Electrocardiographs Market

Electrocardiographs Market Share & Trends Analysis Report, By Product Type (Resting ECG Systems, Holter Monitors, Stress ECG Systems, Event Recorders, Portable ECG, Stationary ECG, ECG Patches), By Lead Type (Single-Lead ECG, 2-Lead ECG, 3-Lead ECG, 6-Lead ECG, 12-Lead ECG), By Technology Type (Portable ECG Systems, Wireless ECG Systems), By End-User (Hospitals and Clinics (often the dominant segment), Home Settings and Ambulatory Surgical Centers (ASCs), Diagnostic Centers, Long-Term Care Facilities). Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

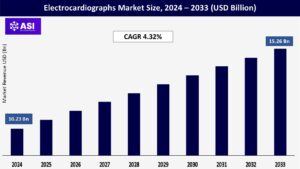

CAGR: 4.32%

Last Updated : March 17, 2026

The global electrocardiograph market size was valued at approximately USD 10.23 billion in 2024 and is projected to reach USD 15.26 billion by 2033, reflecting a compound annual growth rate (CAGR) of 4.32% over the forecast period 2025–2033.

This overview synthesizes insights from multiple market research reports to provide a comprehensive perspective on the Electrocardiograph Market for the period 2024-2033. While it provides a broad understanding of the market’s direction and key trends, readers seeking deeper insights, such as detailed market share data, competitive analysis, and regional dynamics, are encouraged to refer to the complete reports from the sources for a more comprehensive view.

One of the most important factors driving the growth of the electrocardiograph market is the rising global burden of heart-related conditions. Diseases like arrhythmias, heart attacks, heart failure, and coronary artery disease are becoming increasingly common, largely due to modern lifestyle habits such as poor diets, lack of physical activity, and stress. Additionally, an aging population and a surge in related risk factors like obesity, diabetes, and high blood pressure are contributing to the problem. As a result, the need for ECG devices continues to grow, since they play a vital role in the early detection, accurate diagnosis, and ongoing monitoring of these cardiac conditions.

Ongoing innovation is playing a key role in driving the growth of the electrocardiograph market. One major trend is the miniaturization of ECG devices; today’s models are becoming smaller, more portable, and easier to use, making them ideal not just for hospitals, but also for home care, remote clinics, and even personal use. Another advancement is wireless connectivity, which allows real-time data to be transmitted directly to healthcare providers. This makes remote monitoring more effective and expands access to cardiac care, especially in underserved areas. Additionally, ECG functionality is being integrated into smartwatches and wearable fitness trackers, bringing heart monitoring into the daily lives of more consumers and supporting ongoing health tracking. Finally, improvements in sensor technology and user-friendly design are making ECG devices more accurate and accessible, even for non-specialist users.

High-end ECG machines, especially those equipped with advanced features like AI integration, real-time remote monitoring, or multi-lead capabilities, often come with a hefty price tag. For many healthcare facilities, particularly smaller clinics or those in developing regions, this cost can be a major hurdle to adoption. But it’s not just the upfront investment that’s a concern. Ongoing expenses related to maintenance, calibration, and software upgrades can add up over time, making it difficult for some providers to keep these systems running efficiently. As a result, the high cost of ownership remains a significant challenge for the broader adoption of advanced ECG technologies.

Although ECG devices are becoming easier to use, interpreting the results, especially when it comes to detecting subtle or complex heart abnormalities, still demands the expertise of well-trained cardiologists or technicians. Unfortunately, there’s a shortage of such skilled professionals, particularly in rural or underserved regions, which can limit the effective use of ECG technology even when the devices themselves are available. While advancements in AI are helping bridge this gap by offering preliminary analysis, human judgment remains essential for accurate diagnosis and critical clinical decisions.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Resting ECG Systems Holter Monitors Stress ECG Systems Event Recorders Portable ECG Stationary ECG ECG Patches |

| By Lead Type |

Single-Lead ECG 2-Lead ECG 3-Lead ECG 6-Lead ECG 12-Lead ECG |

| By Technology Type |

Portable ECG Systems Wireless ECG Systems |

| By End User |

Hospitals and Clinics (often the dominant segment) Home Settings and Ambulatory Surgical Centers (ASCs) Diagnostic Centers Long-Term Care Facilities |

| Key Players |

AliveCor Inc. Allengers Medical Systems Limited BPL Medical Technologies CompuMed Inc. Fukuda Denshi Co. Ltd. General Electric Company (GE HealthCare) Hill-Rom Holdings Inc. (Baxter International Inc.) Innomed Medical Inc. Koninklijke Philips N.V. Midmark Corporation Nihon Kohden Corporation OSI Systems Inc. Schiller AG. Shenzhen Mindray Bio-Medical Electronics Co. Ltd. BioTelemetry (now part of Philips) iRhythm Technologies Medtronic |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Electrocardiographs Market is categorized by product type, by lead type, by technology, and by end-user. Each segment is rapidly evolving, with different areas of the industry growing at their own pace and shifting in how much of the market they represent. The Electrocardiographs (ECG) market is typically segmented to provide a more granular understanding of its dynamics, identifying key growth areas and dominant segments.

The ECG device market can be broadly categorized based on how the devices are used and their specific functions. Resting ECG systems are the most commonly used type, typically found in clinics and hospitals, and they record the heart’s electrical activity while the patient is at rest. These systems, often 12-lead, are essential tools for routine exams and emergency diagnostics, making them the largest and most established segment due to their affordability and ease of use. Holter monitors, on the other hand, are portable devices that continuously track heart rhythms over 24 to 48 hours or even longer, while patients go about their normal activities. With the rising need to monitor irregular or intermittent heart issues, this segment is growing quickly, supported by innovations in data storage and analysis.

Stress ECG systems are used during physical activity, such as walking on a treadmill, to detect heart conditions that might only appear during exertion. This segment remains stable and vital for diagnosing specific exercise-induced heart problems. Event recorders are another portable option, allowing patients to record their heart activity when they feel symptoms. Some models continuously record and only save data when triggered. These are becoming increasingly popular for identifying sporadic issues that might be missed by short-term monitors like Holters. A more advanced option is Mobile Cardiac Telemetry (MCT) systems, which automatically detect and send abnormal heart activity to a remote monitoring center.

With their longer monitoring duration, real-time data transmission, and wearable design, MCTs are seeing strong growth, especially as remote patient care becomes more widespread. Implantable loop recorders (ILRs) are designed for long-term monitoring, often for years, by being placed under the skin. They’re especially useful for tracking rare or unexplained cardiac events, making this a smaller but steadily growing niche. Finally, ECG patches have emerged as one of the fastest-growing segments. These lightweight, adhesive patches are either disposable or reusable and offer continuous monitoring, often connecting to smartphones for easy tracking. Their comfort, simplicity, and integration with AI tools make them a favorite in wearable healthcare, particularly for outpatient and home use. This segment is booming thanks to the growing demand for flexible, remote, and user-friendly cardiac monitoring solutions.

ECG devices can also be categorized based on the number of electrical leads they use to capture the heart’s activity, which directly impacts the level of detail provided. Single-lead ECGs are the most basic type, typically found in consumer wearables like smartwatches and handheld monitors. While they offer limited data, their simplicity, portability, and effectiveness for basic screening, especially for detecting arrhythmias, make them highly popular, particularly in personal health monitoring. As a result, they are expected to lead the market in terms of unit volume. 3-lead ECGs provide a slightly more detailed view and are often used in hospitals for continuous rhythm monitoring, especially in emergency or critical care settings. Moving up, 5-lead ECGs offer even greater insight and are a common choice in clinical environments where more comprehensive monitoring is needed without the complexity of a full 12-lead system. 6-lead ECGs strike a balance between portability and diagnostic value.

They’re gaining traction in wearable and smartphone-connected devices, making them ideal for routine check-ups and ongoing monitoring in outpatient or home care settings. At the high end of the spectrum is the 12-lead ECG, considered the gold standard in clinical diagnostics. It provides a complete, detailed view of the heart’s electrical activity from multiple angles, making it indispensable for diagnosing conditions like myocardial ischemia or complex arrhythmias. While not as portable, it remains the most valuable in terms of diagnostic accuracy and continues to hold the largest share of revenue among traditional ECG systems.

ECG devices can also be segmented based on their design and how they connect with other systems. Portable ECG systems, including handheld units and compact, often wireless carts, are becoming increasingly popular thanks to the growing demand for home healthcare and remote monitoring. Their ease of use and mobility make them ideal for settings beyond traditional hospitals. Within this category, wireless ECG systems are seeing rapid growth, as they allow seamless data transmission to smartphones, cloud platforms, or central monitoring stations, making them essential for telemedicine and real-time remote care.

Wearable ECG devices, such as smartwatches, patches, and chest straps, represent one of the fastest-growing segments. These offer continuous, non-intrusive heart monitoring, aligning perfectly with consumer health trends and the rise of preventive cardiology. On the more specialized end are implantable ECG devices, like Implantable Loop Recorders (ILRs), which are placed under the skin to provide long-term, continuous monitoring—particularly valuable for detecting rare or unpredictable cardiac events.

The ECG device market can also be segmented based on the primary settings where these devices are used. Hospitals and clinics remain the largest and most established end-user group. Their high patient volumes, need for comprehensive diagnostics, and ability to manage everything from emergency care to pre- and post-operative cardiac assessments make them central to ECG usage. These facilities are typically equipped with advanced infrastructure and are capable of handling a wide spectrum of cardiovascular conditions. Meanwhile, home settings and ambulatory surgical centers (ASCs) are seeing rapid growth.

The ongoing shift toward home-based care, combined with the rising popularity of remote monitoring and wearable ECG devices, is making cardiac diagnostics more accessible and convenient. ASCs, known for their cost-efficiency and streamlined procedures, are also playing a growing role in delivering outpatient cardiac care.

Diagnostic centers represent another important segment, specializing in a range of diagnostic services, including ECG evaluations. Often acting as referral hubs from primary care, these centers provide essential testing services and contribute significantly to the market. Beyond these, a diverse group of other end users, including long-term care facilities, urgent care centers, sports medicine clinics, research institutions, and even individual consumers, are increasingly adopting ECG technologies. As access points to healthcare expand and more people become proactive about heart health, this broad category is gaining momentum, particularly with the rise of user-friendly, direct-to-consumer ECG solutions.

The regional landscape of the Electrocardiographs (ECG) market shows clear differences across the globe, shaped by each area’s unique mix of healthcare infrastructure, disease burden, access to technology, and overall economic development. In more developed regions, advanced healthcare systems and higher awareness of cardiac health drive strong demand for sophisticated ECG technologies.

Meanwhile, in emerging markets, growing investments in healthcare, rising rates of heart disease, and the need for affordable, accessible diagnostic tools are fueling rapid growth. These regional differences highlight how local needs and capabilities influence the adoption and expansion of ECG devices worldwide.

North America continues to lead the global ECG market, holding the largest share of about 39.2% in 2024, with an even more dominant position in specific segments like ECG patches and Holter monitors, where it accounts for roughly 66.5%. This strong market position is underpinned by several key factors. First and foremost, the region faces a high and rising prevalence of cardiovascular diseases, with over 48 million people affected in 2024 alone. This creates a constant need for reliable and frequent cardiac diagnostics. North America also benefits from an advanced healthcare infrastructure, marked by high levels of healthcare spending and a strong emphasis on preventive care and early diagnosis both of which drive the uptake of sophisticated ECG technologies.

The region is quick to embrace innovation, with widespread adoption of cutting-edge tools such as AI-powered ECG systems, wearable devices, and remote patient monitoring. For example, in 2024, Medicare in the U.S. expanded its coverage to include RPM and AI-enabled ECG technologies, further accelerating their use. Another major advantage is the presence of many leading ECG device manufacturers headquartered in North America, which keeps the region at the forefront of product development and market growth. Additionally, a steadily aging population adds to the demand for routine cardiac monitoring. Within the region, the United States stands out as the key driver—thanks to its advanced healthcare system, large patient population, and openness to medical innovation.

Europe holds the second-largest share of the global ECG market after North America and is expected to see steady growth in the coming years. This momentum is largely driven by the high burden of cardiovascular diseases, which continue to be a leading cause of death and illness across the continent. As a result, there’s a strong and ongoing need for effective diagnostic tools like ECGs. The region is also seeing increased adoption of advanced technologies, including portable, wireless, and AI-integrated ECG devices, which are improving both accessibility and diagnostic accuracy.

An aging population, mirroring trends in North America, is further boosting demand for regular cardiac monitoring. Europe also benefits from generally favorable reimbursement policies in many countries, which help support the use of newer and more sophisticated ECG technologies. Additionally, there’s a growing emphasis on outpatient and ambulatory care, as healthcare systems prioritize preventive approaches and cost-effective solutions, leading to increased use of ECG monitoring in non-hospital settings. However, the market does face a few challenges, such as saturation in some traditional segments and variability in reimbursement policies across different countries. Despite this, leading economies like Germany, the UK, France, Italy, and Spain remain strongholds in the European ECG market, thanks to their robust healthcare infrastructures and high levels of healthcare investment.

The Asia-Pacific region is emerging as the fastest-growing market for ECG devices, with some forecasts predicting a remarkable CAGR of up to 16% in ECG-related electrophysiology from 2024 to 2033. This rapid growth is fueled by a combination of factors. A large and increasingly aging population across the region has led to a rising prevalence of cardiovascular diseases, creating a substantial need for effective diagnostic solutions. At the same time, both governments and the private sector are ramping up investments in healthcare infrastructure, particularly in fast-developing countries. Awareness around cardiovascular health is steadily improving, encouraging more people to seek early diagnosis and treatment. Additionally, the region’s growing middle class, especially in countries like China and India, is driving demand for higher-quality healthcare services and technologies.

While Asia-Pacific may still trail North America in adopting some of the most advanced ECG systems, there is growing momentum in the uptake of portable and cost-effective solutions, and increasing interest in AI-based diagnostics. However, challenges remain. The high cost of advanced ECG devices can limit access in price-sensitive markets, and a shortage of trained cardiologists and technicians—particularly in rural and semi-urban areas—can hinder effective device usage. The healthcare landscape in the region is also highly fragmented, with significant disparities in access and care quality across countries. Moreover, navigating the diverse and evolving regulatory environments in APAC can be complex for manufacturers.

Despite these obstacles, the region holds enormous untapped potential. Major countries like China and India are at the forefront of this growth, driven by their massive populations and expanding healthcare sectors. Meanwhile, Japan, South Korea, and Australia continue to contribute significantly, thanks to their advanced medical infrastructure and strong focus on technological innovation.

The Middle East and Africa (MEA) region is seeing steady growth in the ECG market, with particularly strong momentum in mobile ECG devices, which are projected to grow at a CAGR of 8.8% between 2024 and 2030. Several factors are driving this upward trend. The prevalence of cardiovascular diseases is rising across the region, fueled by rapid urbanization and shifting lifestyles. At the same time, healthcare infrastructure is steadily improving, especially in Gulf Cooperation Council (GCC) countries like Saudi Arabia and the UAE, where significant investments are being made to modernize and expand healthcare services.

Healthcare spending is also on the rise, with both governments and private sectors allocating more resources to improve care delivery. This is boosting demand for portable and mobile ECG solutions, which are especially valuable in addressing the challenges of healthcare access in remote or underserved areas. However, the region still faces a number of obstacles. Access to advanced healthcare remains limited in many parts, particularly in sub-Saharan

Africa, where disparities in care are more pronounced. Political and economic instability in some countries can slow down healthcare investments, and a shortage of skilled healthcare professionals poses an additional challenge. Moreover, many MEA countries rely heavily on imported medical equipment, which can drive up costs and limit availability. Despite these challenges, key markets such as Saudi Arabia, the UAE, and South Africa are leading the way, thanks to their relatively advanced healthcare infrastructure, stronger economies, and higher levels of disposable income, positioning them as central players in the region’s ECG market growth.

The market was valued at USD 10.23 billion in 2024.

The market is projected to grow at a CAGR of 4.32% from 2025 to 2033.

Hospitals segment holds the largest market share.

Asia-Pacific region is expected to witness the highest growth rate.

Major players include GE Healthcare, Koninklijke Philips N.V., Nihon Kohden Corporation, and Shenzhen Mindray Bio-Medical Electronics Co.,Ltd.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Electrocardiographs Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Electrocardiographs Market, By Lead Type

5.3 Electrocardiographs Market, By Technology

5.4 Electrocardiographs Market, By End User

6.1 North America Electrocardiographs Market, By Country Type

6.1.1 Electrocardiographs Market, By Product Type

6.1.2 Electrocardiographs Market, By Lead Type

6.1.3 Electrocardiographs Market, By Technology

6.1.4 Electrocardiographs Market, By End User

6.2 U.S.

6.2.1 Electrocardiographs Market, By Product Type

6.2.2 Electrocardiographs Market, By Lead Type

6.2.3 Electrocardiographs Market, By Technology

6.2.4 Electrocardiographs Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping