Gastrointestinal Drugs Market

Gastrointestinal Drugs Market Share & Trends Analysis Report, By Drug Class (Acid Neutralizers, Anti-diarrheal & Laxatives, Antiemetics, Anti-inflammatory Drugs, Biologics, Others), By Route of Administration (Oral, Parenteral, Rectal), By Application (Gastroesophageal Reflux Disease (GERD), Ulcerative Colitis, Crohn’s Disease, Irritable Bowel Syndrome, Constipation, Diarrhoea, Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), By End User (Hospitals, Clinics, Homecare Settings, Others) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

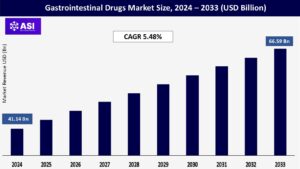

CAGR: 5.48%

Last Updated : November 22, 2025

The global gastrointestinal drugs market size was valued at approximately USD 41.14 billion in 2024 and is projected to reach USD 66.59 billion by 2033, growing at a CAGR of 5.48% during the forecast period (2025–2033).

The Gastrointestinal (GI) Drugs Market encompasses pharmaceutical products used to treat a wide range of disorders affecting the gastrointestinal tract, including the oesophagus, stomach, intestines, liver, gallbladder, and pancreas. These drugs are primarily used for conditions such as gastroesophageal reflux disease (GERD), irritable bowel syndrome (IBS), Crohn’s disease, ulcerative colitis, peptic ulcers, constipation, diarrhoea, and acid reflux.

Common drug classes in this market include antacids, proton pump inhibitors (PPIs), H2 receptor antagonists, laxatives, antiemetics, antidiarrheals, and anti-inflammatory agents. GI drugs are known for their properties such as acid-neutralizing effects (in antacids), suppression of gastric acid secretion (in PPIs and H2 blockers), and modulation of gut motility (in laxatives and antidiarrheals).

The market is driven by the increasing prevalence of gastrointestinal diseases due to sedentary lifestyles, poor dietary habits, and rising stress levels, along with the growing geriatric population and advancements in drug formulations such as delayed-release capsules and biologics.

One of the primary drivers of the gastrointestinal drugs market is the growing global burden of GI disorders such as GERD, irritable bowel syndrome (IBS), Crohn’s disease, and ulcerative colitis. Factors such as unhealthy diets, sedentary lifestyles, increased consumption of processed foods, alcohol, and stress are contributing to the widespread incidence of these conditions.

Additionally, the aging population more prone to chronic digestive problems further boosts demand. As these disorders significantly impact quality of life, the need for effective therapeutic interventions is growing steadily, propelling the market forward.

Innovation in drug development and formulation is another major growth driver. Pharmaceutical companies are investing heavily in the development of next-generation GI drugs, including biologics, biosimilars, and personalized medicine targeting inflammatory pathways.

Controlled-release tablets, orally disintegrating tablets, and targeted delivery systems improve patient compliance and therapeutic outcomes. These advancements not only enhance treatment efficacy but also attract investment and expand the market by providing better options for chronic and complex GI conditions.

A major restraint in the gastrointestinal drugs market is the growing concern over the side effects associated with long-term use of commonly prescribed medications such as proton pump inhibitors (PPIs), antacids, and laxatives.

Studies have linked PPIs with adverse effects including kidney disease, vitamin and mineral deficiencies, bone fractures, and increased susceptibility to infections. Similarly, overuse of laxatives can lead to dependency and impaired bowel function.

These safety concerns have led to increased regulatory scrutiny, lawsuits, and even product recalls in some cases. Such developments not only erode patient and physician trust but also limit market growth by shifting preferences toward non-pharmacological or alternative treatments like dietary changes, probiotics, and herbal remedies.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Drug Class |

Acid Neutralizers Anti-diarrheal & Laxatives Antiemetics Anti-inflammatory Drugs Biologics Others |

| By Route of Administration |

Oral Parenteral Rectal |

| By Application |

Gastroesophageal Reflux Disease (GERD) Ulcerative Colitis Crohn’s Disease Irritable Bowel Syndrome Constipation Diarrhoea Others |

| By Distribution Channel |

Hospital Pharmacies Retail Pharmacies Online Pharmacies |

| By End User |

Hospitals Clinics Homecare Settings Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Gastrointestinal Drugs Market is segmented by Drug class, Route of administration, Application, Distribution Channels and End User. Each factor plays a crucial role in improving patient outcomes, driving the demand for safer and more effective therapies, and encouraging innovation in drug delivery systems ultimately enhancing the management of a wide range of gastrointestinal disorders and promoting better digestive health.

Acid Neutralizers Includes antacids and proton pump inhibitors (PPIs) commonly used for acid reflux and GERD. High demand due to increasing cases of hyperacidity and related disorders. Anti-diarrheal & Laxatives Widely used for managing bowel irregularities such as chronic constipation and diarrhoea.

The segment is driven by the growing elderly population and sedentary lifestyles. Antiemetics These drugs help manage nausea and vomiting, often associated with GI infections, chemotherapy, or motion sickness. They play a critical supportive role in treatment regimens.

Anti-inflammatory Drugs Primarily used in inflammatory bowel diseases (IBD) like Crohn’s disease and ulcerative colitis. Demand is rising due to the chronic nature of these conditions. Biologics An emerging segment offering targeted therapies for moderate-to-severe cases of IBD. Biologics such as TNF inhibitors are increasingly preferred for long-term management. Others Includes miscellaneous drugs such as prokinetics, antispasmodics, and herbal supplements that support gastrointestinal health.

Oral Dominates the market due to ease of administration, patient compliance, and availability in tablet, capsule, or liquid form for a broad range of GI conditions. Parenteral Used in hospital settings for acute or severe conditions, especially for biologics or during episodes of vomiting or severe infections.

Rectal Used in specific cases such as localized treatment of ulcerative colitis or constipation. Although less common, rectal administration offers targeted relief.

Gastroesophageal Reflux Disease (GERD) One of the largest segments, driven by dietary habits, obesity, and sedentary lifestyles. Strong demand for PPIs and antacids. Ulcerative Colitis Increasing prevalence and awareness are expanding this segment.

Biologics and anti-inflammatory drugs are commonly used. Crohn’s Disease A chronic and relapsing condition requiring long-term treatment. The segment benefits from innovations in immunosuppressants and biologics.

Irritable Bowel Syndrome (IBS) Rising stress levels and changing dietary patterns are contributing to its growth. Laxatives, antispasmodics, and probiotics are often prescribed. Constipation Affects a wide demographic, especially the elderly.

The segment sees consistent demand for over-the-counter laxatives and fiber supplements. Diarrhoea A frequent condition in both developed and developing regions, with anti-diarrheal drugs and rehydration solutions in high demand. Others Covers less prevalent GI conditions such as gastritis, peptic ulcers, and GI infections.

Hospital Pharmacies Serve inpatient needs and chronic condition management, especially for parenteral drugs and biologics. Retail Pharmacies A major segment for over-the-counter (OTC) drugs like antacids, laxatives, and anti-diarrheal, offering easy accessibility for consumers. Online Pharmacies Rapidly growing due to convenience, digital health awareness, and availability of subscription models for chronic therapy.

Hospitals Key users for acute and severe GI cases, including surgeries, IV treatments, and inpatient care. Clinics Handle outpatient diagnosis and treatment of common GI disorders, contributing to significant drug prescriptions.

Homecare Settings Gaining traction with the rising elderly population and preference for at-home management of chronic GI issues using oral medications. Others Includes diagnostic centers and rehabilitation facilities that may administer GI drugs as part of broader treatment plans.

North America, led by the U.S., is the largest GI drugs market due to a high prevalence of GERD, IBS, and IBD. Advanced healthcare infrastructure, high drug accessibility, and rapid adoption of biologics and digital health tools drive strong market growth.

Europe has a significant market share, supported by aging populations, strong public healthcare, and wide access to generics and biosimilars. Leading countries include Germany, the UK, France, and Italy, with active clinical research enhancing innovation.

Asia-Pacific is the fastest-growing region, driven by rising GI disorders linked to urbanization and lifestyle changes. Expanding healthcare infrastructure, affordability of generics, and rising use of herbal remedies shape the market in China, India, and Japan.

Latin America shows moderate growth, with Brazil, Mexico, and Argentina as key markets. Growth is supported by healthcare reforms and increasing use of OTC drugs, though rural access and biologic availability remain limited.

MEA is an emerging market with rising GI disease burden. GCC countries are investing in healthcare, while much of Africa relies on generics and traditional medicine. E-pharmacies and awareness campaigns are helping expand access.

The Gastrointestinal market was valued at USD 41.14 billion in 2024.

The Gastrointestinal market is projected to grow at a CAGR of 5.48% from 2025 to 2033.

Acid Neutralizers hold the largest Gastrointestinal market share.

The North America region is expected to witness the highest growth rate.

Major players include AbbVie Inc., Takeda Pharmaceutical Company Limited and Johnson & Johnson.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Gastrointestinal Drugs Market, By Drug Class

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Gastrointestinal Drugs Market, By Route of Administration

5.3 Gastrointestinal Drugs Market, By Application

5.4 Gastrointestinal Drugs Market, By Distribution Channel

5.5 Gastrointestinal Drugs Market, By End User

6.1 North America Gastrointestinal Drugs Market , By Country

6.1.1 Gastrointestinal Drugs Market, By Drug Class

6.1.2 Gastrointestinal Drugs Market, By Route of Administration

6.1.3 Gastrointestinal Drugs Market, By Application

6.1.4 Gastrointestinal Drugs Market, By Distribution Channel

6.1.5 Gastrointestinal Drugs Market, By End User

6.2 U.S.

6.2.1 Gastrointestinal Drugs Market, By Drug Class

6.2.2 Gastrointestinal Drugs Market, By Route of Administration

6.2.3 Gastrointestinal Drugs Market, By Application

6.2.4 Gastrointestinal Drugs Market, By Distribution Channel

6.2.5 Gastrointestinal Drugs Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping