Global Pine Chemicals Market

Global Pine Chemicals Market Size, Market Share & Trends Analysis Report, By Type (Tall Oil, Rosin, Turpentine, Others), By Application (Adhesives & Sealants, Printing Inks, Rubber, Coatings, Surfactants, Others), By End-Use Industry (Construction, Automotive, Paper & Packaging, Personal Care, Others), By Region (North America, Europe, Asia-Pacific, Middle East and Africa, Latin America) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2032

Report Code : ASICMR1010

CAGR: 5.9%

Last Updated : February 2, 2026

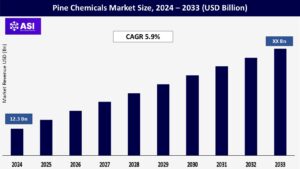

The global pine chemicals market size was valued at approximately USD 12.3 billion in 2024 and is projected to reach USD XX billion by 2033, growing at a CAGR of 5.9% during the forecast period (2026–2033). Pine chemicals, derived from pine trees, play a crucial role in various industries, including adhesives, coatings, printing inks, and rubber processing. These chemicals are sustainably sourced and are gaining traction due to their bio-based nature and eco-friendly properties.

The growing demand for sustainable and renewable chemicals, advancements in extraction and processing technologies, and increasing application scope across multiple industries are key factors driving the pine chemicals market size.

The shift toward sustainable and eco-friendly raw materials in industrial applications drives the demand for pine chemicals. The global push for bio-based alternatives in industries such as adhesives, coatings, and personal care is fueling the pine chemicals market expansion. Regulatory policies promoting sustainability and reducing reliance on petrochemical-based products further bolster the pine chemicals market growth.

Additionally, increasing consumer awareness regarding environmental concerns and health hazards associated with synthetic chemicals encourages manufacturers to shift toward bio-based ingredients. Companies are actively investing in research and development to enhance the performance and cost-effectiveness of pine-derived chemicals, making them more viable for large-scale industrial applications. The European Union’s Green Deal, the U.S. EPA’s initiatives on sustainable chemicals, and China’s drive for a circular economy are further reinforcing this trend. Moreover, industries such as cosmetics and food additives are leveraging pine-based derivatives due to their natural composition and minimal environmental impact. These factors collectively reinforce pine chemicals market growth across industrial applications.

Pine chemicals, such as rosin and turpentine, are widely used in adhesives, coatings, and rubber processing due to their superior adhesion, flexibility, and thermal resistance. The growth of the construction and automotive industries, particularly in emerging economies, is further boosting demand.

The adhesives sector is witnessing an increased demand for bio-based rosin esters due to their superior bonding properties, particularly in pressure-sensitive and industrial adhesives. The coatings industry is benefiting from the enhanced tackiness and film-forming abilities of pine-derived resins, leading to their integration into high-performance paints and varnishes. In the rubber industry, pine chemicals play a crucial role in enhancing the durability and elasticity of rubber compounds used in tire manufacturing and industrial applications.

Additionally, with stricter environmental regulations restricting the use of petroleum-based chemicals in these industries, companies are actively exploring pine-based alternatives as a means to comply with sustainability mandates while maintaining product efficiency.

Innovations in refining and processing techniques have improved the quality and performance of pine chemicals, making them more competitive with synthetic alternatives. Advanced fractionation and distillation methods are enhancing the yield and purity of rosin, turpentine, and tall oil derivatives. These improvements are strengthening competitiveness across the pine chemicals industry.

The availability of raw materials is highly dependent on the forestry industry, making the market vulnerable to supply chain disruptions, climate change impacts, and regulatory restrictions on deforestation. This affects the overall pricing and availability of pine chemicals. Additionally, unexpected shifts in raw material costs and seasonal variations in pine tree resin production can lead to market instability. The increasing emphasis on sustainable forestry practices and reforestation efforts may mitigate some of these risks, but supply chain constraints remain a significant challenge for industry players.

Although pine chemicals offer sustainability advantages, synthetic petrochemical-based alternatives often provide cost benefits and consistent quality. The price sensitivity of end-use industries could limit the adoption of pine chemicals in certain applications. Large-scale manufacturers in sectors such as adhesives, coatings, and rubber may opt for synthetic resins and chemicals due to their lower production costs, scalability, and long-term stability. The development of enhanced bio-based formulations and increased regulatory pressure on petrochemicals could help balance the competition, but pricing and performance factors continue to pose challenges for the widespread adoption of pine chemicals.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Tall Oil Rosin Turpentine Others |

| By Application |

Adhesives & Sealants Printing Inks Rubber Coatings Surfactants Others |

| By End-use Industry |

Construction Automotive Paper & Packaging Personal Care Others |

| Key Players |

Kraton Corporation Eastman Chemical Company DRT (Dérivés Résiniques et Terpéniques) Harima Chemicals Group Ingevity Corporation Georgia-Pacific Chemicals Arakawa Chemical Industries Forchem Oyj SunPine AB Resinall Corp |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Tall oil accounts for a significant share of the pine chemicals market, driven by its widespread use in adhesives, coatings, and emulsifiers. Its natural emulsifying and binding properties make it a preferred ingredient in various industrial applications. Rosin, another dominant segment, is a key ingredient in adhesives, printing inks, and rubber processing due to its excellent tackiness and water resistance.

Rosin-based products hold approximately 33.4% of the total pine chemicals market share. Turpentine, widely utilized in fragrances, pharmaceuticals, and solvent applications, is witnessing increased demand due to the rising preference for natural ingredients in consumer products. Other pine derivatives, such as pitch and sterols, are used in specialized applications, including nutraceuticals and bio-based surfactants.

The adhesives & sealants segment dominates the pine chemicals market, accounting for more than 31.9% of total demand. Rosin derivatives are widely used in industrial adhesives due to their superior bonding capabilities and environmental advantages. Printing inks represent another key application, where rosin-based resins enhance ink adhesion and drying properties. The rubber industry is a rapidly growing segment, with pine chemicals playing a critical role in improving elasticity and durability in tires and industrial rubber products.

Coatings utilize pine-based ingredients for enhanced adhesion, water resistance, and durability, making them essential in paints and varnishes. Surfactants, primarily derived from tall oil, are increasingly used in detergents and emulsifiers, particularly in personal care and household cleaning products. Other applications, including personal care, food additives, and pharmaceuticals, continue to expand as industries shift toward bio-based ingredients.

The construction sector remains a major consumer of pine chemicals, with high demand for pine-based adhesives and coatings in sustainable building materials. The automotive industry is another significant contributor, particularly in rubber processing for tire manufacturing and coatings for vehicle protection. Paper & packaging applications are growing steadily, driven by the extensive use of tall oil and rosin in paper sizing and packaging adhesives.

The personal care segment is seeing increased adoption of turpentine derivatives in cosmetics and fragrances, reflecting the industry’s shift toward natural ingredients. Other industries, including pharmaceuticals, food additives, and agrochemicals, are also leveraging pine-derived chemicals for their functional and sustainable properties.

North America accounted for 25% of the global pine chemical market share in 2024, driven by the presence of major manufacturers and strong demand from end-use industries such as adhesives, paints & coatings, and surfactants. The U.S. is a key player in the region, with companies like Kraton Corporation and Ingevity Corporation leading the pine chemicals market.

The U.S. has a well-established forest products industry, particularly in the southeastern states, where pine trees are abundant. This region is a major producer of tall oil and gum rosin, which are widely used in industrial applications. Additionally, the growing demand for bio-based and sustainable chemicals in the U.S. is driving the adoption of pine-derived products. Government initiatives, such as the BioPreferred Program, which promotes the use of bio-based products, are further supporting the pine chemicals market growth.

Canada is also contributing to the North American market, with its vast forest resources and focus on sustainable forestry practices. The country’s emphasis on reducing carbon emissions and promoting green chemistry is creating opportunities for pine chemical manufacturers. Such initiatives are expected to sustain pine chemicals market growth in North America over the forecast period.

Europe held a 30% of the pine chemicals market share in 2024, supported by stringent environmental regulations and the adoption of bio-based chemicals. The region’s focus on sustainability and circular economy principles is driving demand for pine chemicals in various applications, including adhesives, paints & coatings, and printing inks.

Countries like Finland and Sweden are major producers of pine chemicals due to their vast forest resources and advanced forestry practices. Finland, in particular, is a global leader in tall oil production, with companies like Forchem Oyj playing a significant role in the market. The European Union’s Green Deal, which aims to achieve climate neutrality by 2050, is further boosting the demand for bio-based chemicals, including pine-derived products.

Germany and France are also key markets in Europe, driven by their strong industrial base and focus on sustainable manufacturing. The growing demand for eco-friendly adhesives and coatings in the automotive and construction industries is fuelling market growth in these countries.

Asia-Pacific is projected to record the highest CAGR of 7.5% during the forecast period, driven by rapid industrialization and increasing demand for adhesives and coatings in countries like China, India, and Japan. The region’s expanding manufacturing sector, coupled with rising environmental awareness, is creating significant opportunities for pine chemical manufacturers. These trends are contributing to a steady increase in the pine chemicals market size across the Asia-Pacific region.

China is the largest market in the region, accounting for over 40% of Asia-Pacific’s pine chemical demand. The country’s booming construction and packaging industries are driving the need for adhesives and coatings, which rely heavily on pine-derived chemicals. Additionally, China’s focus on reducing reliance on petroleum-based products is boosting the adoption of bio-based alternatives.

India is another significant contributor to the Asia-Pacific market, with its growing population and urbanization driving demand for adhesives, paints, and surfactants. The Indian government’s initiatives to promote sustainable manufacturing and reduce carbon emissions are further supporting market growth.

Japan and South Korea are also key markets, with their advanced industrial sectors and focus on innovation. These countries are increasingly adopting pine chemicals in high-performance applications, such as electronics and automotive coatings.

In Southeast Asia, countries like Indonesia, Malaysia, and Vietnam are emerging as new hubs for pine chemical production and consumption. The region’s abundant forest resources and growing industrial base are creating opportunities for market expansion.

The Middle East and Africa are emerging markets for pine chemicals, with a focus on addressing energy access issues and promoting sustainable development. The region’s growing construction and packaging industries are driving demand for adhesives and coatings, which rely on pine-derived chemicals.

Saudi Arabia and the UAE are key markets in the Middle East, with their focus on diversifying their economies and reducing reliance on oil. The region’s Vision 2030 initiatives are creating opportunities for bio-based chemicals, including pine-derived products.

In Africa, South Africa is a leading market for pine chemicals, driven by its well-established forestry industry and growing demand for sustainable products. The country’s Renewable Energy Independent Power Producer Procurement (REIPPP) program is also supporting the adoption of bio-based chemicals in various applications.

Latin America is making significant strides in the pine chemicals market, with Brazil and Chile leading the way. The region’s abundant forest resources and focus on sustainable forestry practices are driving the production and consumption of pine-derived chemicals.

Brazil is the largest market in Latin America, accounting for over 50% of the region’s pine chemical demand. The country’s thriving construction and packaging industries are driving the need for adhesives and coatings, which rely heavily on pine chemicals. Additionally, Brazil’s PROINFA program, which promotes the use of renewable energy and bio-based products, is supporting the pine chemicals market growth.

Chile is another key market in the region, with its focus on sustainable forestry and an export-oriented economy. The country’s commitment to carbon neutrality by 2050 is creating opportunities for pine chemical manufacturers.

Argentina and Colombia are also emerging markets, with their growing industrial base and focus on sustainable development driving demand for pine-derived products.

The global pine chemicals market was valued at approximately USD 12.3 billion in 2024 and is projected to reach USD XX billion by 2033, growing at a CAGR of 5.9% during the forecast period (2026–2033).

Tall oil, rosin, and turpentine are the dominant segments. Rosin holds around 33.4% of the market share and is widely used in adhesives, printing inks, and rubber processing.

Pine chemicals are primarily used in adhesives & sealants (31.9% of demand), printing inks, rubber processing, coatings, and surfactants.

The North American pine chemicals market dominates the market and holds 25% of the global market share.