Heparin Market

Heparin Market Share & Trends Analysis Report, By Product Type (Low Molecular Weight Heparin (LMWH), Unfractionated Heparin (UFH), Ultra-low Molecular Weight Heparin (ULMWH)), By Source Type (Porcine, Bovine), By Route of Administration (Subcutaneous Injection, Intravenous Infusion)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 2.14%

Last Updated : March 20, 2026

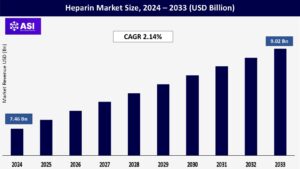

The global heparin market size was valued at approximately USD 7.46 billion in 2024 and is projected to reach USD 9.02 billion by 2033, demonstrating a compound annual growth rate (CAGR) of 2.14% during the forecast period of 2025–2033.

The heparin market is expected to grow steadily between 2025 and 2033, supported by several key trends. One of the main drivers is the increasing global burden of chronic illnesses such as cardiovascular diseases and cancer, which often require anticoagulant therapy. Additionally, as medical procedures become more advanced and widely accessible, the demand for reliable blood thinners like heparin continues to rise. Looking ahead, the market shows strong potential for continued expansion.

Despite some challenges such as supply chain constraints and growing competition, there’s a positive outlook. Innovations in formulation and delivery, along with strategic partnerships among industry players, are expected to keep the momentum going. Ultimately, the rising need for effective anticoagulation in an increasingly complex healthcare landscape makes heparin a crucial and growing component of modern medicine.

Several health conditions are driving the growing demand for heparin, with cardiovascular diseases (CVDs) leading the way. Globally, cases of heart attacks, strokes, atrial fibrillation, and blood clots like deep vein thrombosis (DVT) and pulmonary embolism (PE) are rising. Heparin plays a vital role in both preventing and treating these potentially life-threatening events. Cancer is another major factor. People with cancer face a much higher risk of developing blood clots, a condition known as cancer-associated thrombosis. As a result, heparin is frequently used to manage and reduce this risk. Diabetes also contributes to the demand. Over time, it can lead to vascular complications, which increase the likelihood of clot formation.

In these cases, anticoagulation becomes an important part of care. Lastly, patients with kidney problems, especially those undergoing dialysis, often rely on heparin. It’s essential in preventing clots from forming in the dialysis machine, ensuring the process runs safely and effectively.

Heparin plays a crucial role in a wide range of surgical procedures, from heart surgeries to orthopedic operations like knee and hip replacements, and many other major interventions. Its main job is to prevent blood clots during and after surgery, which helps reduce complications and supports better recovery for patients. As the number of complex and high-risk surgeries continues to rise around the world, the demand for heparin is growing alongside it. With medical advancements enabling more people to undergo these life-saving or life-improving procedures, the need for reliable anticoagulation has never been more important.

Most of the heparin used today comes from animal sources, especially the intestinal lining of pigs. While this method has been the standard for decades, it also brings with it several challenges. For one, disease outbreaks like African Swine Fever can significantly affect pig populations. When this happens, the supply of raw materials drops, often causing shortages and price spikes. Another issue is geopolitical dependence.

A large portion of crude heparin is produced in China, meaning that global access can be impacted by trade disputes, export restrictions, or diplomatic tensions. There are also ethical and religious considerations. Some individuals and communities are uncomfortable with, or prohibited from using, products derived from certain animals. As awareness grows, so does interest in finding alternative sources of heparin. From a manufacturing perspective, producing heparin from animal tissue brings quality control challenges. Because it’s a natural, biological product, its composition can vary from batch to batch.

This variability can complicate dosing and increase the risk of inconsistent therapeutic effects. Additionally, the risk of contamination is a serious concern. The 2008 contamination crisis highlighted how complex supply chains and multiple intermediaries can increase the chance of harmful adulteration, which can lead to dangerous side effects and major product recalls. This has led to strict, and often expensive, quality assurance measures. Finally, there’s the issue of limited availability. Extracting heparin is resource-intensive; only a few doses can be made from a single pig. So keeping up with global demand is a constant balancing act, especially if any part of the supply chain is disrupted.

As precision medicine continues to advance at a rapid pace, it’s creating challenges for regulatory systems that are still catching up. Agencies like the FDA and EMA are working to adapt, but the speed and complexity of innovation, especially in areas like gene and cell therapies, combination drug-device products, and novel diagnostic tests, often outpace existing guidelines. This can lead to uncertainty for developers and delays in bringing promising treatments to patients. One particularly tricky area is the approval of companion diagnostics, which are critical tools used to identify which patients will benefit from a specific therapy.

These require close coordination between different regulatory bodies, making the approval process lengthy and complex. Even after regulatory approval, another hurdle remains: getting treatments covered. Insurers and payers often struggle to define clear reimbursement policies for precision medicine. The high costs, personalized nature of the treatments, and limited long-term data make it hard to justify coverage, which can lead to significant delays and financial uncertainty for both patients and healthcare providers.

On a global scale, the lack of harmonized regulatory standards adds another layer of complexity. Different countries have different rules, making it challenging for companies to navigate approvals across borders and slowing the international rollout of innovative therapies. Addressing these regulatory and reimbursement issues is crucial to unlocking the full potential of precision medicine and ensuring it reaches the people who need it most.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Low Molecular Weight Heparin (LMWH) Unfractionated Heparin (UFH) Ultra-low Molecular Weight Heparin (ULMWH) |

| By Source Type |

Porcine Bovine |

| By Route of Administration |

Subcutaneous Injection Intravenous Infusion |

| Key Players |

Pfizer Inc. LEO Pharma A/S Dr. Reddy’s Laboratories, Ltd. GlaxoSmithKline plc Sanofi Aspen Holdings Fresenius SE & Co., KGaA B. Braun Medical, Inc. Sandoz (Novartis AG)

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Heparin Market is categorized by product type, by source type and by route of administration. Each segment is rapidly evolving, with different areas of the industry growing at their own pace and shifting in how much of the market they represent. Segmental analysis of the heparin market provides a detailed understanding of its various components, highlighting growth drivers and challenges within each sub-segment. This breakdown helps in identifying lucrative opportunities and formulating targeted strategies.

Low Molecular Weight Heparins (LMWHs), such as Enoxaparin, Dalteparin, and Tinzaparin, currently dominate the heparin market and are expected to maintain their leading position in the coming years. Their widespread use is driven by several advantages over traditional unfractionated heparin (UFH), including a better safety profile, more predictable anticoagulant effects, and a longer half-life. Additionally, LMWHs are easier to administer, often requiring only a simple subcutaneous injection, which makes them suitable for outpatient or even home use. They are also associated with a lower risk of Heparin-Induced Thrombocytopenia (HIT), a potentially dangerous side effect.

These benefits have made LMWHs the preferred option for the prevention and treatment of deep vein thrombosis (DVT), pulmonary embolism (PE), and certain cardiac conditions. Unfractionated Heparin (UFH), while still an important anticoagulant, is gradually losing market share due to the growing preference for LMWHs. UFH continues to be used mainly in acute care settings, such as during cardiac surgeries, dialysis procedures, and in patients with severe renal impairment. Its short half-life and the ability to quickly reverse its effects with protamine sulfate make it valuable in these high-risk situations.

However, UFH requires frequent laboratory monitoring, has a higher risk of bleeding, and carries a greater likelihood of causing HIT, which limits its broader use. Meanwhile, Ultra-low Molecular Weight Heparins (ULMWHs), including Semuloparin and Bemiparin, are emerging as the fastest-growing segment in the market. These next-generation anticoagulants offer even more targeted action, reduced bleeding risk, and highly precise dosing, making them especially promising for specialized medical applications such as cancer-associated thrombosis and certain surgical settings. As clinical adoption increases, ULMWHs are expected to play a key role in the future landscape of anticoagulation therapy.

Porcine-derived heparin currently makes up the vast majority of the global heparin supply. Its dominance is largely due to its long-standing use, well-established production processes, and what many consider superior anticoagulant activity when compared to alternatives like bovine heparin. Most low molecular weight heparins (LMWHs) are also sourced from pigs. However, relying so heavily on a single animal source brings challenges. Outbreaks of diseases like African Swine Fever can threaten supply chains, and there are also ethical and religious concerns among certain populations that make porcine products less acceptable.

Additionally, geopolitical and logistical issues tied to pig farming and exportation can add another layer of complexity. Bovine-derived heparin, while currently representing a smaller portion of the market, is starting to gain more attention. It offers a valuable alternative for regions where cultural or religious beliefs prohibit the use of pig-derived products. Beyond that, it’s seen as a way to diversify the heparin supply chain and reduce over-reliance on a single animal source. Growing regulatory acceptance and continued efforts to ensure bovine heparin’s safety and effectiveness are helping to boost interest in this segment.

At the same time, there’s growing excitement around synthetic and recombinant forms of heparin. Although still in the early stages of development and commercialization, these lab-based alternatives are being explored to overcome many of the issues tied to animal-derived sources, such as contamination risks, supply instability, and ethical concerns. While not yet widely available, synthetic and recombinant heparins hold considerable promise for the future of anticoagulant therapy.

Subcutaneous injection is currently the most common and widely used method for administering heparin, particularly because of the popularity of low molecular weight heparins (LMWHs). This route has gained strong traction thanks to its convenience patients can often administer it themselves at home without the need for hospital visits. It also tends to carry a lower risk of infection compared to intravenous methods, especially for long-term use, making it a practical and patient-friendly option.

On the other hand, intravenous infusion remains essential in acute and hospital-based settings. It is the preferred method for delivering unfractionated heparin (UFH) when a rapid response is needed, such as during surgeries, emergency interventions, or in critically ill patients. However, this route requires trained medical professionals, frequent monitoring, and carries a higher risk of systemic bleeding, which limits its use outside controlled environments.

Looking ahead, while heparin itself isn’t currently available in oral form, the growing use of direct oral anticoagulants (DOACs) is influencing the broader anticoagulant landscape. As a result, there is ongoing research into developing oral versions of heparin or heparin-like compounds. If successful, these innovations could significantly change how anticoagulation therapy is delivered in the future.

When looking at the global heparin market, it’s clear that different regions are at very different stages of development. These variations are shaped by a mix of factors, including the strength of local healthcare systems, the prevalence of chronic diseases, government regulations, and overall economic conditions. North America and Europe currently lead the market. Their dominance is largely due to well-established medical infrastructure, advanced treatment protocols, and a higher burden of chronic illnesses like heart disease and cancer, which drive consistent demand for anticoagulants like heparin.

Meanwhile, the Asia-Pacific region is emerging as the fastest-growing market. With a massive population base, rapidly developing economies, and steadily improving access to healthcare, countries in this region are seeing a surge in both demand and investment. This makes the Asia-Pacific a key area to watch for future growth. Regions like Latin America and the Middle East & Africa (MEA) may currently have smaller market shares, but they hold strong potential. As their healthcare systems continue to evolve and modernize, and as awareness and diagnosis of conditions requiring anticoagulation improve, these areas are expected to offer increasing opportunities for heparin manufacturers and suppliers.

North America continues to lead the global heparin market, consistently accounting for the largest share around 39.5% in 2024, with the United States being the primary driver of this dominance. Several factors contribute to the region’s strong position. One of the biggest reasons is the high prevalence of cardiovascular conditions such as heart attacks, deep vein thrombosis (DVT), and pulmonary embolism. These illnesses require effective blood thinners like heparin for both treatment and prevention. North America’s advanced healthcare infrastructure also plays a major role. With access to cutting-edge diagnostics, high healthcare spending, and a strong emphasis on quality care, the region is well-positioned to support the use of premium heparin products. Clinical practice in the U.S. and Canada is guided by well-established protocols that encourage the use of heparin, particularly in surgical and high-risk patients.

The presence of major pharmaceutical companies and ongoing research and development activities further strengthen the region’s leadership in innovation and product availability. Another key factor is the high number of complex surgical procedures performed across the region, which drives continuous demand for anticoagulants. In terms of market trends, North America has seen a growing preference for Low Molecular Weight Heparin (LMWH), thanks to its safer profile, ease of use, and suitability for outpatient care. Additionally, strategic partnerships and collaborations among industry players continue to shape the market and pave the way for future growth.

Europe commands a significant portion of the global heparin market, holding around 28.3% as of 2023. This strong position is shaped by a mix of demographic, medical, and institutional factors. A major driver is Europe’s aging population. As people live longer, there’s a corresponding rise in age-related chronic conditions like cardiovascular disease and venous thromboembolism (VTE), both of which often require anticoagulant treatment. Similar to North America, the burden of these conditions is prompting sustained demand for heparin-based therapies.

The region also benefits from robust healthcare systems and proactive public health initiatives, which help ensure that essential medicines like heparin are widely accessible and properly utilized. European countries are also actively investing in medical research, with ongoing studies focused on developing safer, more effective heparin derivatives and alternative therapies. Awareness campaigns around thrombosis prevention have added further momentum to market growth. In terms of trends, Europe is seeing increasing adoption of Low Molecular Weight Heparins (LMWHs), favored for their safety, convenience, and suitability in both hospital and outpatient settings. Countries like Germany, France, and the UK are particularly influential, serving as major hubs for innovation, pharmaceutical production, and clinical adoption.

The Asia-Pacific region is emerging as the fastest-growing market for heparin, and for good reason. With vast and aging populations, particularly in countries like China and India, there’s a rising tide of chronic illnesses such as cardiovascular disease and diabetes that demand effective anticoagulant therapies. This demographic shift alone is creating a strong and sustained need for heparin across the region. What’s fueling this growth even further is the rapid development of healthcare infrastructure. Governments and private sectors alike are investing heavily in hospitals, diagnostic centers, and treatment facilities, making medical care more accessible to a wider population. As disposable incomes rise, more people are also able to afford advanced treatments that include the use of drugs like heparin.

Awareness around blood clotting disorders and the need for preventive therapies is growing as well, thanks to better education and public health campaigns. Additionally, the region has a strategic edge in production. China and India are not only major consumers but also key suppliers of crude heparin and its active pharmaceutical ingredients (APIs). This local manufacturing capability ensures a more stable and cost-effective supply chain. Trends indicate a swift uptick in the use of Low Molecular Weight Heparins (LMWHs), driven by their safety and convenience. Local pharmaceutical companies are ramping up research and development efforts and increasingly collaborating with global firms to expand their reach. Within the region, India and Japan stand out as particularly promising markets poised for significant growth.

The Middle East and Africa (MEA) region is steadily emerging as a promising market for heparin, showing strong potential for future growth. A key driver of this momentum is the rising investment in healthcare infrastructure. Governments across the region are allocating more resources to improve hospitals, clinics, and diagnostic services, which is helping increase access to critical treatments like anticoagulants. Chronic diseases such as heart conditions, diabetes, cancer, and stroke are becoming more prevalent in the region, further boosting the demand for heparin as a core part of treatment and prevention strategies.

Alongside public sector efforts, there’s also a noticeable increase in private investment, with pharmaceutical and biopharma companies recognizing the region’s potential and seeking to expand their footprint. Saudi Arabia stands out as a particularly strong market within MEA, thanks to its ongoing economic development and substantial healthcare spending. The country is leading the way in modernizing medical services, making it a key destination for companies aiming to serve the regional market. However, growth doesn’t come without its challenges. Regulatory complexity and differences in healthcare access across countries in the region can make it difficult for companies to scale operations efficiently. Still, the overall trend is clear: MEA is on the radar of global pharmaceutical players and is quickly transforming from an emerging to a strategic market for heparin.

The market was valued at USD 7.46 billion in 2024.

The market is projected to grow at a CAGR of 2.14% from 2025 to 2033.

Low Molecular Weight Heparin (LMWH) segment holds the largest market share.

Asia-Pacific region is expected to witness the highest growth rate.

Major players include Baxter International Inc., B. Braun Melsungen AG, Pfizer Inc., Dr. Reddy’s Laboratories Ltd., Sanofi S.A., Fresenius SE & Co. KGaA, LEO Pharma A/S, and Opocrin S.p.A.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Heparin Market,By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Heparin Market,By Source Type

5.3 Heparin Market,By Route of Administration

6.1 Heparin Market, By Country

6.1.1 Heparin Market,By Product Type

6.1.2 Heparin Market,By Source Type

6.1.3 Heparin Market,By Route of Administration

6.2 U.S.

6.2.1 Heparin Market,By Product Type

6.2.2 Heparin Market,By Source Type

6.2.3 Heparin Market,By Route of Administration

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping