High Potency Active Pharmaceutical Ingredients Market

High Potency Active Pharmaceutical Ingredients Market Share & Trends Analysis Report, By Type (Innovative HPAPI, Generic HPAPI), By Manufacturer Type (Captive Manufacturer, Merchant Manufacturer), By Synthesis Type (Synthetic, Biotech), By Therapeutic Application (Oncology, Hormonal Disorders, Glaucoma, Others)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

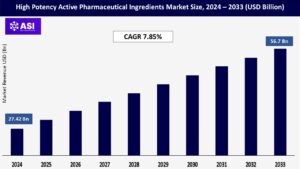

CAGR: 7.85%

Last Updated : November 22, 2025

The global High Potency Active Pharmaceutical Ingredients Market size was valued at approximately USD 27.42 billion in 2024 and is projected to reach USD 56.7 billion by 2033, growing at a CAGR of 7.85% during the forecast period (2025–2033).

The High Potency Active Pharmaceutical Ingredients (HPAPI) Market encompasses the development, manufacturing, and supply of highly pharmacologically active compounds used in extremely low doses to produce therapeutic effects. HPAPIs are primarily utilized in the treatment of cancer, hormonal disorders, and autoimmune diseases, where targeted therapy is essential.

These compounds are characterized by their high biological activity and low daily dose requirements often less than 10 mg per day necessitating specialized handling, containment, and manufacturing practices to ensure safety for workers and prevent cross-contamination.

Key properties of HPAPIs include high target specificity, potency at low concentrations, and the need for sophisticated infrastructure such as isolators and closed systems in production facilities. The growing trend toward personalized medicine, increased incidence of chronic diseases, and the rise in oncology drug development are key factors driving the expansion of the HPAPI market.

One of the primary drivers of the HPAPI market is the increasing focus on oncology and targeted therapies. Cancer treatment often requires highly potent drugs that can act on specific molecular targets with minimal side effects. HPAPIs play a critical role in the formulation of such drugs, enabling lower dosages while maintaining therapeutic efficacy.

With the global burden of cancer rising and precision medicine gaining traction, pharmaceutical companies are investing heavily in the development of targeted drugs based on HPAPIs. This trend is further supported by advancements in biotechnology and a growing number of HPAPI-based drugs receiving regulatory approvals.

Manufacturing HPAPIs involves complex containment and safety requirements due to their potency and toxicity. Most pharmaceutical companies prefer to outsource this process to specialized Contract Development and Manufacturing Organizations (CDMOs) that have the necessary infrastructure and regulatory expertise.

This outsourcing trend is growing due to cost-efficiency, scalability, and reduced time to market. The expansion of global CDMOs with dedicated high-containment facilities has enabled pharmaceutical firms to develop HPAPI-based drugs without investing heavily in their own manufacturing capabilities, thus accelerating the market’s growth.

Due to their highly potent and hazardous nature, HPAPIs are subject to stringent regulatory guidelines from agencies such as the FDA, EMA, and OSHA. Manufacturers must implement robust containment strategies, including advanced cleanroom technologies, closed system isolators, and strict occupational safety procedures to prevent cross-contamination and protect worker health. Establishing such infrastructure requires significant capital investment and ongoing compliance costs, making entry into the HPAPI market a major financial and operational challenge.

Smaller pharmaceutical companies may find it difficult to meet these requirements, while even large firms may face delays in product development and market entry due to regulatory audits and complex safety assessments. These barriers can slow down innovation and restrict the scalability of HPAPI manufacturing.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Innovative HPAPI Generic HPAPI |

| By Manufacturer Type |

Captive Manufacturer Merchant Manufacturer |

| By Synthesis Type |

Synthetic Biotech |

| By Therapeutic Application |

Oncology Hormonal Disorders Glaucoma Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The High Potency Active Pharmaceutical Ingredients Market is segmented by Type, Manufacturer Type, Synthesis Type and Therapeutic Application. Each factor contributes significantly to advancing precision medicine, improving therapeutic outcomes in critical disease areas like oncology, and ensuring safe and efficient drug manufacturing practices.

As the demand for targeted and potent therapies grows, HPAPIs will remain at the forefront of pharmaceutical innovation, driving the evolution of modern drug development and specialized treatment strategies.

The market is segmented into Innovative HPAPI and Generic HPAPI. Innovative HPAPIs lead the market owing to their use in patented, cutting-edge drugs developed for specific therapeutic targets, particularly in oncology and rare diseases. These APIs are typically developed in-house by pharmaceutical innovators and command premium pricing due to their clinical efficacy and exclusivity.

On the other hand, Generic HPAPIs are gaining ground as patent expirations open opportunities for biosimilars and generic formulations, driving demand in cost-sensitive regions and expanding access to potent therapies at lower prices.

The market is divided into Captive Manufacturers and Merchant Manufacturers. Captive manufacturers are large pharmaceutical companies that produce HPAPIs internally for their own drug products, maintaining tight control over quality, intellectual property, and regulatory compliance.

In contrast, Merchant manufacturers or contract development and manufacturing organizations (CDMOs) supply HPAPIs to various pharmaceutical clients, making this segment increasingly important due to the growing trend of outsourcing complex manufacturing processes to specialized, high-containment facilities.

The market is segmented into Synthetic HPAPIs and Biotech HPAPIs. Synthetic HPAPIs dominate the market, widely used in small-molecule drugs with well-established processes, high scalability, and cost-efficiency.

However, Biotech HPAPIs produced via advanced biotechnological methods like fermentation or cell culture are growing rapidly, driven by the rise of biologics, immunotherapies, and antibody-drug conjugates. These biotech-based APIs require specialized production environments and are integral to modern targeted therapies.

The HPAPI market is segmented into Oncology, Hormonal Disorders, Glaucoma, and Others. Oncology is the largest application segment, as most HPAPIs are used in anti-cancer drugs due to their strong cytotoxic effects and ability to act at low doses.

Hormonal disorders, including endocrine therapies and contraceptives, represent a significant market due to sustained demand across age groups and genders. Glaucoma, though a niche application, benefits from the use of HPAPIs in advanced ocular treatments. The Others category includes applications in infectious diseases, autoimmune conditions, and cardiovascular disorders, reflecting the expanding therapeutic use of highly potent molecules.

North America holds the largest share of the global HPAPI market, led by the United States. The dominance is attributed to a strong pharmaceutical industry, advanced R&D infrastructure, and the high prevalence of chronic diseases such as cancer, which demand potent and targeted therapies.

The presence of major pharmaceutical companies and contract manufacturing organizations (CMOs), as well as stringent regulatory frameworks (e.g., FDA guidelines for containment and occupational safety), ensures high-quality production and innovation. Increasing investments in biologics and oncology-focused drug development further drive market growth in this region.

Europe is the second-largest market for HPAPIs, supported by robust pharmaceutical production capabilities in countries like Germany, Switzerland, France, and the UK. The region benefits from strong government support for healthcare innovation, strict regulatory compliance (e.g., EMA standards), and high investment in oncology and specialty medicines.

Additionally, the demand for outsourcing HPAPI production to EU-based CMOs is growing due to their expertise in high-containment manufacturing. Europe’s focus on sustainable and green chemistry practices is also influencing HPAPI production technologies.

Asia Pacific is the fastest-growing HPAPI market, driven by rapid industrialization of the pharmaceutical sector, especially in India and China, which are emerging as global manufacturing hubs for HPAPIs and intermediates. Cost-effectiveness, skilled labor availability, and growing domestic demand for oncology drugs and hormonal therapies support regional growth.

However, regulatory compliance and containment challenges remain key concerns. Countries like Japan and South Korea are also contributing through high investments in innovative biologics and targeted therapies. Expansion of local CMOs and global partnerships are shaping the market dynamics positively.

In Latin America, the HPAPI market is in a developing stage, with moderate growth observed in countries such as Brazil, Mexico, and Argentina. Rising healthcare awareness, increasing cancer incidence, and government initiatives to improve access to advanced therapies are encouraging pharmaceutical innovation.

However, limited local manufacturing capacity for HPAPIs and dependence on imports restrain growth. Investments in public-private partnerships and gradual improvements in regulatory frameworks are expected to support market expansion in the coming years.

The Middle East & Africa region represents a nascent but growing HPAPI market. Countries like South Africa, Saudi Arabia, and the UAE are gradually improving pharmaceutical manufacturing and healthcare delivery capabilities.

While HPAPI production is still minimal, rising cancer prevalence, increasing demand for specialty treatments, and expanding healthcare infrastructure are driving interest in high-potency therapies.

The market remains highly import-dependent, but international collaborations and government incentives for local pharmaceutical growth could boost regional development over time.

The high potency active pharmaceutical ingredients market was valued at USD 27.42 billion in 2024.

The high potency active pharmaceutical ingredients market is projected to grow at a CAGR of 7.85% from 2025 to 2033.

Innovative HPAPI hold the largest market share.

The North America region is expected to witness the highest growth rate.

Major players include Lonza Group AG, Thermo Fisher Scientific Inc. and Catalent Inc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 High Potency Active Pharmaceutical Ingredients Market, By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 High Potency Active Pharmaceutical Ingredients Market, By Manufacturer Type

5.3 High Potency Active Pharmaceutical Ingredients Market, By Synthesis Type

5.4 High Potency Active Pharmaceutical Ingredients Market, By Therapeutic Application

6.1 North America High Potency Active Pharmaceutical Ingredients Market, By Country

6.1.1 High Potency Active Pharmaceutical Ingredients Market, By Type

6.1.2 High Potency Active Pharmaceutical Ingredients Market, By Manufacturer Type

6.1.3 High Potency Active Pharmaceutical Ingredients Market, By Synthesis Type

6.1.4 High Potency Active Pharmaceutical Ingredients Market, By Therapeutic Application

6.2 U.S.

6.2.1 High Potency Active Pharmaceutical Ingredients Market, By Type

6.2.2 High Potency Active Pharmaceutical Ingredients Market, By Manufacturer Type

6.2.3 High Potency Active Pharmaceutical Ingredients Market, By Synthesis Type

6.2.4 High Potency Active Pharmaceutical Ingredients Market, By Therapeutic Application

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping