Ethyl Tertiary Butyl Ether Market

Ethyl Tertiary Butyl Ether Market & Trends Analysis Report, By Production Method (Synthetic ETBE, Bio-ETBE), By Application (Gasoline Blending, Aviation Fuels), By End User (Oil Refineries, Fuel Distributors)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

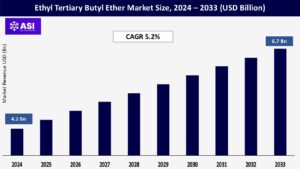

CAGR: 5.2%

Last Updated : March 16, 2026

The global ethyl tertiary butyl ether (ETBE) Market size was valued at approximately USD 4.2 billion in 2024 and is projected to reach USD 6.7 billion by 2033, growing at a CAGR of 5.2% during the forecast period.

ETBE is a high-octane oxygenate additive derived from the reaction of isobutylene with ethanol, widely used in gasoline blending to improve combustion efficiency and reduce harmful emissions. Compared to MTBE (Methyl Tertiary Butyl Ether), ETBE offers better environmental performance, particularly due to its higher renewable ethanol content, making it a favored choice under various biofuel mandates.

Growth is driven by rising ethanol production, global initiatives for cleaner fuels, and stringent fuel quality regulations in Europe, Japan, and other regions.

In order to reduce carbon monoxide (CO), nitrogen oxides (NOx), and particle emissions, governments in parts of Asia, Europe, and Japan require gasoline to have a higher oxygen content.

With its high octane value and renewable ethanol-derived component, ethyl tert-butyl ether (ETBE) is essential to fulfilling these requirements while preserving engine performance. Key factors influencing market demand include laws like Japan’s biofuel blending requirements and the EU Renewable Energy Directive (RED II).

The use of bioETBE, which is made from bioethanol, is increasing as a result of the increased emphasis on environmentally friendly gasoline additives. In addition to helping achieve carbon emission reduction targets, bio-ETBE lessens dependency on oxygenates derived from fossil fuels, such as methyl tert-butyl ether (MTBE).

Market penetration has been further accelerated by the introduction of advantageous blending credits and incentives by nations like France and Spain to promote the use of bio-based ETBE.

The price of raw materials, especially ethanol and isobutylene, has a significant impact on the cost of producing ETBE. The dynamics of the crude oil market, shifts in biofuel blending regulations, and variations in agricultural production all affect the price of ethanol.

Refinery operations and petrochemical production cycles are intimately related to isobutylene availability, therefore changes in output or interruptions in supply can have a direct impact on the stability of the ETBE market.

Other oxygenates that compete with ETBE include synthetic octane boosters, methyl tert-butyl ether (MTBE) in some non-EU markets, and direct ethanol blending (E10/E15).

Because direct blending requires fewer processing steps, it is frequently the favored option in nations with developed ethanol infrastructure, which may restrict ETBE’s market growth.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Production Method |

Synthetic ETBE Bio-ETBE |

| By Application |

Gasoline Blending Aviation Fuels |

| By End-User |

Oil Refineries Fuel Distributors |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Ethyl Tertiary Butyl Ether Market is segmented by Production Method (Synthetic ETBE, Bio-ETBE), By Application (Gasoline Blending, Aviation Fuels), By End User (Oil Refineries, Fuel Distributors).

Each factor plays a crucial role in enhancing patient safety, increasing the adoption of self-administered anticoagulant therapies, and supporting the development of more convenient, prefilled drug delivery systems that streamline treatment in the management of thromboembolic and cardiovascular conditions.

Synthetic ETBE (Largest Segment)

The largest segment of synthetic ETBE This sector, which uses fossil-based ethanol and isobutylene for manufacturing, has the most market share because of its well established refinery integration, steady supply of feedstock, and cheaper production costs than bio-based substitutes. In areas without strict requirements for biofuel mixing, it continues to be the recommended choice.

Bio-ETBE

Made from renewable bioethanol, this market is expanding quickly, especially in Europe and Japan, where carbon reduction goals, advantageous blending credits, and incentives for renewable fuels promote uptake. Markets seeking to reduce greenhouse gas emissions and dependence on oxygenates derived from fossil fuels are favoring bio-ETBE more and more.

Gasoline Blending (Largest Application)

ETBE is primarily used as an oxygenate in vehicle fuels to assist in fulfilling strict pollution standards and octane rating criteria. It is a popular option in areas with stringent fuel quality rules due to its high blending efficiency and compatibility with the current fuel infrastructure.

Aviation Fuels

ETBE is being assessed and included into bio aviation fuel blends in this new application area to improve combustion efficiency, lower particle emissions, and preserve low sulfur content. As the aviation industry accelerates its transition to sustainable fuel alternatives, this area is anticipated to gain pace.

Oil Refineries

The main producers and integrators of ETBE are oil refineries, which include it straight into gasoline pools during the fuel formulation and refining operations. Efficient large-scale manufacturing is ensured by their well-established infrastructure and availability of feedstocks like ethanol and isobutylene.

Fuel Distributors

Fuel distributors are responsible for the mixing, storing, and supplying of ETBE-enriched fuels to the wholesale and retail markets. They are essential in providing oxygenated gasoline to final customers and guaranteeing adherence to local fuel quality regulations.

Due to biofuel blending requirements under the EU Renewable Energy Directive (RED II), France, Spain, and Italy are leading the world in the adoption of ETBE. Strong ethanol output, well-established refinery infrastructure, and a strong emphasis on lowering emissions from the transportation sector all help the area. Europe is positioned as a major exporter since it has the largest proportion of the world’s bio-ETBE capacity.

Japan continues to be a significant ETBE customer, substituting it for direct ethanol blending as the principal biofuel addition to improve fuel stability. Adoption is increasing in emerging economies like South Korea and Thailand as a result of stricter fuel quality upgrades, carbon reduction goals, and urban air quality improvement initiatives.

Because direct ethanol blending is preferred in this region (E10/E15), adoption is still low when compared to other regions. Nonetheless, as biofuel regulations grow, there are prospects in specialized premium fuel markets and possible incorporation into sustainable aviation fuel (SAF) formulas.

Latin America and the Middle East: To increase fuel blending flexibility, Brazil and Mexico are investigating ETBE as a supplemental oxygenate in addition to their current ethanol projects. Countries in the GCC, including Saudi Arabia and the United Arab Emirates, are evaluating ETBE’s capacity to assist refinery diversification plans and satisfy international clean fuel export regulations.

The global ETBE market size was valued at USD 4.2 billion in 2024.

The global ETBE market is projected at a CAGR of 5.2%.

The Gasoline blending application dominates the market.

Asia-Pacific, driven by Japan’s biofuel policies and emerging markets adopting clean fuel mandates

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Ethyl Tertiary Butyl Ether Market, By Production Method

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Ethyl Tertiary Butyl Ether Market, By Application

5.3 Ethyl Tertiary Butyl Ether Market, By End-User

6.1 North America Ethyl Tertiary Butyl Ether Market , By Country

6.1.1 Ethyl Tertiary Butyl Ether Market, By Production Method

6.1.2 Ethyl Tertiary Butyl Ether Market, By Application

6.1.3 Ethyl Tertiary Butyl Ether Market, By End-User

6.2 U.S.

6.2.1 Ethyl Tertiary Butyl Ether Market, By Production Method

6.2.2 Ethyl Tertiary Butyl Ether Market, By Application

6.2.3 Ethyl Tertiary Butyl Ether Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping