEA’s fragmented market reflects stark contrasts: Latin America (pioneered by Brazil/Mexico) exhibits stable growth through public-private partnerships and cost-led peritoneal dialysis dominance, although economic instability limits infrastructure. In contrast, the GCC (Saudi Arabia/UAE) invests aggressively in technology-savvy centers with state-supported treatment and increasing home dialysis pilots, prioritizing sustainability through water-saving tech. Africa depends on NGOs and peritoneal dialysis where available, with telemedicine supporting limited coverage. Region-wide issues involve uneven reimbursement and supply chains, and development is dependent on localized solutions and foreign investment.

The global Dialysis Machine Market was valued at USD 20.96 billion in 2024.

The market is projected to grow at a CAGR of 4.9 % from 2025 to 2033.

Hemodialysis machines hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Fresenius Medical Care, Baxter International, DaVita Inc., B. Braun Melsungen AG, Nipro Corporation, Toray Medical Co., Ltd.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Dialysis Machine Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Dialysis Machine Market, By Application

5.3 Dialysis Machine Market, By End User

6.1 North America Dialysis Machine Market, By Country

6.1.1 Dialysis Machine Market, By Technology

6.1.2 Dialysis Machine Market, By Application

6.1.3 Dialysis Machine Market, By End User

6.2 U.S.

6.2.1 Dialysis Machine Market, By Technology

6.2.2 Dialysis Machine Market, By Application

6.2.3 Dialysis Machine Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping