Electric Motor Sales Market

Electric Motor Sales Market Size, Share & Trends Analysis Report By Motor (AC, DC, Hermetic), By Power Output (Integral HP Output, Fractional HP Output), Application (Motor Vehicle, HVAC) Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

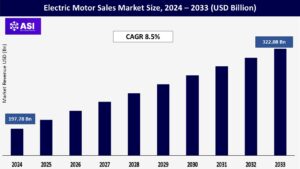

CAGR: 8.5%

Last Updated : June 23, 2026

The global Electric Motor Sales Market size was valued at USD 197.78 billion in 2024 and is projected to reach USD 322.08 billion by 2033, growing at a CAGR of 8.5% from 2025 to 2033.

The growth of this market is primarily driven by the growing demand for home appliances such as refrigerators, dryers, vacuum cleaners, grinders, mixers, and others, the increasing inclination towards the utilization of green vehicles, and government support and encouragement for the adoption of electric vehicles.

In addition, rising awareness regarding sustainability and the significance of reduced carbon emissions is adding to the growth of this market.

According to the U.S. Energy Information Administration, the combined sales of plug-in hybrid electric vehicles, battery electric vehicles (BEVs), and hybrid vehicles grew from 17.8% in the first quarter of the financial year 2024 to 18.7% in the second quarter. The 30.7% year-over-year increase in the sale of hybrid vehicles mainly influenced this growth.

Continuous research and development efforts are focused on enhancing the efficiency of electric motors. Advancements in motor design, materials, and manufacturing processes help reduce energy losses, resulting in higher overall efficiency and lower operating costs.

The development of electric motors with higher power density allows for more compact designs without sacrificing performance. These high-power density motors are particularly valuable in applications where space is limited, such as automotive propulsion systems and industrial machinery.

In September 2022, Mitsubishi Electric Corporation announced that it has jointly developed an electric motor design support system with Toshiba Mitsubishi-Electric Industrial Systems Corporation (TMEIC) that incorporates Mitsubishi Electric’s Maisart AI technology to reduce the time required to generate electricity significantly, engine designs that achieve the same efficiency as conventional design methods used by experienced engineers by hand.

TMEIC plans to introduce the system for internal work in the financial year 2024. The new system can be used in the design of electric motors for industrial pumps, compressors, and fans.

The heating and air-conditioning (HVAC) industry has expanded with the growing demand for heating and cooling across residential, commercial, and industrial locations. This has led the new construction activities to look at the HVAC equipment supply in the buildings as an important characteristic during construction.

Moreover, it has ultimately fueled the demand for the deployment of electric motors. Developing economies are the major countries indulged in the HVAC industry’s growth as commercial spaces are increasing, along with the rising standard of living.

The major factor that can restrain the key market growth is the high maintenance cost of the motor. In some cases, the operational cost is also very high, which can hamper its adoption by customers.

For example, if a high-horsepower motor is used, along with a low load factor, the cost per hour of the operation increases significantly. However, some motors do not have a self-starting torque, as in the case of induction motors.

Furthermore, auxiliaries may also be required to start single-phase motors. Therefore, the growth of the market may impede on account of such factors.

Neodymium spot prices slid 42% in the past 12 months after earlier spikes, complicating BOM forecasts for traction-motor programs. EV platforms require up to 5 kg of magnet material, so price swings ripple through entire model portfolios.

OEMs hedge by dual-sourcing and experimenting with magnet-reduced topologies such as ferrite-assisted synchronous motors. Parallel research on synchronous-reluctance designs offers magnet-free torque maps but demands tight air-gap machining.

The uncertainty nudges procurement teams toward long-term offtake contracts, yet sustained volatility could still shave growth from the electric motor market.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Motor Type |

AC Dc Hermetic |

| By Power Output Type |

Integral HP Output Fractional HP Output |

| By Application Type |

Motor Vehicle Segment HVAC |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

AC motors segment dominated the global market with a revenue share of 71.2% in 2024. This high share is attributable to AC motors’ extensive applications, ranging from irrigation pumps to modern-day robotics. Furthermore, they are smaller, cheaper, lighter, and extensively used in HVAC equipment.

The adoption of electric AC motors in the automotive industry has increased exponentially, owing to the advent of highly efficient and low-cost electronics, accompanied by improvements in permanent magnetic materials.

Increasing demand for them in various industries, including chemicals, paper and pulp, cement, and wastewater treatment, is likely to further contribute to the segment’s growth.

Growing sales of electric vehicles and the subsequent scope of the machine type are also expected to spur the segment’s growth over the forecast period.

The hermetic motors segment is projected to grow at the fastest CAGR of 8.9% from 2025 to 2033. Hermetic motors are mainly used in various applications such as centrifugal chillers, commercial air conditioning units, household and commercial refrigerators, aircraft engines, and industrial operations.

Rising demand for advanced commercial cooling solutions in large enterprises, spacious commercial buildings, and households is primarily driving the growth of this segment. In addition, the increasing use of cold storage by the retail and food industry also contributes to hermetic motors’ growth opportunities.

Fractional HP output segment held the largest revenue share of this market in 2024. The growth of this segment is mainly influenced by factors such as its wide array of use cases in all household appliances, ranging from vacuum cleaners to coffee machines and refrigerators.

It is also used in industrial equipment as it proves suitable for operations in a heavy industrial environment. These motors have numerous advantages, including high starting torque and stability over electric current fluctuations.

In addition, the energy efficiency provided by FHP motors is higher than that of its counterparts, which is poised to translate into greater demand from industrial users willing to replace existing machines with more efficient ones.

Integral HP output segment is projected to grow at fastest CAGR from 2025 to 2033. The increasing demand for these motors in industrial applications primarily drives the growth of this segment. IHP motors are commonly used in centrifugal pumps, power air and gas compressors, pneumatic systems, refrigeration systems, conveyors, material handling equipment, etc.

The growing adoption, increasing automation of manufacturing processes in multiple businesses, and availability of advanced industrial machinery are anticipated to drive the demand for IHP output electric motors.

Based on application, the motor vehicles segment dominated the global electric motor market in 2024. This is attributed to multiple aspects, such as the growing focus of governments on reducing the carbon footprint of motor vehicles and developing sustainable transportation and mobility solutions.

The focus of multiple automotive industry brands on launching their advanced products in global and regional markets adds to the growth of this segment. For instance, in October 2024, Bentley Motors, one of the prominent companies in the automotive industry, announced the extension of the company’s Beyond100 strategy initiative, now referred to as Beyond100+, from 2025 to 2033.

The announcement also included confirmation from the brand regarding the launch of the first fully electric car in 2026. It also plans to build only fully electric vehicles from 2033 onwards.

The HVAC equipment segment is expected to experience the fastest CAGR from 2025 to 2033. This segment is mainly driven by growing demand from commercial buildings, increasing companies’ focus on delivering advanced products, rising inclination towards changing traditional workplaces into smart commercial spaces, and growing market and utilization of co-working spaces.

Furthermore, an increase in the use of HVAC systems in industrial settings for energy efficiency, maintaining air quality, and compliance requirements regarding the work environment is projected to add growth potential to this segment during the forecast period.

Asia Pacific electric motor market dominated the global industry, with a revenue share of 51.2% in 2024. The growing adoption of electric vehicles primarily influenced this market, and China made a significant contribution to it.

According to the U.S. International Trade Commission, approximately 1.60 million electric vehicles were exported from China in 2023. In addition, increasing demand for HVAC systems by industrial users, growing adoption of automation systems in multiple manufacturing businesses, and government support to shift dependence from other sources to energy-efficient electric motors are expected to drive more growth in the coming years.

Europe was identified as a lucrative region for the electric motor market. The growth of this market is driven by several factors, including government initiatives that support incentives and regulations promoting clean transportation, which lead to the adoption of electric vehicles and motors.

Focusing on reducing carbon emissions and developing charging infrastructure also contributes to Europe’s electric motor market growth. The demand for electric motors in the European market is primarily fueled by key countries such as the U.K., Germany, and France.

North America electric motor market is expected to experience substantial growth during the forecast period. This market is mainly influenced by factors such as growing demand for the automotive industry, increasing trend of automation in various manufacturing facilities, rise in the inclusion of industrial and commercial HVAC systems, and the presence of various key companies in the region.

In addition, increasing awareness regarding the reduction of carbon footprint and enhanced efforts by organizations and governments to include energy-efficient solutions are adding to the growth opportunities.

The market is expected to grow CAGR of 8.5% from 2025 to 2033.

The current market size is USD 197.8 B7illions in 2024.

Asia Pacific currently holds the largest market shares.

The Motor type segment is the leading segment in this market.

Some of the prominent players Allied Motion, Inc., AMETEK.Inc., Johnson Electric Holdings Limited, Nidec Motor Corporation, Franklin Electric, Regal Rexnord Corporation, Schneider Electric, Siemens, ORIENTAL MOTOR USA CORP.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Electric Motor Sales Market, By Motor Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Electric Motor Sales Market, By Power Output Type

5.3 Electric Motor Sales Market, By Application Type

6.1 North America Electric Motor Sales Market , By Country

6.1.1 Electric Motor Sales Market, By Motor Type

6.1.2 Electric Motor Sales Market, By Power Output Type

6.1.3 Electric Motor Sales Market, By Application Type

6.2 U.S.

6.2.1 Electric Motor Sales Market, By Motor Type

6.2.2 Electric Motor Sales Market, By Power Output Type

6.2.3 Electric Motor Sales Market, By Application Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping