Digital PCR Market

Digital PCR Market Share and Trend Analysis, By Technology (Droplet Digital PCR, Chip-based Digital PCR), By Application (Clinical Diagnostics, Oncology Research, Infectious Disease Detection, Genetic Analysis, Environmental Monitoring and Food Safety, Pharmaceutical and Biotechnology Applications, Research Institutions), By End User (Healthcare Institutions, Diagnostic Laboratories, Academic and Research Institutions, Pharmaceutical and Biotechnology Companies, Contract Research Organizations, Government Laboratories and Public Health Agencies) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

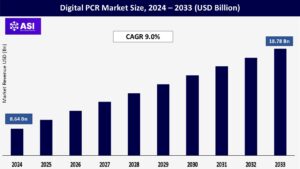

CAGR: 9.0%

Last Updated : August 11, 2025

The global Digital PCR Market was valued at USD 8.64 billion in 2024 and is projected to reach USD 18.78 billion by 2033, expanding at a compound annual growth rate CAGR of 9.0% during the forecast period (2025 – 2033).

Digital polymerase chain reaction is a state-of-the-art field of molecular biology methods that provides a previously uncharacterized level of sensitivity and accuracy for nucleic acid detection and quantitation. The technology divides samples into thousands of unique microreactions, providing absolute quantitation without standard curves or reference material. Digital PCR technology has emerged to be a valuable tool in a number of applications such as clinical diagnostics, oncology research, the detection of infectious disease, and genetic testing.

The high precision of the technology makes it highly useful for the detection of low-abundance targets, copy number variation, and rare mutations that would escape on the use of the traditional PCR approaches. Healthcare facilities, pharma firms, and research organizations employ digital PCR platforms more often because of their superior performance for liquid biopsy studies, precision medicine programs, and biomarker identification programs. Market growth is a result of increasing demand for precision diagnostic devices that will assist in the diagnosis of diseases at the early stage, monitoring of treatment, and therapy decision-making in all segments of medicine.

The rising significance of tailored health care strategies strongly fuels digital PCR market growth as health care systems globally give high value to patient-specific treatment strategies. Precision medicine programs need high-sensitivity molecular diagnostic equipment to identify unique genetic variations, biomarkers, and treatment targets influencing treatment selection and patient outcome. Digital PCR is more adept at detecting uncommon mutations, copy number alterations, and minimal residual disease markers that are pivotal in the creation of targeted therapy as well as monitoring for response to therapy.

The absolute quantification component of the technology eliminates reliance on standard curves, giving doctors better information to make therapeutic decisions. Pharmas increasingly incorporate digital PCR platforms into companion diagnostic development plans, paving the way for regulatory approval routes for targeted therapies. Clinicians appreciate the utility of digital PCR for cancer genomics, pharmacogenomics, and the diagnosis of rare diseases, where accurate molecular identification has a direct impact on patient care quality. Government initiatives for precision medicine research, such as the high funding allocations provided for genomic studies, also stimulate the application of digital PCR in research and clinical use.

The increasing global cancer and genetic disease burden generates broad needs for new diagnosis technologies that have the capacity to detect at an early stage and follow. Cancer is one of the major causes of death globally, and early detection significantly improves survival and cure. Higher sensitivity for the detection of circulating tumor DNA, cancer biomarkers, and treatment resistance mutations from liquid biopsy samples is offered by digital PCR technology. The fact that the technology can identify low-abundance nucleic acids makes it very useful in the detection of minimal residual disease, measurement of treatment response, and diagnosis of recurrence of disease.

Genetic illnesses that afflict millions of people worldwide call for sophisticated diagnostic equipment to diagnose them with accuracy and introduce family screening programs. The digital PCR systems surpass to identify copy number variation, gene duplication, and allelic variants of low frequency causing inherited diseases. Healthcare networks globally invest heavily in molecular diagnostic facilities to support increasing patient populations needing genetic testing services. Aging populations across the globe give rise to rates of incidence of cancer and generate requirements for advanced diagnostic platforms with the ability to offer early intervention schemes. Outbreaks of infectious diseases, such as ongoing pandemics, illustrate the unparalleled merit of digital PCR in detecting pathogens and surveillance programs.

The high upfront capital expense of digital PCR instruments constitutes monumental barriers to extensive utilization, especially for smaller medical facilities and low-resource laboratories. Digital PCR instruments are typically high-end equipment that comes with initial investments higher than typical PCR equipment, which are financially unaffordable to under-resourced institutions with limited budgets. Operational costs such as specialized reagents, consumables, and maintenance agreements trigger recurring capital outlays that discourage adopters from embracing such technologies. Digital PCR system complexity requires professional training of laboratory staff, at the cost of additional time and expense requirements for successful implementation.

Trained technicians, who are capable of using cutting-edge molecular diagnostic equipment, are not available in most geographies, which restricts coverage in underpenetrated markets. Healthcare reimbursement policies tend to lag behind technology development and introduce uncertainty in cost recovery on digital PCR-based diagnostic testing. Smaller diagnostic laboratories and research institutions may struggle to justify investments in digital PCR when there are other demands on limited available funding. Specialist expertise is necessary for technical interpretation of results, which is not always present in every laboratory, potentially causing delays in installation or suboptimal utilization of the strengths of the platform.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Droplet Digital PCR Chip-based Digital PCR

|

| By Application |

Clinical Diagnostics Oncology Research Infectious Disease Detection Genetic Analysis Environmental Monitoring and Food Safety Pharmaceutical and Biotechnology Applications Research Institutions

|

| By End User |

Healthcare Institutions (Hospitals, Diagnostic Laboratories, Clinical Research Organizations) Diagnostic Laboratories Academic and Research Institutions Pharmaceutical and Biotechnology Companies Contract Research Organizations Government Laboratories and Public Health Agencies

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Digital PCR technology consists of two main platforms: droplet digital PCR and chip-based digital PCR systems, both of which provide numerous benefits for different applications. Droplet digital PCR leads the market segment because it has better performance capabilities and widespread commercial availability from top manufacturers. Water-in-oil emulsion chemistry is employed in droplet digital PCR to produce thousands of isolated droplets of template molecules, which facilitate highly precise quantitation through Poisson distribution analysis. Multinationals such as Bio-Rad Laboratories have developed end-to-end digital PCR systems for droplets with unparalleled sensitivity for the detection of rare mutations and copy number examination.

Chip-based digital PCR systems produce multiple solutions by partitioning the sample into separate reaction chambers through microfluidic array partitioning. The systems leverage advances in throughput capacity and automation and are best for use in laboratory applications requiring high throughput. Current technological advancements center around enhancing multiplexing capability, enhancing automation functionality, and decreasing processing time to maximize laboratory workflow efficiency. The technology sector keeps evolving with the introduction of new platform innovations responding to particular market requirements such as point-of-care, heightened sensitivity, and simplified operation protocols.

Digital PCR application covers varied applications such as clinical diagnostics, cancer research, infectious disease monitoring, and gene analysis, with oncology being the largest application segment. Cancer diagnosis drives strong market demand by way of liquid biopsy uses, analysis of circulating tumor DNA, and minimal residual disease monitoring programs. The technology is best suited for the detection of low-prevalence cancer mutations, therapeutic response monitoring, and detection of drug resistance markers that inform therapeutic choice. Infectious disease use was highlighted by recent pandemic experience, as digital PCR’s sensitivity is suitable to pathogen detection and viral load measurement.

Examples of genetic testing application include copy number variation analysis, screening for inherited disease, and pharmacogenomic study to establish personal medicine programs. Applications in the environment and food security involve the identification of genetically modified organisms, pathogen contamination, and antimicrobial resistance markers by digital PCR. The biotech and pharmaceutical industries are now using digital PCR for drug development applications such as biomarker validation, companion diagnostic development, and quality control of cell therapy. Digital PCR technology is applied in research institutions in gene expression studies, epigenetic analysis, and next-generation sequencing library quantification. The variety of applications demonstrates the adaptability and growing utility of digital PCR across various scientific fields and commercial applications.

Hospitals, diagnostic laboratories, and clinical research organizations are the key end-user market for digital PCR technology. Diagnostic laboratories are especially responsible for driving growth in the market with rising use of molecular diagnostic platforms for routine clinical testing. These laboratories need high-throughput, precise instruments able to handle multiple sample types under strict quality control. Academic and research institutions are another key end-user segment, using digital PCR platforms for basic research, biomarker discovery, and method development work. Pharmaceutical and biotechnology firms increasingly incorporate digital PCR instruments into drug development pipelines, regulatory filings, and quality control for manufacturing.

Dedicated contract research organizations offer digital PCR services to aid in clinical trials, biomarker research, and regulatory compliance programs. Digital PCR technology finds application in government laboratories as well as public health institutions for the surveillance of diseases, outbreak investigations, and population health monitoring programs. The end-user market remains growing as technology improves by way of availability and applications increase across numerous different industries. Smaller point-of-care and lab environments are discovering opportunities in emerging markets as companies create simpler, more affordable digital PCR platforms.

North America leads the global digital PCR market with robust market share fueled by developed healthcare infrastructure and heavy research spending. The United States leads regional growth with widespread use of molecular diagnostics in clinical practices and research-active pharmaceuticals. Market leaders such as Bio-Rad Laboratories, Thermo Fisher Scientific, and other industry majors have strong presence in North American markets. Government-funded schemes for precision medicine research and genomic research drive digital PCR adoption in academic and clinical establishments. The area is aided by the favorable reimbursement practices and policy environments to facilitate the adoption of new technologies.

European digital PCR markets are characterized by sustained growth underpinned by robust healthcare systems and high research and development expenditures. Germany, France, and the UK are important European markets underpinned by advanced diagnostics infrastructure and early take-up of technology. The European regulatory authorities such as the European Medicines Agency encourage the adoption of digital PCR with streamlined authorization for diagnostics purposes. A growing aging population and cancer incidence in the region generate high demand for precision diagnostic technology. Mutual research partnerships between European institutions and biotechnology firms drive market growth and technological advancements.

Asia Pacific is the region with the highest growth rate of digital PCR technology due to rising healthcare infrastructure and growing research activity. China, Japan, and India are representative of massive market potential with developing pharma industries and government healthcare spending. The region also experiences rising incidence of chronic conditions such as cancer, hence creating massive demand for sophisticated diagnostic technology. Increased healthcare spending and enhanced laboratory infrastructure facilitate the adoption of digital PCR in a wide range of applications. Government initiatives towards establishing biotechnology and precision medicine research drive the market within the region.

Latin America and Middle East Africa regions reflect rising market opportunity for digital PCR technology, albeit currently with smaller market shares. Both markets have challenges such as decaying healthcare infrastructure and stringent budgets that will have the tendency to slow down technology adoption. Stronger knowledge of the advantages of precision medicine and more research activity, though, present market growth opportunities. Government support for healthcare modernization and infectious disease surveillance programs reinforces digital PCR adoption. International partnerships and technology transfer programs encourage the rapid rate of market growth in these emerging nations.

The global Bronchoscope market was valued at USD 8.64 billion in 2024.

The market is projected to grow at a CAGR of 9.0 % from 2025 to 2033.

Droplet Digital PCR (ddPCR) hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Bio-Rad Laboratories, Inc., Thermo Fisher Scientific Inc., QIAGEN N.V., F. Hoffmann-La Roche AG, Stilla Technologies, Abbott Laboratories, Agilent Technologies, Inc., Takara Bio Inc., Danaher Corporation, and Merck KGaA.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Digital PCR Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Digital PCR Market, By Application

5.3 Digital PCR Market, By End User

6.1 North America Digital PCR Market, By Country

6.1.1 Digital PCR Market, By Technology

6.1.2 Digital PCR Market, By Application

6.1.3 Digital PCR Market, By End User

6.2 U.S.

6.2.1 Digital PCR Market, By Technology

6.2.2 Digital PCR Market, By Application

6.2.3 Digital PCR Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping