Fipronil Market

Fipronil Market & Trends Analysis Report, By Product Type (Gel, Granules, Liquid Formulations), By Application (Agriculture, Veterinary, Household and Structural Pest Control), By End Use (Farmers, Pest Control Operators, Pet Owners)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 4.2%

Last Updated : March 16, 2026

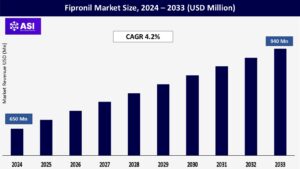

The global Fipronil Market size was valued at approximately USD 650 million in 2024 and is projected to reach USD 940 million by 2033, growing at a CAGR of 4.2% during the forecast period (2025–2033).

A broad-spectrum insecticide belonging to the phenyl pyrazole chemical family, fipronil is extensively utilized in home, veterinary, and agricultural pest management. Fipronil works by interfering with the insect’s central nervous system and is well-known for its efficacy against ants, cockroaches, termites, fleas, and beetles.

greater pest resistance to older pesticides, increased crop protection needs, greater pet health awareness, and the expansion of urban pest management services are some of the main growth factors. Significant obstacles are presented by its contentious environmental character and regulatory limitations, nevertheless.

The usage of high-efficacy pesticides like fipronil is growing as a result of the strain that growing food demand and declining cultivable area are placing on global agricultural systems.

Fipronil works especially well against pests that are known to seriously harm crops like rice, sugarcane, corn, cotton, and potatoes, including locusts, stem borers, leafhoppers, rootworms, and termites. Farmers in Asia-Pacific and Latin America favor it because of its capacity to offer durable residual control.

Ownership of companion animals has significantly increased in both developed and developing nations, particularly in metropolitan areas. This movement is also raising awareness of zoonotic disease prevention, flea and tick control, and pet care.

Veterinary professionals frequently advise using fipronil-based products, such as collars, shampoos, sprays, and spot-on treatments, to control parasites. Demand is also being boosted by the availability of over-the-counter products and rising pet healthcare expenditures.

Fipronil’s ecotoxicological profile, in particular its detrimental effects on pollinators including bees, aquatic creatures, and soil microfauna, has drawn increased attention from around the world. Because fipronil contributes to bee colony collapse disorder (CCD), the European Union has prohibited its use in agriculture.

A number of other nations have enforced stringent application restrictions, required buffer zones, or pre-market risk evaluations.

For producers, these requirements make post-market surveillance, formulation adjustment, and registration more expensive and complicated.

Furthermore, regulators are being forced to tighten limitations due to mounting criticism from NGOs and environmental activists, which is limiting the uptake of products in a number of high-potential areas.

Certain pest species, such as cockroaches, fleas, and other crop-damaging insects, have developed resistance to fipronil as a result of repeated and unmonitored use. In addition to decreasing its effectiveness, this forces consumers to take larger dosages or convert to alternative or synergistic insecticides, which raises the expense of treatment.

Integrated pest management (IPM) tactics, which aim to use as few chemicals as possible, are likewise threatened by pest resistance. Product rotation, combination treatments, and resistance management programs are therefore increasingly essential, which complicates things for end users and slows market expansion.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Gel Granules Liquid |

| By Application |

Agriculture Veterinary Household/Urban Pest Control |

| By End-Use |

Farmers Pest Control Operators Pet Owners |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Fipronil Market is segmented by Product Type (Gel, Granules, Liquid Formulations), By Application (Agriculture, Veterinary, Household and Structural Pest Control), By End Use (Farmers, Pest Control Operators, Pet Owners).

Each factor plays a crucial role in enhancing patient safety, increasing the adoption of self-administered anticoagulant therapies, and supporting the development of more convenient, prefilled drug-delivery systems that streamline treatment for thromboembolic and cardiovascular conditions.

Gels are frequently used to manage pests in homes and businesses, especially ants and cockroaches. They are ideal for indoor settings like homes, restaurants, businesses, and hospitals because of their precise targeting, localized application, and low odor. Their long-lasting effectiveness, convenience of use, and safety in restricted locations are the main reasons for their rising popularity.

Termite treatments, lawn management, and agricultural soil applications are the main uses for granular formulations. For pests that live in or close to root zones, these formulations are favored due to their slow-release characteristics, decreased spread, and focused soil penetration. They are also frequently utilized in golf course upkeep and beautification.

Products containing liquid fipronil are adaptable and often utilized in both the veterinary and agricultural fields. For systemic pest control in crop protection, they are sprayed on or treated in seeds. Liquids are used in veterinary settings in spray-on drugs for cattle and poultry, as well as topical spot-on treatments for pets. Strong demand is a result of their quick response and simplicity in large-area applications.

With fipronil being used to manage pests in rice, sugarcane, corn, cotton, and potatoes, agriculture continues to be the major use segment. High-value crops can benefit from its long-lasting residual control and broad-spectrum effectiveness, particularly in areas where pest outbreaks are common. Its selective use is also being supported by the growing trend toward integrated pest control (IPM) systems.

Fipronil is a crucial active component in flea, tick, and lice prevention medications for dogs, cats, cattle, and poultry in veterinary medicine. It can be found in collars, shampoos, sprays, and spot-on treatments. Demand in this market is being sustained by rising pet ownership, zoonotic illness awareness, and animal welfare laws.

In urban settings, fipronil works quite well to get rid of termites, ants, and cockroaches. It is frequently used in commercial buildings, kitchens, warehouses, and construction foundations. Growing urbanization, consumer awareness, and government-sponsored sanitation initiatives are driving the segment’s growth in emerging nations.

Farmers are the primary users of fipronil for crop protection, particularly in Asia-Pacific, Latin America, and Africa. Granules and liquids are used in large-scale farming operations for soil and foliar pest control. With increasing adoption of yield-boosting agrochemicals, the segment is expected to see steady growth.

Professional pest control service providers extensively use gel and spray formulations of fipronil for effective pest management in urban and commercial spaces. The rise in outsourced pest control services, especially in sectors like hospitality, healthcare, and retail, is bolstering this user group.

Pet owners are major drivers of the veterinary application segment. The increasing number of companion animals and demand for convenient flea/tick control solutions have led to strong adoption of over-the-counter and prescription fipronil products. This segment is particularly strong in North America, Europe, and urban centers in Asia.

The fastest-growing market in Asia-Pacific is driven by China, India, and Southeast Asia. Demand is being driven by increased middle-class pet ownership, high agricultural activity, and rising pest resistance.

steady demand, especially in the US, for urban pest control and pet care. Environmental scrutiny and regulatory limitations, however, continue to be issues.

heavily restricted, with fipronil’s usage in agriculture partially prohibited. Nonetheless, it is still little use in veterinary and specialized applications.

In Brazil, Argentina, and Colombia, the agricultural sector is expanding, and more fipronil-based solutions are being used to preserve crops and control termites.

moderate development, particularly in South Africa and the Gulf area, due to the need for pest control in residential and agricultural settings.

The global Fipronil market size was valued at USD 650 million in 2024.

The global Fipronil market is projected at a CAGR of Approximately 4.2%

The segment that dominates the market is Agriculture.

Asia-Pacific region shows the highest growth potential

BASF, Bayer, Gharda Chemicals, Parijat Industries, Adama, and others.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Fipronil Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Fipronil Market, By Application

5.3 Fipronil Market, By End-Use

6.1 North America Fipronil Market , By Country

6.1.1 Fipronil Market, By Product Type

6.1.2 Fipronil Market, By Application

6.1.3 Fipronil Market, By End-Use

6.2 U.S.

6.2.1 Fipronil Market, By Product Type

6.2.2 Fipronil Market, By Application

6.2.3 Fipronil Market, By End-Use

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping