Electric Truck Market

Electric Truck Market Size, Share & Industry Analysis, By Application (Logistics &Delivery, Waste Management) By Propulsion (BEV, PHEV, and FCEV), By Vehicle Type (Light Duty Trucks, Medium Duty Trucks, and Heavy Duty Trucks), Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

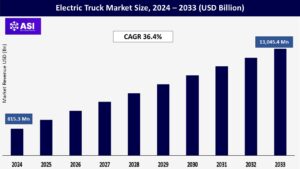

CAGR: 36.4%

Last Updated : June 23, 2026

The global Electric Truck Market size was valued at USD 815.3 million in 2024 and is projected to grow from USD 1,091.6 million in 2024 to USD 13,045.4 million by 2033, exhibiting a CAGR of 36.4% during the forecast period of 2025-2033.

Asia Pacific dominated the global market with a share of 51.74% in 2024. The electric truck market refers to the segment of the automotive industry that involves the production, sale, and utilization of trucks powered by electric motors and batteries rather than traditional internal combustion engines.

Fuel prices globally are highly uncertain and rising. Refueling solutions will also have costs that vary by region and increase over time. With gas prices rising, electric vehicles look more appealing to consumers.

It is estimated that the annual cost to fuel a light commercial vehicle is around USD 3,500 annually for the average American. The estimated cost to fuel a similar vehicle using a suitable electric propulsion system is around USD 850, roughly three times less.

EVs have significantly less running costs than IC vehicles as electric motors are more efficient than gasoline engines. Further, around 85% of the energy through an electric motor is converted into movement; on the other hand, it is around 40% in gas-powered vehicles.

In a situation where electricity and fuel costs were equal, a commercial electric vehicle would be cheaper to own than a gasoline-fueled vehicle. The major countries are also focusing on developing charging infrastructure, which will surge the demand for these trucks during the forecast period.

The recent trend of self-driving technology will influence the global market. Top manufacturers such as Tesla, Volvo, Vera, Daimler, and others have been developing this self-driving technology in trucks for the market.

Startup companies such as Embark, Einride, TuSimple, and others have also started developing this technology. Moreover, autonomous trucking brings greater efficiency to the trucking market.

Cargo companies need to move large quantities of cargo every day. Autonomous truck would allow companies to move more freight with the same number or even fewer drivers, as one person will be responsible for monitoring multiple trucks.

Polyurethane foam is a type of polymer created by combining two different kinds of liquid chemicals, an isocyanate (also known as side A) and a polyol, in addition to various additives and catalysts. This process results in polymer formation (known as side B.) The distillation of crude oil is the source of both of these chemicals.

When combined to make polyethene, isocyanates and polyols give off heat and vapour, respectively. Isocyanates have been shown time and again to present serious health risks. They can irritate the skin and make it more sensitive.

Cancer, asthma, lung damage, and other respiratory and breathing issues can be caused by the vapours and aerosols that are released during and after mixing side A and side B chemicals up until the time that the polyurethane is cured.

These vapours and aerosols can also irritate the skin and the eyes. Those who work with polyurethane vapours or are exposed to them are advised to follow the guidelines developed for personal safety by the Environmental Protection Agency (EPA). It can hinder the market growth.

The initial asset required for manufacturing electric trucks is comparatively much higher than CNG, petroleum, and diesel trucks. The cost of components and machinery used for production is also relatively high. This is majorly due to the high cost associated with electric batteries used in trucks.

Europe is responsible for over one-quarter of global EV assembly, but it is a tiny supply chain apart from cobalt processing at 20%. Moreover, the U.S. has an even more minor role in the global EV battery supply chain, with only 10% of EV production and 7% of battery production capacity.

The production of these trucks is less sophisticated than other conventional fuel trucks and thus is highly affected by the prices of batteries in the market. Further, in most regions, the raw material required for batteries is required to be imported, which also adds to the high prices of batteries.

The production of such commercial vehicles is currently limited due to the high cost incurred. According to a report by Forbes on energy innovation, the manufacturing cost of an electric truck is much higher currently compared to diesel or petrol trucks. Still, by 2030, it will be 50% cheaper compared to diesel and petrol variants with falling battery prices.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Vehicle Type |

Light Duty Trucks Medium Duty Trucks Heavy Duty Trucks |

| By Application Type |

Logistics & Delivery Waste Management |

| By Propulsion Type |

BEV PHEV FCEV |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The light duty trucks segment held the largest share of the market in 2024. Sales of light-duty have continued to increase. China accounted for the maximum number of light duty trucks in 2024. the growth is attributed to key market players and OEMs in the country.

Europe was the second largest market share in 2024 due to increasing response to carbon dioxide (CO2) performance standards. The medium-duty commercial trucks segment is emerging as the fastest-growing segment in the electric truck market, projected to grow at approximately 39% CAGR from 2025 to 2033.

This remarkable growth is primarily driven by increasing adoption in urban logistics, last-mile delivery services, and municipal applications. The segment’s rapid expansion is supported by the growing emphasis on zero-emission zones in cities and the rising demand for sustainable urban delivery solutions.

Medium-duty electric trucks are particularly attractive for businesses operating in metropolitan areas due to their optimal balance of range, payload capacity, and maneuverability.

The electric heavy-duty truck segment dominates the electric truck market, commanding approximately 87% market share in 2024. This significant market presence is driven by the increasing demand for sustainable solutions in long-haul transportation and logistics.

The segment’s dominance is reinforced by major fleet operators transitioning to electric commercial truck vehicles to meet stringent emission regulations and reduce operational costs. Heavy-duty electric trucks on the market are particularly gaining traction in regions with well-developed charging infrastructure and supportive government policies.

The segment’s strong performance is further bolstered by technological advancements in battery capacity and range capabilities, making these vehicles increasingly viable for commercial operations.

Battery Electric Vehicles (BEVs) dominate the electric truck market, commanding approximately 73% market share in 2024, driven by significant technological advancements in battery technology and growing environmental consciousness.

The segment’s prominence is reinforced by extensive government support worldwide, particularly in regions like China and Europe, where stringent emission regulations and substantial incentives are accelerating BEV adoption.

The Plug-in Hybrid Electric Vehicle (PHEV) segment is emerging as the fastest-growing category in the electric truck market, with projections indicating robust growth through 2025-2033.

This remarkable expansion is driven by PHEV’s unique ability to bridge the transition between conventional and fully electric vehicles, offering both range flexibility and emission reduction benefits. Fleet operators are increasingly favoring PHEVs for their versatility in long-haul operations while maintaining the ability to operate in zero-emission zones.

FCEVs represent an emerging technology with significant potential, particularly in heavy-duty long-haul applications where their quick refueling capabilities and extended range offer distinct advantages.

Both segments benefit from ongoing technological advancements and increasing investment in their respective infrastructures, contributing to the overall diversification of clean transportation solutions.

The logistics & delivery segment held the largest market share in 2024. This is attributed to the growing demand for sustainable and efficient last-mile delivery solutions, driven by the rise of e-commerce and increasing consumer expectations for rapid and reliable delivery of their orders.

Electric trucks are particularly suitable for urban logistics and delivery applications, where routes are typically shorter and more predictable, allowing for easier integration of EVs into existing fleets.

Additionally, logistics and delivery companies are under increasing pressure to reduce their environmental footprint, making electric trucks a viable solution to meet sustainability goals.

Waste management is expected to register a notable growth rate from 2025 to 2033. This is owing to the increasing adoption of EV technology in this area as a means of reducing emissions, operating costs, and environmental impact.

The growing demand for sustainable waste management solutions, driven by government regulations and consumer pressure, along with the need for cost-effective alternatives to traditional diesel-powered trucks, has positioned EV trucks as a viable option.

These vehicles are particularly used for waste management applications, where routes are often predictable and involve frequent stops, allowing for regenerative braking and optimized energy recovery.

The waste management sector is benefiting from advancements in EV technology, including increased range and payload capacity, which makes electric trucks a practical solution for a wider range of applications.

Asia Pacific led the electric truck market share (with China accounting for most of the share), and it stood at USD 224.5 million in 2024. The factors include a growth in the sale and registration of commercial electric vehicles. For instance, in 2024, China showed significant growth from 2023 to 2024.

Furthermore, most consumers prefer commercial electric vehicles in prime nations such as China, Japan, and India. This will result in an upsurge in demand for these trucks in the region.

Europe held a significant share of the global market in 2024. This is owing to the stringent regulatory environment and emission restrictions levied by the European Union, which compel vehicle manufacturers to adopt environment-friendly solutions.

In addition, the presence of a robust vehicle engineering and manufacturing ecosystem in countries such as Germany, the UK, and France has led to innovative solutions and bundled offerings by EV manufacturers.

For instance, in June 2024, Daimler Truck announced the launch of its TruckCharge brand in Europe, which offers all of the company’s solutions related to electric truck charging infrastructure.

North America dominated the global market with a revenue share of 37.6% in 2024. North America is also anticipated to observe promising growth in the market. In the U.S., electric truck brands have consistently increased demand. The number of electric LDVs per public charging point in the U.S. is 18. Also, the infrastructure investment in charging stations was increased by the government. These factors will impact the market growth.

The U.S. government, along with various state governments, has implemented tax credits, grants, and subsidies that encourage both manufacturers and consumers to invest in electric trucks. Additionally, new product offerings and associated services by manufacturers have fueled demand for EVs in the region.

The Middle East’s electric truck market is witnessing significant transformation as countries in the region diversify their economies and embrace sustainable transportation solutions. The market benefits from substantial investments in infrastructure development and growing environmental awareness.

The region’s commitment to reducing carbon emissions and modernizing transportation systems drives market growth, with various countries implementing supportive policies and incentives for electric vehicle adoption.

The market is expected to grow CAGR of 36.4% from 2025 to 2033.

The current market size is USD 815.3 Millions in 2024.

Asia Pacific currently holds the largest market shares.

Rising gasoline, fuel, diesel, and petrol prices are offering attractive chances for the worldwide electric truck market to flourish. Furthermore, prominent market participants are utilizing renewable energy sources in the production of electric vehicles on a global scale.

Some of the key players operating in the market are AB Volvo, Workhorse, BYD Company Ltd., Tata Motors, Daimler AG, Scania, Dongfeng Motor Company, Paccar Inc., Geely Automobiles Holdings Ltd., and Man SE.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Electric Truck Market, By Vehicle Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Electric Truck Market, By Application Type

5.3 Electric Truck Market, By Propulsion Type

6.1 North America Electric Truck Market , By Country

6.1.1 Electric Truck Market, By Vehicle Type

6.1.2 Electric Truck Market, By Application Type

6.1.3 Electric Truck Market, By Propulsion Type

6.2 U.S.

6.2.1 Electric Truck Market, By Vehicle Type

6.2.2 Electric Truck Market, By Application Type

6.2.3 Electric Truck Market, By Propulsion Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping