Europe Lidocaine Market

Europe Lidocaine Market size, share & trends analysis report By formulation (Injections, Creams, Ointments, Gel), By Application (Dentistry, Cardiac Arrhythmia, Epilepsy, Cosmetic Surgery, General Surgery), By Distribution Channel (Hospitals Outlets, Retail Pharmacies) Industry analysis report regional outlook growth potential, price trends, competitive market share & forecast period 2025-2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

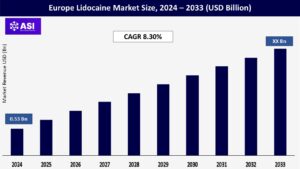

CAGR: 8.30%

Last Updated : July 25, 2025

The Europe Lidocaine Market was around USD 0.53 billion in 2024 and is expanding at a CAGR 8.30% for the forecast period (2025-2033). The lidocaine market in Europe is critical in order to enable efficient pain management and local anesthesia during medical, dental, and cosmetic procedures. It is particularly important for applications involving surgery, dermatological treatments, and relief from chronic pain.

Market growth will be propelled by rising demand for minimally invasive procedures, an aging population on the rise, and the increasing application of cosmetic treatment throughout the region.

The European region is experiencing an upward trend in elderly population, and Eurostat puts the figure at approximately 30% of EU residents aged 65 and above by the year 2050. This demographic change is directly related to a rise in age-related chronic conditions like osteoarthritis, diabetic neuropathy, and lower back pain. These conditions necessitate regular and potent pain management mechanisms, of which lidocaine forms an integral part. Lidocaine, particularly in topical or patch formulations, is commonly utilized to alleviate nerve pain and discomfort tied to aging. Its low side effects and local application, therefore, render it a safer option compared to systemic analgesics such as opioids that are toxic in old patients.

For instance, the application of lidocaine patches for postherpetic neuralgia, a prevalent pain syndrome in the elderly, has become routine practice in British and German geriatric care. As home healthcare gains popularity throughout Europe, demand for simple pain relief products such as lidocaine patches and ointments is growing rapidly. Governments and insurance companies are also financing non-opioid pain management, further assisting the usage of lidocaine in elderly care programs.

The European aesthetic medicine market is expanding with rapid growth, as more and more consumers look for minimally invasive cosmetic treatments to beautify their looks and increase self-esteem. ISAPS states that nations such as France, Italy, and the UK have experienced tremendous growth in treatments such as dermal fillers, laser treatment, and micro needling. Lidocaine is widely applied in these treatments to numb the skin and reduce discomfort before and after procedures. It is usually mixed into filler formulations or used topically before treatments. The increasing popularity of aesthetic treatments among millennials and middle-aged people fueled by social media culture and the trend of cosmetic improvement has affected the demand for lidocaine-containing anesthetics directly.

Patients are a priority for spas and dermatologists, and lidocaine provides smoother, painless procedures that enhance client satisfaction. For example, it is common to find Parisian and Milanese clinics touting “numbed” or “pain-free” treatments as an upscale service, employing lidocaine as the major anesthetic drug. In a market where the cosmetic business is projected to increase continuously, the use of lidocaine as complementary agent in non-surgical procedures is becoming a requirement. Market Restraints Strict Regulatory Environment and Delayed Approvals.

The European market for lidocaine is severely challenged by the continent’s tightly regulated pharmaceutical and medical environment. Lidocaine products have to endure extensive testing, documentation, and approval by health agencies like the European Medicines Agency (EMA) in order to be sold. This encompasses thorough evaluation of safety, effectiveness, and quality of manufacture. Although these controls guarantee public protection, they also cause longer approval times and rising costs for manufacturers. Smaller firms and generic manufacturers tend to struggle with the intricacies of compliance procedures, which can delay product introductions or discourage market entry in the first place. New EU regulations—e.g., revisions to the Medical Device Regulation (MDR) and more stringent criteria on topical anesthetics—have introduced uncertainty and added to regulatory costs.

For instance, in 2022, some of the lidocaine-containing topical products were withdrawn from some European markets for a short term following non-compliance concerns with labeling and dosing. This regulatory inflexibility, although put in place to safeguard patients, can limit innovation, reduce access to products, and dampen market growth, particularly for newer or more sophisticated formulations that need more scrutiny.

The European market for lidocaine is confronted with serious challenges as a result of Europe’s restrictive pharmaceutical and medical regulatory climate. Any product incorporating lidocaine has to be stringently tested, documented, and approved by health organizations like the European Medicines Agency (EMA) for them to be sold. This involves comprehensive examination of safety, efficacy, and quality of manufacture.

While these regulations make the public safer, they also contribute to longer approval times and higher expenses for manufacturers. Small businesses and generic companies are frequently hampered by the complexity of compliance processes, which can postpone product release or even discourage market entry. Changes in EU regulations, including revising the Medical Device Regulation (MDR) and tightening regulations on topical anesthetics, have also led to uncertainty and further regulatory burden. For instance, in 2022, a number of lidocaine-containing over-the-counter topical products were suddenly removed from a few European markets on grounds of noncompliance with labeling and dosing requirements. Such regulatory inflexibility, although for protecting patients, can hinder innovation, reduce product access, and decelerate market development, particularly for newer or higher-tech formulations that need further examination.

| Report Metric | Details |

|---|---|

| By Formulation |

Injections Creams Ointments Gel |

| By Application |

Dentistry Cardiac Arrhythmia Epilepsy Cosmetic Surgery General Surgery |

| By Distribution Channel |

Hospitals Outlets Retail Pharmacies |

| Key Players |

|

| Europe |

U.K. |

Among the different formulations, injections command the largest share of the European lidocaine market because of their extensive application in surgery and dental procedures where rapid-acting, deep anesthesia is needed. Lidocaine injections are a common feature of operating theaters, out-patient surgery, and dental surgeries in Germany, the UK, and France. Creams and ointments are also extensively applied, particularly for dermatological purposes and minor skin procedures.

These products are favored due to ease of application and reduced systemic absorption. Gels are increasingly being used in cosmetic dermatology and for the treatment of minor injuries, as they are popular for fast absorption and non-greasy consistency. The increasing use of over-the-counter lidocaine gels for localized pain in muscles and joints is boosting growth in this segment. Lidocaine injections represented around 48.1% of the overall market revenue in 2023, while gels will be driven at a CAGR of 7.9% during the period between 2024 and 2030 with rising demand in cosmetic as well as homecare uses.

The largest application sector for lidocaine is general surgery, fueled by its critical use in local anesthetic applications in outpatient and minimal-invasive surgeries. Hospitals and outpatient surgical centers routinely depend on lidocaine for procedure efficiency and patient comfort. Dentistry is also a major segment, with lidocaine being widely utilized in root canals, extractions, and cavity fillings.

Dental-specific lidocaine injections and topical anesthetics enable steady growth among European dental practices. Cosmetic surgery has witnessed significant growth, especially in urban areas such as Paris, Milan, and London, where demand for dermal fillers and laser therapy is on the rise. The use of lidocaine to alleviate pain and discomfort in such procedures is essential for patient satisfaction. Cardiac arrhythmia therapy employs lidocaine intravenously as a second-line antiarrhythmic, although use is more specialized and hospital-based. Although epilepsy is not a direct treatment application for lidocaine, its use in neurology is primarily experimental or adjunctive. General surgery and dentistry collectively contributed more than 60% of overall lidocaine utilization in 2024, which reflects high medical reliance.

Hospital channels control lidocaine distribution in Europe, with sales of more than 56.7% of total market revenue in 2024. This is a result of lidocaine’s frequent application in surgery, emergency treatment, and inpatient cases that need prescription and professional handling. Hospitals buy in bulk from licensed pharma suppliers, which guarantees consistent demand. Chain and independent retail pharmacies are the second-largest channel, especially for over-the-counter and topical preparations such as creams, gels, and patches. Such products are commonly prescribed for transient relief of pain, post-treatment care, and managing chronic pain. Community pharmacies are major touchpoints in Spain and Italy for elderly groups requiring non-prescription lidocaine preparations.

The retail pharmacy channel is anticipated to grow steadily on the back of increasing consumer health consciousness and self-care trends, particularly in case of musculoskeletal pain and dermatological use. With e-prescriptions and online pharmacy networks growing stronger, access to both prescription and OTC lidocaine is likely to increase, further accelerating retail penetration

North America is still the market leader in the global telemedicine market. In 2024, the region held a share of about 43.1% of the total global market share due to developed healthcare infrastructure, widespread digital health technology adoption, and favorable government policies. The U.S. telemedicine market alone was worth USD 32.3 billion in 2024 increasing at a CAGR of 18.25%. High incidence of chronic diseases, an ageing population, and rising demand for superior technology are the factors attributing to this growth.

Europe is also a leading region in terms of telemedicine market share, with the UK, Germany, and France taking top positions in adoption thanks to conducive government policy and rising health digitization. The region is further supported by high-developed healthcare systems and growing efforts towards minimizing health expenses via digital technologies. National health policy implementation and reimbursement for telemedicine have further driven adoption across the continent.

The Asia-Pacific region has the fastest-growing telemedicine market, with an estimated CAGR of 19.5% from 2024 to 2030. The growth is fueled by greater internet penetration, a high patient population, and growing demand for affordable healthcare services. Government programs in nations such as India and China to encourage telemedicine are also fueling this expansion.

Latin America telehealth market valued at USD xx billion in 2023 is and registering a CAGR of 24.1%. The high prevalence of chronic conditions, ageing population, and rise in adoption of digital healthcare solutions drive growth in the region. Brazil and Mexico are forerunners with high investment in telehealth infrastructure and accommodating regulations.

The telehealth market in the Middle East and Africa was valued at USD xx billion in 2024 and is expected to grow at a CAGR of 26.8% during the period 2025-2030. Improving internet connectivity, rising smartphone penetration, and initiatives by governments such as Saudi Arabia’s Vision 2030 are fueling the digitalization of healthcare in the region. The UAE led with the highest portion of 24.8% in 2024, led by initiatives to disseminate awareness and adopt telehealth platforms by patients and healthcare providers.

The Europe Lidocaine Market was valued at USD 0.53 billion in 2024.

The Europe lidocaine market is projected to grow at CAGR of 8.30 % from 2025 to 2033.

Dental procedures holds the largest market share of Europe Lidocaine Market.

Germany and the united kingdom region is expected to witness the highest growth rate

Some of the major players in the Europe Lidocaine Market are Pfizer Inc, Teva Pharmaceutical Industries Ltd, Viatris Inc. (formerly Mylan N.V.).

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Europe Lidocaine Market, By Formulation

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Europe Lidocaine Market, By Application

5.3 Europe Lidocaine Market, By Distribution Channel

6.1 U.K.

6.2 Germany

6.3 France

6.4 Spain

6.5 Italy

6.6 Russia

6.7 Nordic

6.8 Benelux

6.9 The Rest of Europe

7.1 Global Market Share (%) By Players

7.2 Market Ranking By Revenue for Players

7.3 Competitive Dashboard

7.4 Product Mapping