Disposable Medical Gloves Market

Disposable Medical Gloves Market Share and Trend Analysis, By Material Type (Latex, Nitrile, Vinyl, Polyethylene), By Application (Examination, Surgical, Laboratory), By End User (Hospitals, Diagnostic Labs, Home Healthcare) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033.

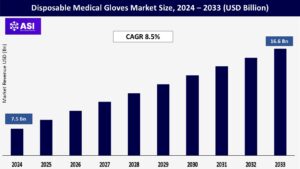

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 8.5%

Last Updated : August 11, 2025

The global Disposable Medical Gloves Market was valued at USD 7.5 billion in 2024 and is projected to reach USD 16.6 billion by 2033, expanding at a compound annual growth rate CAGR of 8.5% during the forecast period (2025 – 2033).

Disposable medical gloves have become an absolute imperative of modern healthcare as an essential barrier against infection and transmission of contaminants. These throwaway gloves prevent both the patients and health workers from cross-contamination as they receive medical treatment, test, and examinations. The industry produces gloves using various materials like latex, nitrile, vinyl, and polyethylene with varying properties for particular purposes. Their uses extend beyond hospitals and clinics to dental facilities, home care, diagnostics, and even non-clinical plants where hygiene is very important.

Increased awareness of infection control and disease prevention, along with improved regulation and expanded healthcare services, has driven demand for disposable gloves. With changing models of healthcare delivery and the world grappling with emerging infectious pathogens, the consumption of disposable gloves is increasing even more, making it a key component of public health protection.

Infection control has taken the pole position among the efforts to deliver quality care, and disposable gloves head the pole position. The decade has seen a series of outbreaks of infectious illnesses, ranging from viral epidemics to hospital-acquired infections, each one contributing to emphasizing the necessity for strict hygiene protocols. These disposable gloves are today an integral part of daily routine among health care providers, relying on them to create a barrier between them and potentially infectious microbes.

This heightened infection control focus is not only limited to hospital environments but has found its way to outpatient clinics, diagnostic centers, and even home care. As the public has become more aware of the risks of infectious disease, disposable glove sales have increased exponentially. Government policy, health promotion programs, and institutional policy have all contributed to this trend, and gloves have become ubiquitous standard of healthcare encounters. Rising levels of chronic illness, by definition necessitating long-term medical care, serve only to reinforce the need for reliable protective equipment. In this environment, disposable gloves are not a privilege–they are an essential, a comfort to patients and caregivers.

The look of disposable medical gloves has been transformed with advances in material technology and production methods. Although latex gloves have been the standard with their sensitivity and flexibility for many years, allergic responses have pushed the trend toward synthetics. Nitrile gloves have emerged as a popular leader due to resistance to chemicals, durability, and comfort. Gloves also offer an easy option for people with latex allergy, allowing their use by a broader population. Vinyl gloves, while not being as durable, provide the low-cost alternative for low-risk procedures, whereas polyethylene gloves are used where high rates of change are involved.

The sector has also tackled the environmental concern by producing biodegradable gloves made of vegetable material, in response to the demand from the market for environmentally friendly options. Technological advancements in design have led to ridged surfaces for improved grip, powder-free finishes to reduce irritation, and improved fit for improved comfort with prolonged use. Industrialization has achieved more quantity and uniformity, with the gloves being produced in bulk even during high-demand seasons. These changes not only improved the quality and variety of gloves available but also enabled manufacturers to create products to suit specific needs of different medical specialties.

Though there are quite a few drivers for the disposable medical glove market, there are some valid restraints. Raw material price volatility is one of the most important among them. Synthetic and latex glove manufacturing depends heavily on natural rubber supply and petroleum compound, which subsequently grapple with the pressures of increasing supply and demand globally. An unexpected spike in raw material costs may strangle producers’ margins as well as inflate end-users prices, potentially limiting availability in poor conditions. Environmental concerns are also a matter of special concern. Most disposable gloves are non-biodegradable and single use, contributing to the burden of medical waste.

With plenty of used gloves being generated in medical facilities, the environmental burden is increasingly becoming intolerable. Calls for greener practice are made by regulatory bodies and activist organizations, but a more environmentally friendly alternative requires a high research and development capital as well as production capacity. New material market entry is also avoided by strict regulatory guidelines, which enforce rigorous testing and certification for safety and effectiveness. Cost, function, and sustainability have to be balanced by manufacturers, who have to contend with these cross-matching forces while fulfilling the mounting demand for disposable gloves.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Latex Nitrile Vinyl Polyethylene

|

| By Application |

Examination Surgical Laboratory

|

| By End User |

Hospitals Diagnostic Labs Home Healthcare

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Segmentation of disposable medical gloves market is based on materials utilized in their production, which possess properties specific to individual and are applicable for respective applications. Latex gloves have been widely used over many years due to their good elasticity, comfort, and sensitivity, making them appropriately equipped for delicate surgical procedures and procedures requiring precision. But with the passing time, there has been a steady shift towards the artificial substitutes due to the danger posed by allergic reactions. Nitrile gloves are gaining popularity due to enhanced puncture resistance, chemical protection, and being hypoallergenic. Their cross-clinical use has made them the first choice in most medical centers, ranging from the emergency ward to laboratories.

Vinyl gloves, though less resistant, provide a cost-effective alternative for procedures that have low risk such as routine tests and food preparation. Light polyethylene gloves perform best where continuous glove replacement is required, for instance, in food preparation or housekeeping activities. The recent past has also witnessed the development of biodegradable gloves made from renewable raw materials where greater concern is placed on environmental care. Selection of the material is normally influenced by user-oriented needs, for instance, protection, comfort, economy, and environmental compatibility. Manufacturers evolve along with the market by developing new formulations and materials to meet changing healthcare professionals’ and facilities’ needs.

Disposably medical gloves are used on diverse applications with differing protection and performance requirements. The most extensive application is examination gloves, which are used in general patient assessment, diagnostic procedures, and non-surgical treatment. Examination gloves offer a consistent barrier to contaminants without hindering dexterity and comfort. Surgical gloves are another highly critical category, which is made for use in operating rooms where sterility, resistance, and sensitivity of the sense of touch become utmost priorities. These gloves undergo strong quality testing for ensuring them to provide the best safety and performance standards.

Protective gloves are used in specific activities like chemotherapy, where resistance to toxic chemicals is necessary, and in the laboratory setting, where resistance to biological and chemical threats is necessary. Disposable gloves, though, are not applied solely in the health sector but also in the food preparation, cleaning, and industrial sectors where protection and hygiene from contamination are needed. With medical practices becoming more complex and new risks emerging, application-specific demand for gloves should rise, which would drive innovation and fragmentation in the market. Firms are responding with gloves that bear features individually tailored to address the specialized requirements of each use, from enhanced grip and fit to enhanced chemical and pathogen resistance.

The disposable glove market for end-users is as diverse as the applications to which they are adapted. Hospitals are the biggest consumers and, even among these, by far the biggest by market size. They require a large number as well as high levels of procedure variety done on a daily basis. In emergency rooms, operating rooms, intensive care units, and general hospital wards all along hospitals, gloves are used, and they vary in protection and performance needs. Diagnostic labs are a second big category of end-users, relying on gloves to protect staff in the sampling process, analysis, and handling potentially infectious materials.

Home health care has created new demand for disposable gloves as patients and caregivers attempt to remain sanitary when receiving in-home care and personal treatments. The primary market drivers include dental clinics, ambulatory surgical centers, and outpatient facilities, each with particular needs for glove comfort and durability. Veterinary clinics and pet centers also became major end-users, expanding the market even wider. As models for healthcare delivery evolve, the range of end-users will be wider and will present new opportunities for companies to design products that serve precise needs of individual customer segments.

North America dominates the disposable medical gloves market because of developed healthcare infrastructure, high levels of infection prevention awareness, and rigorous regulatory mandates. The region is enriched with well-developed supply chains as well as safety concern and quality focus, the result of which is gloves’ easy availability to fulfill the requirement of healthcare professionals. The renewed effort to enable local production further entrenched the market, reducing import reliance and creating a more robust supply chain during periods of higher demand.

Europe dominates a significant share of the market with comprehensive healthcare networks and strict regulatory frameworks. Greenism has risen across the entire continent, with purchasing policies supporting gloves made from environmentally compatible material. Compliant infection control protocols and ongoing investment in healthcare infrastructure have maintained steady growth across the continent, with countries focusing on quality, safety, and environmental care.

Asia Pacific is the biggest expanding disposable medical gloves market, with its growth fueled by growth in healthcare services expansion, increasing healthcare awareness of hygiene, and increased healthcare spending. Malaysia, Thailand, and India are top manufacturing hubs, exporting and supplying locally. Expansion in this region is also facilitated by the enhancement in the availability of healthcare, increased infection control consciousness, and rapid build-out of healthcare infrastructure in emerging economies.

Latin America is seeing steady growth of the disposable medical gloves market as a result of increased access to healthcare, growth in government public healthcare expenditure, and increasing infection control awareness, with regional demand led by Brazil even though price sensitivity remains; in contrast, the Middle East and Africa region offers incredible future opportunities driven by investments in health centers and government efforts to modernize, which are driving premium protection equipment demand, although logistical issues within the supply chain and cost remain – however, the two regions are set to grow even further in the market as access to healthcare improves and infection control becomes increasingly a priority issue.

The global Disposal Medical Gloves Market was valued at USD 7.5 billion in 2024.

The market is projected to grow at a CAGR of 8.5 % from 2025 to 2033.

Examination gloves hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Top Glove Corporation, Hartalega Holdings, Kossan Rubber Industries, Ansell, Cardinal Health, Supermax Corporation, Semperit AG, Rubberex, Mölnlycke Health Care, Kimberly-Clark, Dynarex.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Disposable Medical Gloves Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Disposable Medical Gloves Market, By Application

5.3 Disposable Medical Gloves Market, By End User

6.1 North America Disposable Medical Gloves Market , By Country

6.1.1 Disposable Medical Gloves Market, By Technology

6.1.2 Disposable Medical Gloves Market, By Application

6.1.3 Disposable Medical Gloves Market, By End User

6.2 U.S.

6.2.1 Disposable Medical Gloves Market, By Technology

6.2.2 Disposable Medical Gloves Market, By Application

6.2.3 Disposable Medical Gloves Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping