High-Level Disinfection Services Market

High-Level Disinfection Services Market Share & Trends Analysis Report By Product/Service Type (Disinfection Services, Consumables, Equipment) By Application (Surgical Instruments, Endoscopes, Ultrasound Probes, Respiratory Therapy Equipment, Dialysis Instruments, Hospital Furniture & Fixtures) By End User (Hospitals & Clinics, Diagnostic & Imaging Centers, Ambulatory Surgical Centers (ASCs), Dental Clinics, Research & Academic Institutes, Long-term Care Facilities (Nursing Homes, Rehabilitation Centers) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

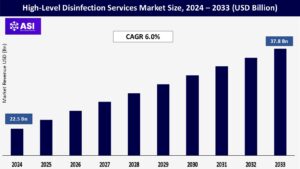

CAGR: 6.0%

Last Updated : March 7, 2026

The global High-Level Disinfection Services Market was valued at approximately USD 22.5 billion in 2024 and is projected to reach USD 37.8 billion by 2033, growing at a CAGR of 6.0% during the forecast period (2025–2033).

High-level disinfection (HLD) services are critical for the elimination of all microorganisms (except high levels of bacterial spores) on reusable medical and surgical devices in the health care environment. In particular, HLD services are critical for semi-critical instruments, which include endoscopes, ultrasound probes, and respiratory equipment. HLD services also ensure the safety and effectiveness of the instruments that touch mucous membranes or non-intact skin.

Since HLD services are highly influenced due to volume of surgical procedures, increased emphasis on infection prevention strategies, and government regulatory guidelines for sterilization in hospitals and clinics, HLD services to be in significant demand. Along with increased complexity in automated reprocessing systems, and outsourcing disinfecting services there are key indications that the market would like to see a continued expansion of HLD services.

The rising incidence of healthcare-associated infections (HAIs) remains a significant factor in the High-Level Disinfection Services Market. HAIs are a concern for public health, resulting in prolonged hospital stays, escalating healthcare costs, and increased morbidity and mortality rates. The World Health Organization (WHO) reported that 15 in 100 patients in low- and middle-income countries develop an HAI during hospital care.

In the United States alone, the Centers for Disease Control and Prevention (CDC) has reported over 687,000 HAIs occurring in acute care hospitals and approximately 72,000 deaths from HAIs each year. The continued rise in HAIs has placed more focus on the enforcement of infection prevention regulations. The Food and Drug Administration (FDA), the CDC, and the Occupational Safety and Health Administration (OSHA) all require validated disinfection practices for semi-critical devices in patient care.

In March 2024, the U.S. FDA released its revised reprocessing guidance on reusable medical devices and emphasized standardized high-level disinfection (HLD) methodology. To provide full compliance while mitigating the risk of litigation, hospitals and healthcare facilities increasingly outsource to professional disinfection service providers.

Centralized HLD services provide uniformity, traceability, and safety standards that continue to evolve, and demand for these services is increasing in hospitals, surgical centers, and diagnostic laboratories.

The world is is experiencing an unprecedented shift in healthcare towards minimizing invasive and outpatient procedures. In recent years, this has driven demand for high-level disinfection services with the additions of procedures such as colonoscopy, bronchoscopy, transesophageal echocardiography, and other urological diagnostics that utilize reusable semi-critical instruments and/or devices with contact to patients’ mucous membranes and therefore require high-level disinfection.

The American Society for Gastrointestinal Endoscopy (ASGE) reports that more than 15 million colonoscopies are performed in the U.S. alone, the majority of which are performed in outpatient surgical centers. As outpatient care and care delivery models expand, especially in the post-COVID-19 era, many healthcare systems are decentralizing their services to reduce hospital burdens and patients’ costs.

In February 2024, Olympus Corporation will launch their expanded offering of reusable endoscopes intended for outpatient diagnostic and therapeutic settings. This will contribute to an overall increase in outpatient procedures that can produce cost-effective and durable devices but also require multiple rounds of high-level disinfection.

As the number of procedures using reusable devices grows, so does the demand for routinely validated and consistent disinfection services. Centralized high-level disinfection services simplify adherence to reprocessing standards and requirements while assisting facilities with the potential for cross-contamination and hospital-acquired infections while reinforcing the role for the central disinfection services globally.

The High-Level Disinfection Services Market encounters considerable restraints due to the high initial capital and subsequent operational expenses before deploying advanced disinfection equipment and professional service contracts. Automated disinfection systems, including Automated Endoscope Reprocessors (AERs) and UV-C disinfection units, require high-cost input, installation, and maintenance, making financial implications a burden—especially to small- and medium-sized healthcare staff in developing regions.

Additionally, consumables, including chemical disinfectants (e.g., glutaraldehyde, ortho-phthalaldehyde) and single-use accessories, have added to occasionally ongoing expenses. The need for trained personnel to monitor and use the systems adds to labor costs. These financial thresholds may postpone or limit HLD services, the use of advanced HLD technologies, and professional services in resource-limited settings.

For example, amongst many hospitals across Latin America, and within some parts of Asia-Pacific, budget and reimbursement structures hinder widespread use of centralized high-level disinfection services in hospitals, thereby limiting market growth even as demand for infection control grows.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product/Service Type |

Disinfection Services Consumables Equipment |

| By Application |

Surgical Instruments Endoscopes Ultrasound Probes Respiratory Therapy Equipment Dialysis Instruments Hospital Furniture & Fixtures |

| By End User |

Hospitals & Clinics Diagnostic & Imaging Centers Ambulatory Surgical Centers (ASCs) Dental Clinics Research & Academic Institutes Long-term Care Facilities (Nursing Homes, Rehabilitation Centers) |

| Key Players |

STERIS plc Ecolab Inc. Getinge AB Advanced Sterilization Products (ASP) Olympus Corporation Cantel Medical (a Steris company) Belimed AG Metrex Research, LLC Shinva Medical Instrument Co., Ltd. Wassenburg Medical (A Member of HOYA Group) Steelco S.p.A. Tuttnauer Ltd. Parker Laboratories, Inc. |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The High-Level Disinfection (HLD) Services Market is segmented by product type, Application, and End-User. Each segment plays a vital role in enabling infection prevention across diverse healthcare settings through the safe and effective reprocessing of reusable medical devices.

In 2024, Disinfection Services had the highest market share of 43.5%, driven by increased outsourcing among healthcare facilities that are seeking validated high throughput disinfection solutions. Healthcare facilities such as hospitals and ambulatory surgical centers are relying on third-party providers for onsite and offsite HLD services.

This trend allows facilities to achieve regulatory compliance while reaping the benefits of a third-party provider’s reprocessing costs. STERIS, Ecolab, Olympus and others are expanding their service offerings with the booking of baseline HLD service and follow-up service of decontaminated scope pick-up and reprocessing.

Consumables comprising chemical disinfectants (ie. glutaraldehyde, ortho-phthalaldehyde, peracetic acid) were a large part of the market share because they are required in the manual and automated disinfection cycle. The segment is likely to grow because the market will have an ongoing need for replenishment of sterilants and disinfectant wipes; for example, HLD in healthcare consumers can vary from 24 to 36 sterilizations depending on environmental conditions.

Equipment such as automated endoscope reprocessors (AER), ultrasonic washers, and UV-C disinfection units is in high demand due to increased activity in developed markets where human error can occur and negatively affect patient outcomes. Automation can reduce human error, support consistency, yet reduce patient turnover times because time on scopes or AERs is reduced; within hospitals, large and specialty clinics are embracing capital-intensive disinfection systems.

Endoscopes were the largest application segment in 2024, with a market share of 34.1%. These semi-critical devices pose significant risks for cross-contamination if the endoscopes are not appropriately disinfected. The demand for professional high-level disinfection (HLD) solutions has been propelled by the increase in GI and pulmonary diagnostic procedures and the awareness of outbreaks due to infected endoscopes.

Surgical Instruments also continue to be a major segment, particularly surgical departments of hospitals and ambulatory surgery centers (ASCs) because of their high volume. The demand comes from the increasing inpatient and outpatient surgeries performed globally, especially in orthopedics, general surgery, and gynecology. Ultrasound Probes and Respiratory Therapy Equipment are seeing greater emphasis as they are utilized both in critical care, along with being utilized in regular diagnostics.

Incidents of transferred infections when using respiratory and imaging devices due to unsterilized devices before their use became primary services after the COVID-19 pandemic was the key catalyst for the increased focus on device disinfection before usage, as this incident shaped hospital protocols thus influencing this service segment’s demand. Instruments used in Dialysis demonstrate particular consideration for high-level disinfection between uses to limit cross-patient contamination.

Furthermore, the increase in chronic kidney disease (CKD) and its dependency on dialysis has further evened volumes to reprocess dialysis instruments. The institutional hospital category within Process of care can see hospital furniture and fixtures such as mattresses, stretchers, and movable equipment standardized into HLD workflows, again especially within the ICU and isolation units where surface disinfection is the focus to control infection transmission.

Hospitals and Clinics top the market and command an impressive share of over 54% of total revenue in 2024. With significant patient populations, high surgical volumes, and regulatory requirements to maintain sterile environments, hospitals have the greatest need for both disinfection equipment as well as professional services.

Massive capital expenditures on automated disinfection systems and standardizing reprocessing responsibility have commonality across major hospitals worldwide. Diagnostic and Imaging Centers experience annual growth because of the routine use of reusable transducers, ultrasound probes, and endocavitary devices.

While hospitals shifted from inpatient to outpatient volume growth in diagnostic settings, ensuring compliance and acceptance of probe processing policies is now of increasing importance. Ambulatory Surgical Centers (ASCs) are a fast-growing market segment based on increased day surgeries and minimally-invasive procedures. Since ASCs operate with lean staffing models and limited staff training, they are ideally suited to outsource HLD services.

Dental Clinics comprise a small but growing segment, as offices in metropolitan areas have an increased focus on implied HLD certification. Although the published practice guidelines mentor repeated use of dental tools on multiple patients, dental health boards are mandating adherence to infection control disinfection protocols more comprehensively than ever before. Research Institutes and Academic Institutions routinely use a variety of reusable equipment including simulators in clinical labs and simulation facilities.

Since training requires a simulation of clinical scenarios and testing obligations generally include clinical task performance, research and academic institutions are likely to adopt flexible outsourcing of HLD services over time. Long-term Care Facilities (nursing homes and rehabilitation centers) are emerging end-users. With elderly and immunocompromised populations at risk for infections, the proper disinfection of mobility aids, respiratory devices, and patient contact surfaces is becoming more recognized and increasing demand in this market segment.

According to an estimate for the 2024 market, North America will represent 41.2% of the market share based on its established healthcare infrastructure with strict regulations and high levels of awareness for infection control. The US is the lead contributor due to the increase in the usage of reusable medical instruments and mandates for various compliance guidelines from the FDA, CDC, and The Joint Commission.

The demand for surgical volumes, outpatient procedures, and the desire for automated disinfection systems is growing in the region, as well as companies such as STERIS Corporation, Ecolab, and Cantel Medical are based in this region, thereby encompassing a more expansive industry for different professional disinfection services and equipment. It’s worth mentioning that with increasing awareness for healthcare-associated infections (HAIs) and litigation, healthcare organizations are financially investing in centralized and onsite high-level disinfection services.

Europe is a large part of the HLD services market with mature healthcare systems of countries like Germany, France, UK, Austria, and the Netherlands. These systems have strong regulations with respect to infection prevention and control, including some standards and guidelines from the European Centre for Disease Prevention and Control (ECDC), bringing renewed focus to verified disinfection processes.

In the last few years, healthcare facilities in Eastern and Central Europe have been investing more in automated products for disinfection, as well as outsourcing reused medical device reprocessing. For example, the number of endoscopic procedures in Germany jumped from 1,292,572 in 2018 to 2,261,878 by 2023, increased demand for known, consistent, and scalable HLD solutions. Furthermore, Europe is experiencing an increase in cross-border healthcare, which only adds to the need for standardized protocols for disinfection.

The Asia-Pacific region will exhibit the highest growth, of 8.2% CAGR during the forecast period (2025 to 2033). Countries like China, Japan, India and South Korea are well positioned for growth due to anticipated growth in hospital surgical volumes, the increased recognition of the risks of infection, and better investments in healthcare.

The rise of hospital-acquired infections (HAIs), particularly in urban areas where the population density is high, has sparked national infection control initiatives and initiatives to recommend reprocessing guidelines. In 2023, India’s Ministry of Health advocated that all tertiary hospitals implement standardized endoscope reprocessing practices, resulting in a major increase in demand for HLD services and consumables. In addition, local infection control companies are emerging with cost-effective disinfection systems customized for regional use, which has encouraged adoption in secondary and tertiary care settings throughout Asia.

Latin America and the Middle East & Africa (MEA) are experiencing moderate growth in the HLD services market due to gradual improvements in healthcare infrastructure and infection prevention efforts. In Latin America, Brazil, Mexico, and Chile are seeing increases in elective surgeries and endoscopic diagnostics, which require thorough disinfection protocols; however, uneven access to healthcare services and economic disparities slow the spread of investment towards HLD service providers.

In the MEA region, countries such as Saudi Arabia, the UAE, and South Africa are investing considerable national resources in hospital hygiene and accreditation programs, and as a result, demand for HLD services such as outsourcing and automated systems is increasing. Nevertheless, some barriers to entry persist, including a lack of personnel trained in HLD services, the cost of equipment, and overall regulatory enforcement is often inconsistent continuing to limit scalable penetration in many areas of the region.

The market was valued at USD 22.5 billion in 2024.

The market is projected to grow at a CAGR of 6.0% from 2025 to 2033.

Hospitals & Clinics hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include STERIS plc, Ecolab Inc. and Getinge AB

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 High-Level Disinfection Services Market, By Product/Service Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 High-Level Disinfection Services Market, By Application

5.3 High-Level Disinfection Services Market, By End User

6.1 North America High-Level Disinfection Services Market, By Country

6.1.1 High-Level Disinfection Services Market, By Product/Service Type

6.1.2 High-Level Disinfection Services Market, By Application

6.1.3 High-Level Disinfection Services Market, By End User

6.2 U.S.

6.2.1 High-Level Disinfection Services Market, By Product/Service Type

6.2.2 High-Level Disinfection Services Market, By Application

6.2.3 High-Level Disinfection Services Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping